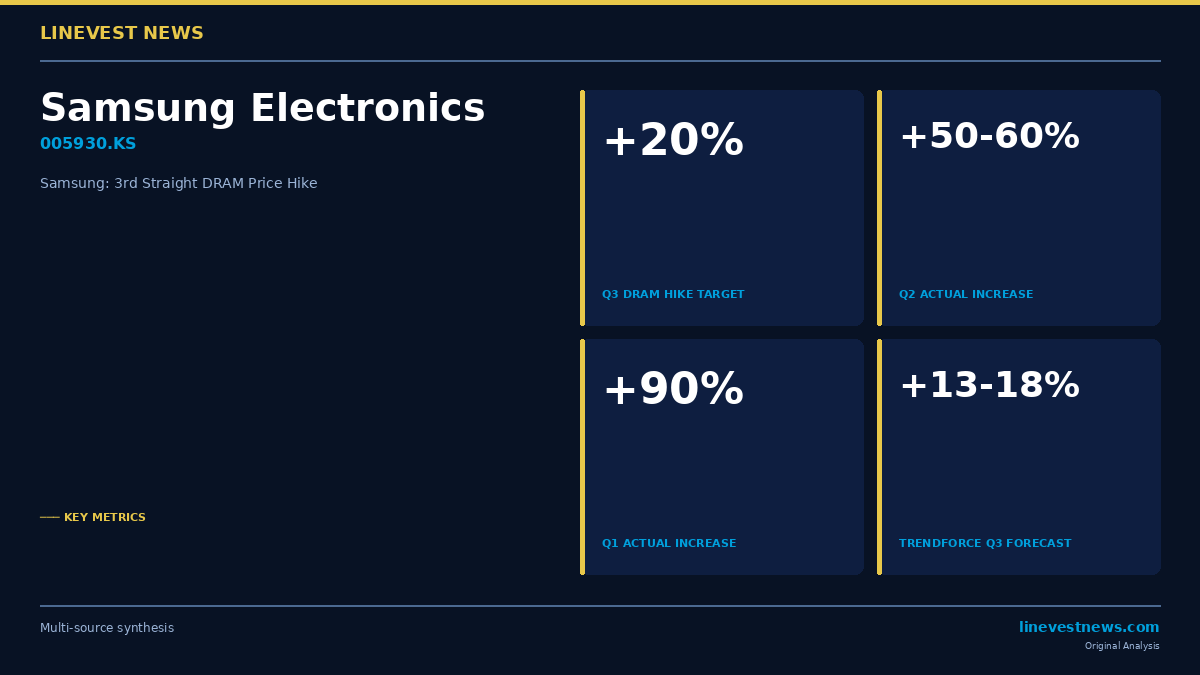

Samsung Electronics (005930.KS) is targeting a third consecutive quarter of DRAM price increases, seeking to raise average selling prices by up to 20% in the July–September period — a move that would extend one of the most aggressive pricing cycles in the memory industry's recent history.

Part A — The Price Hike Plan

Industry sources confirmed that Samsung verbally notified select customers, including Chinese electronics manufacturers, of its intent to increase DRAM prices in Q3 2026. An executive at one Chinese electronics company told local media the company "held related discussions with Samsung Electronics last month and was verbally notified of the DRAM price increase plan."

The planned increase follows a steep two-quarter run-up: DRAM average selling prices rose more than 90% quarter-on-quarter in Q1 2026 before climbing a further 50–60% in Q2. A 20% sequential gain in Q3 — if fully realised — would mark the third straight quarter of double-digit price growth.

Samsung's ambitions are not limited to standard commodity DRAM. Research firm CINNO Research forecasts LPDDR5X (8GB) contract prices to rise roughly 20% in Q3, while TrendForce notes that Samsung is negotiating "aggressively" and LPDDR hikes could exceed 20%, though customer acceptance remains uncertain.

TrendForce itself projects Q3 DRAM contract prices will advance 13–18% from Q2 levels, citing supply that remains "extremely constrained" even as weaker demand for consumer electronics moderates the pace of gains. The research house also forecasts NAND flash contract prices to climb 10–15% quarter-on-quarter during the same period.

Samsung Electronics has not issued an official statement on its Q3 pricing strategy.

Part B — What It Means for Korean Investors

Diverging trajectories within Korea's memory duopoly

The pricing push creates a notable distinction between Korea's two chip giants. Samsung's memory revenue mix carries heavier exposure to commodity DRAM — standard server and mobile modules sold at market rates — meaning it captures more of the absolute price swing than its domestic rival. TrendForce data show Samsung's ASP growth in recent quarters has outpaced SK Hynix (000660.KS), a pattern driven by this commodity-skewed mix.

SK Hynix, by contrast, derives a larger share of its DRAM revenue from high-bandwidth memory (HBM) sold under negotiated contracts tied to AI accelerator shipments. HBM pricing tends to be set through quarterly bilateral agreements rather than the open market, dampening both the upside and the downside relative to commodity swings. In a rising-price environment, SK Hynix's HBM premium provides margin stability; Samsung's commodity exposure provides a larger top-line uplift.

Pricing cycle: powerful, but decelerating

The sequential deceleration — from a 90% jump in Q1 to roughly 55% in Q2 to a targeted 20% in Q3 — suggests the memory pricing cycle is maturing rather than accelerating. That pattern historically signals either a peak or a plateau: demand-side pressure (PC, smartphone) is beginning to offset the AI-server-driven supply crunch. TrendForce's forecast of 13–18% actual realisation (versus Samsung's 20% ask) implies some customer pushback, particularly from handset original equipment manufacturers in China already contending with thin margins.

For investors, a decelerating but still-positive pricing trend implies continued upward earnings revisions for Samsung and SK Hynix in Q3, though the pace of upgrades may slow from what was seen after Q1 and Q2 results.

Downstream implications

Chinese consumer-electronics makers — which account for a material share of DRAM and LPDDR demand — face tightening input costs for a third consecutive quarter. Handset brands relying on LPDDR5X for flagship devices will need to absorb or pass through higher component costs, potentially compressing margins or delaying product launches.

Micron's parallel strategy of locking in 16 long-term supply agreements with price floors indicates that customers across sectors are accepting structural pricing floors rather than betting on a price collapse — a bullish signal for sustained memory margins through at least 2027.

Market context

The KOSPI closed at 8,088 on July 3, 2026, up 5.76% after a sharp rebound in semiconductor names. Samsung Electronics and SK Hynix each gained more than 8% on that session as domestic funds absorbed foreign selling pressure. Against that backdrop, fresh evidence of durable pricing power reinforces the bull case for Korea's memory sector — provided the LPDDR negotiations produce closer to the 20% ask than the 13% floor.

Sources: Korea Herald · Seoul Economic Daily · TrendForce

"