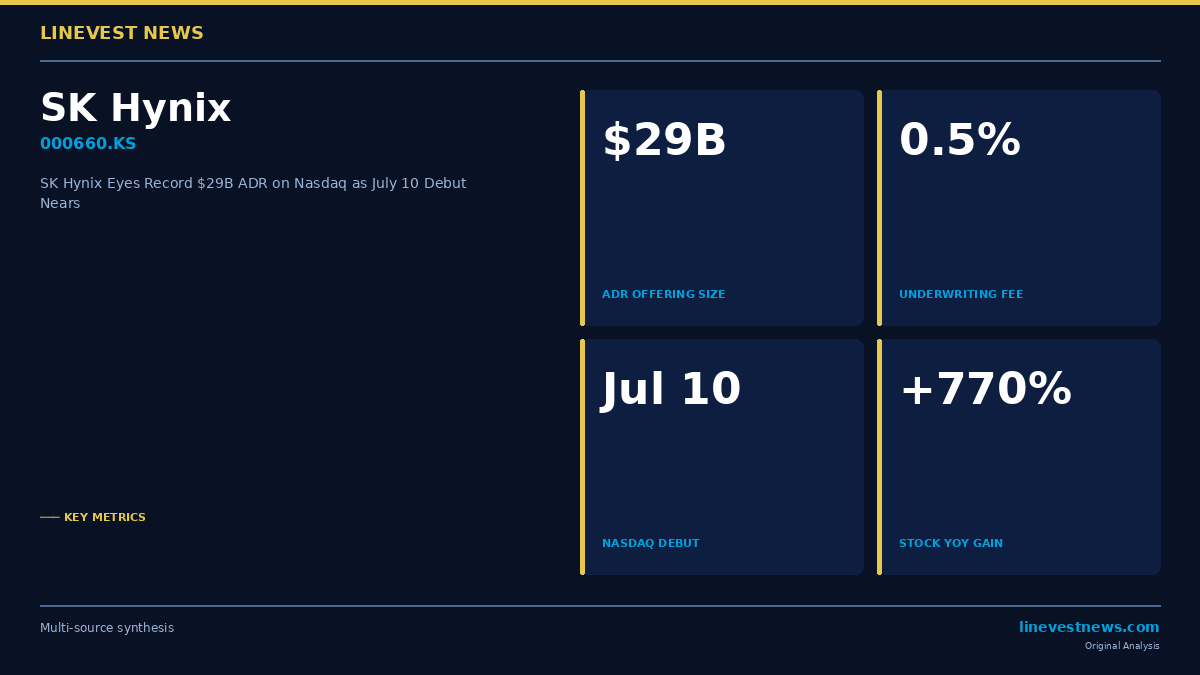

SK Hynix is closing in on what could be the largest American Depositary Receipt offering in history, with the South Korean memory chipmaker weighing a deal that would raise up to approximately $29 billion on Nasdaq and begin trading as early as July 10, according to people familiar with the matter.

The offering, which would involve issuing new ADRs equivalent to up to 2.5% of SK Hynix's total outstanding shares, is being arranged by Bank of America, Citigroup, Goldman Sachs and JPMorgan Chase. Underwriting fees are expected to come in at roughly 0.5% of proceeds — around $130 million — a figure that sits well below the 1%-plus typically charged on large US share sales. The company declined to comment when contacted by Korea Herald.

Part A — The Offering

At $29 billion (₩45.45 trillion), the deal would surpass Alibaba's $25 billion New York listing in 2014 — the largest IPO in history at the time — as the record holder for an ADR transaction. Saudi Aramco's 2019 domestic IPO raised $29.4 billion, and even SpaceX's record $86 billion offering paid a 0.67% underwriting fee — making SK Hynix's proposed rate unusually lean.

The structure is a secondary offering of newly issued shares in ADR form, not a conversion of existing Seoul-listed common stock. Each ADR is expected to represent a fixed ratio of the underlying 000660.KS shares traded on KOSPI, providing US institutional investors direct synthetic exposure to the company without navigating Korean brokerage arrangements.

Deliberations were still ongoing as of July 4, and final terms — including the exact share count and pricing range — remain subject to change.

Part B — Korean Market Implications

Why Nasdaq, and why now

SK Hynix's market capitalisation has ballooned to approximately $1.1 trillion won-adjusted on the back of a 770% stock gain over the past twelve months, driven largely by its near-monopoly position in high-bandwidth memory (HBM) used in AI accelerators. A Wall Street listing carries a strategic rationale beyond the capital raise itself: it embeds SK Hynix into US index funds, broadens the shareholder base among American institutional investors, and subjects the company to a higher-visibility governance standard that could partially close any discount relative to US semiconductor peers.

Dilution arithmetic for KOSPI holders

At 2.5% of total shares, the offering is modest in dilution terms. At SK Hynix's current price, earnings per share dilution would be under 2.5% on a fully-diluted basis — largely offset if the proceeds are deployed into capacity that compounds future earnings. The 000660.KS share has already absorbed a -15% single-day selloff this week before recovering 10% the next session, suggesting the market is pricing in some form of capital action.

Use of proceeds: capacity ahead of HBM5

The company has earmarked the capital for three specific projects: Phase 1 of the Yongin Semiconductor Cluster wafer fabrication facility, the Cheongju P&T7 advanced packaging plant, and procurement of EUV (extreme ultraviolet) lithography machines. All three feed directly into next-generation HBM production. SK Hynix's roadmap calls for HBM4 volume shipments in H2 2026 and HBM5 qualification beginning in 2027 — the new fab and packaging infrastructure is essential to meeting those timelines without cannibalizing existing capacity at its Icheon and Cheongju campuses.

What the ADR means for foreign ownership dynamics

Foreign investors already hold roughly 50% of SK Hynix's free float on KOSPI. A Nasdaq-listed ADR pool would allow US funds to accumulate exposure without appearing in Korea's foreign ownership registry — a structural shift that could gradually reduce the signal value of the Korea Stock Exchange's daily "net foreign buying" figure for this name. It also means that a future forced-selling event in the ADR market (margin calls, index rebalances) would not necessarily appear as KOSPI selling pressure, complicating the usual read-through for domestic traders.

Competitive context

Samsung Electronics (005930.KS) holds a dominant share of DRAM and NAND markets but has no ADR equivalent. Micron Technology (MU), the closest US comp, trades at a revenue multiple broadly in line with post-ADR SK Hynix valuations — the Nasdaq listing is partly intended to capture that premium. SK Hynix is targeting the valuation gap between its KOSPI multiple and where a US-listed AI-infrastructure hardware company would trade.

Sources: Korea Herald · Yahoo Finance / Bloomberg · TechTimes