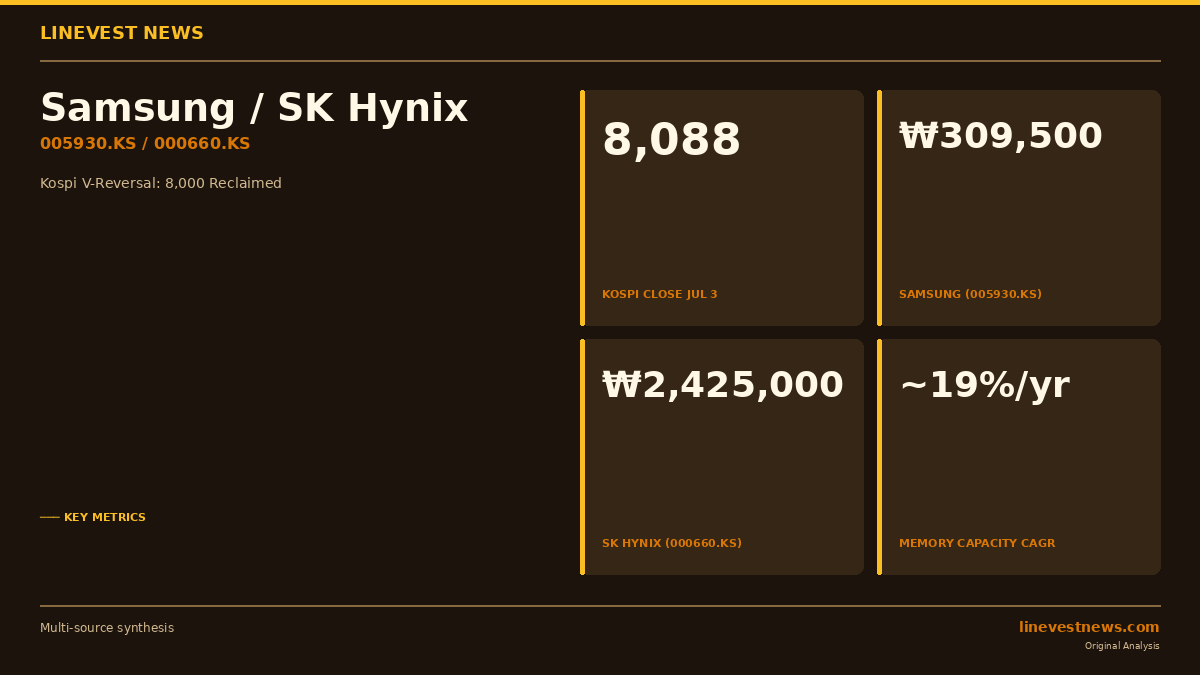

South Korea's chip duo staged one of the sharpest reversals of the year on Friday, July 3, and the pattern of the move matters more than its size. The Kospi (Korea's benchmark equity index) closed at 8,088.34, up 5.76%, after diving below 7,400 intraday — a swing violent enough to trigger a buy-side sidecar, the automatic five-minute halt on program-buy orders, per the Korea JoongAng Daily. Samsung Electronics (005930.KS), the world's largest memory-chip maker, finished at ₩309,500 ($226), up 8.22%; SK Hynix (000660.KS), the leading supplier of high-bandwidth memory for AI accelerators, jumped 10.88% to ₩2,425,000 ($1,770), according to The Korea Times. Both had cratered the prior session, when the Kospi fell 7.89% to 7,648.

For a portfolio manager in New York, the question isn't the bounce — it's whether the memory trade just broke. The overnight trigger was real: US chip stocks sold off for a second day after Meta signaled it would resell spare AI computing capacity, feeding fears that hyperscaler capex — and therefore memory demand — is peaking. Micron fell 5.49%, Marvell 9.84%, Intel 5.25%, AMD 4.26% and Broadcom 2.41%, per Chosun Biz, which also noted a soft US jobs report (June nonfarm payrolls rose 57,000 versus a 115,000 consensus), nudging up the odds the Federal Reserve holds rates through December.

Why It Matters

Why Seoul decoupled. Rather than following Wall Street down, Korean institutions bought the dip aggressively — a net roughly ₩2.5 trillion ($1.8 billion) by early afternoon, while individuals and foreigners were net sellers, according to Chosun Biz. Lee Jae-won, an analyst at Yuanta Securities Korea, characterized the prior day's rout as "a valuation de-rating driven by noise rather than fundamental damage." The tape agreed: all ten of the Kospi's largest stocks closed higher.

The fundamental anchor is supply, not demand. On July 2, SEMI (the global semiconductor-equipment and materials industry association, whose members include Micron, Samsung and SK Hynix) sent a letter to senior Trump-administration officials warning that "interventions that distort pricing or capacity decisions risk prolonging the demand downturn," as first reported by Bloomberg and corroborated by Tom's Hardware. The letter followed reports that Apple sought Washington's help to source memory from China's CXMT and YMTC to ease a shortage. Crucially, SEMI projects industry memory capacity growing about 19% annually yet still trailing AI-driven demand, leaving laptop, automotive and appliance memory tight for an extended period, per Chosun Biz. That is a shortage thesis — the opposite of the glut fear that drove the US selloff.

The cycle context cuts both ways. Memory is famously cyclical: in the 2022–2023 downturn, SK Hynix posted a full-year 2023 net margin near ‒28% and Samsung cut output by roughly half before the slump bottomed, as CNBC reported in November 2023. The current AI-led upcycle has already lifted Samsung 11.52% and SK Hynix 15.77% in the month to June 30, per Korea Exchange (KRX) data cited by Chosun Biz. But the same report flagged how choppy the tape has become: newly listed single-stock 2x leverage ETFs badly lagged their underlyings over that month because daily rebalancing bleeds returns in volatile sessions — a reminder that a 10% intraday round-trip is now routine for these names.

What the rally is not pricing. Structural demand has a domestic supply answer that the market has largely shrugged off. On June 29, President Lee Jae-myung unveiled a ₩800 trillion (about $584 billion, by Seoul Economic Daily's conversion) plan for four memory front-end fabs in the Honam region of southwest Korea — ₩400 trillion each from Samsung and SK Hynix — alongside a ₩392 trillion ($286 billion) packaging hub in the Chungcheong region and ₩312 trillion ($228 billion) of investment in the Yeongnam region, per Newsis. Yet Samsung and SK Hynix shares fell on the announcement day, with coverage from CNBC and BigGo Finance citing power, water, workforce and multi-year build timelines. That muted reaction, just four sessions before Friday's surge, is the clearest evidence that this market is trading the memory cycle — not headline capex.

The data point that settles it. The debate between "AI glut" and "memory shortage" will be adjudicated by earnings, not price action. Samsung typically issues preliminary quarterly guidance in early July ahead of its full Q2 report, scheduled for July 23 per its investor-relations calendar, with SK Hynix reporting later in the month. Operating-profit guidance and any commentary on HBM pricing and contract terms will show whether Friday's bargain-hunters or Thursday's sellers read the cycle correctly.

Sources: Korea JoongAng Daily · The Korea Times · Chosun Biz · Tom's Hardware · CNBC · Bloomberg · Newsis

This article is journalism, not investment advice. LineVest is not a registered investment adviser. Figures are drawn from the cited sources as of publication; won-to-dollar conversions use an approximate rate of 1,370 KRW per USD unless a cited source specifies otherwise. Verify all data independently before making financial decisions.