Core revenue recovery and a 30% cut in recurring R&D expense deliver Hanall's first operating profit in over a year, even as short-term borrowings surge to pre-fund a dense schedule of Phase 3 clinical readouts through 2026.

Source: Q1 2026 Quarterly Report — Filed with DART | Consolidated Financial Statements | Unit: ₩ billions

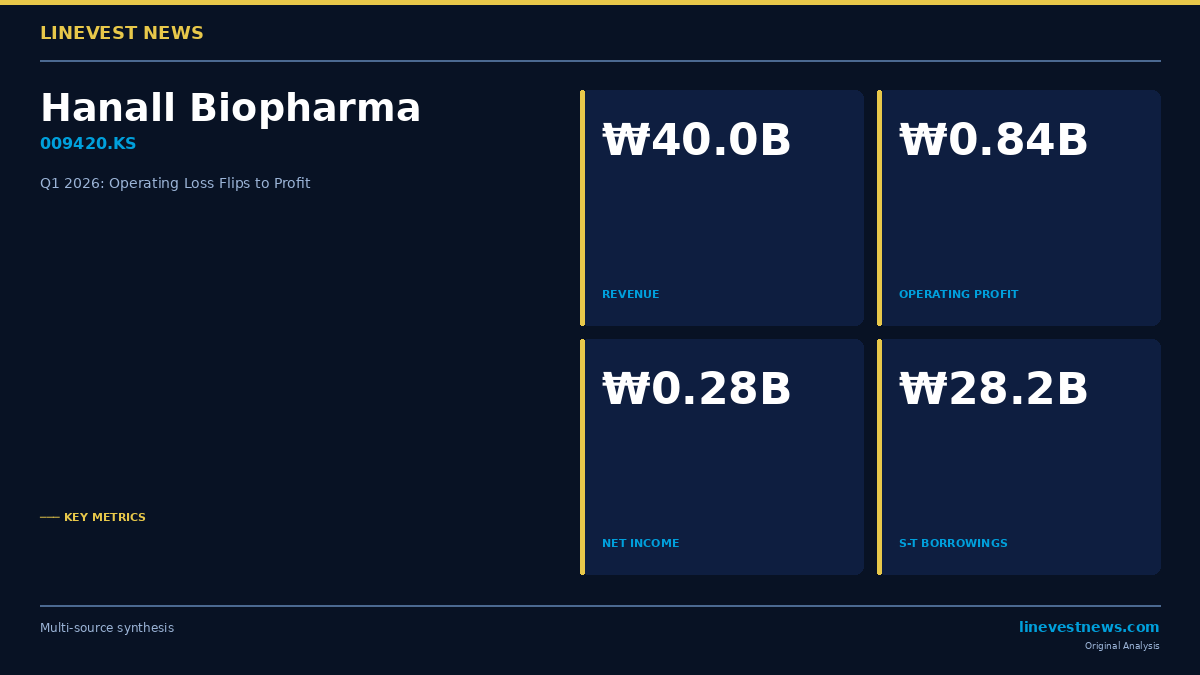

Hanall Biopharma posted consolidated revenue of ₩40.03 billion in Q1 2026, up 10.7% year-over-year, converting an operating loss of ₩390 million into a profit of ₩840 million — a swing of more than ₩1.2 billion at the operating level in a single quarter. Net income turned positive at ₩280 million, confirming the improvement reflects genuine operating momentum rather than one-time gains. Beneath the headline recovery, however, lies a significant balance sheet repositioning: short-term borrowings surged 79.0% from ₩15.74 billion to ₩28.17 billion in a single quarter, lifting the debt-to-equity ratio from 39.3% to 50.2%. The capital buildup is most naturally read as deliberate runway preparation ahead of multiple Phase 3 clinical catalysts — above all, the batoclimab top-line data in thyroid eye disease expected in H1 2026, an event that, depending on its outcome, could either validate or undermine the core investment thesis for the stock.