South Korea's currency closed the first half of 2026 as one of the worst performers among Group of 20 nations, and the scale of the equity exodus driving it rivals — and by some measures surpasses — the country's most turbulent financial crises.

Part A: The Currency Collapse in Numbers

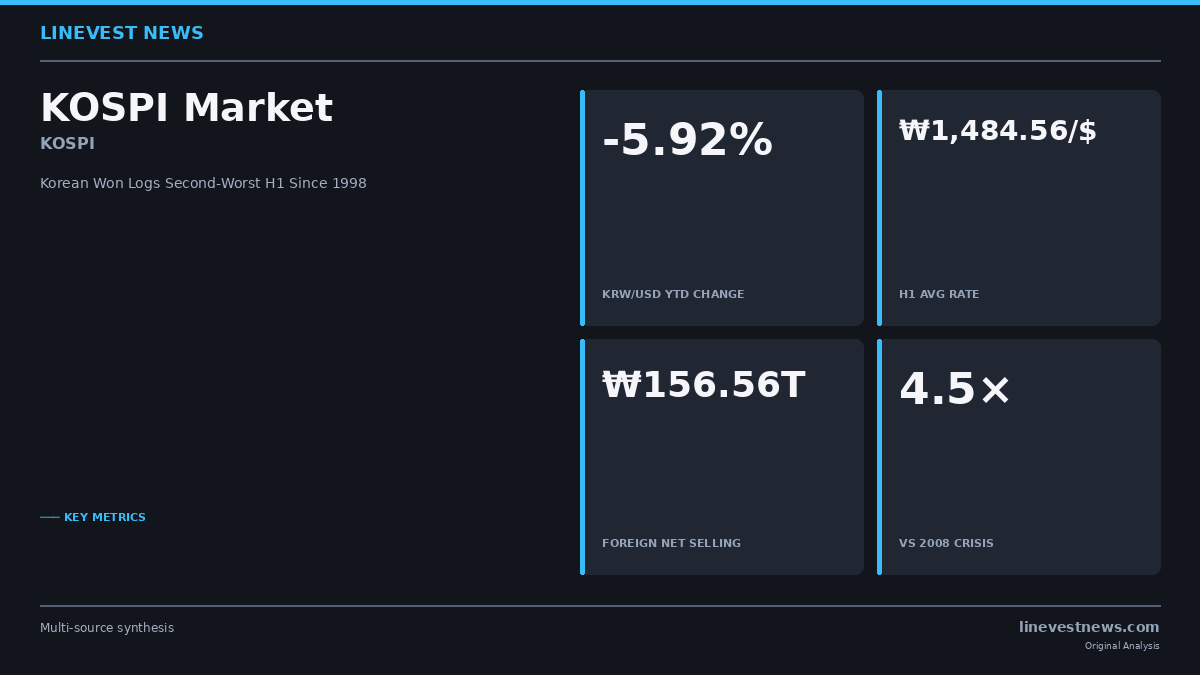

The Korean won depreciated 5.92% against the US dollar through July 3, pushing the first-half average exchange rate to 1,484.56 won per dollar — the second-highest H1 average on record after the 1,493.08 won logged during the 1998 Asian financial crisis, according to Korea Herald data.

Among G20 nations, only Turkey's lira (-8.23%) and Indonesia's rupiah (-6.56%) fell further against the greenback, placing the won as Asia's second-biggest major-currency loser behind the rupiah.

The won first breached the 1,500-won threshold in March 2026 for the first time since the 2008 global financial crisis, triggered by an escalation in Middle East tensions. Although the currency retreated briefly to the low 1,400-won range in April, it rebounded above 1,500 by mid-May and has remained elevated since.

The Scale of the Equity Exodus

The primary driver of won weakness has been an unprecedented withdrawal of foreign capital from Korean equities. From January 2 through July 3, overseas investors sold a net ₩156.56 trillion (approximately USD 102.3 billion at prevailing rates) of shares on the KOSPI.

To put that in perspective: the total net foreign selling recorded during all of 2008 — the year the global financial crisis toppled Lehman Brothers — was ₩34.58 trillion. The 2026 figure through only the first half of the year is more than 4.5 times that full-year crisis total.

Part B: Market Impact and Investor Implications

Currency Drag on USD Returns

For foreign investors holding KOSPI exposure in dollar terms, won depreciation acts as a silent second loss. Even where individual stock prices in won have risen, a 5.92% currency slide erodes the equivalent USD return dollar-for-dollar. An investor holding a KOSPI position that returned +5% in won terms through June 30 would have realized near-zero gains in dollar terms.

This dynamic helps explain the self-reinforcing nature of the current cycle: foreign selling pressures the won downward, which deepens dollar-denominated losses, which in turn accelerates further selling — a feedback loop that has amplified both the equity outflows and currency weakness beyond what domestic fundamentals alone would suggest.

What Makes 2026 Different From Prior Crises

Korea has weathered two previous episodes of comparable currency stress: the 1997–98 Asian financial crisis, when the won briefly collapsed past 2,000 per dollar, and the 2008–09 global financial crisis, when it peaked near 1,580. In both cases, net foreign selling was contained to single-digit trillion-won sums on an annualized basis.

What distinguishes 2026 is scale and concentration. The earlier crises were driven by broader emerging-market contagion and systemic credit stress. The current episode is concentrated in Korean equities specifically — particularly large-cap semiconductor and technology stocks that account for an outsized share of KOSPI's free-float weight.

Who Absorbs the Selling

Samsung Electronics (005930.KS) and SK Hynix (000660.KS) together represent roughly 30% of KOSPI's market capitalization by free-float weight. The bulk of net foreign selling has been concentrated in these two names, consistent with global fund managers reducing overweight positions in a sector that surged on AI-demand expectations but now faces pricing uncertainty and geopolitical risk around US chip-export controls.

The KOSPI index itself has tested the 8,000-level in early July — a sharp reversal from its all-time highs — reflecting both the selling pressure and the compounding FX headwind on portfolio valuations.

BOK in the Crossfire

The Bank of Korea faces a difficult calibration: cutting rates to cushion slowing growth would risk widening the rate differential with the United States and further weakening the won, while keeping rates elevated could prolong domestic credit stress. Governor Rhee Chang-yong has repeatedly stressed the bank's readiness to deploy FX smoothing operations if volatility becomes disorderly, without committing to a specific exchange rate floor.

What Would Signal Stabilization

For foreign investors watching for a re-entry signal, analysts point to three conditions: (1) a sustained slowdown in the weekly net-selling pace from overseas funds, (2) a won that stabilizes — or recovers — below 1,450 per dollar, and (3) tangible progress on US–Korea trade negotiations, which have added a geopolitical layer to the risk calculus.

Until those conditions materialise, the combination of currency drag and equity-market volatility is likely to keep many offshore allocators on the sidelines — or actively reducing Korean exposure. The won's near-1998 first-half average is the starkest statistical summary of what has been a bruising six months for foreign holders of Korean equities.

Sources: Korea Herald · Korea Exchange (KRX) net foreign flow data