Samsung Life Insurance032830.KS

About Samsung Life Insurance

Samsung Life Insurance is South Korea's largest life insurer, selling death-protection, health, savings, and annuity products through one of the country's biggest tied-agent networks as well as bancassurance and digital channels. It manages an extensive investment portfolio of bonds, loans, and equities backing long-duration policy liabilities, and controls asset-management and other financial subsidiaries. The company occupies a pivotal place in the Samsung Group as a principal shareholder of Samsung Electronics, a holding that represents a large share of its asset value. Earnings blend insurance-service results with investment income, against a backdrop of a mature domestic life market.

The stock is often analyzed less as an insurer than as a governance instrument: its Samsung Electronics stake makes it central to the group's control structure, and long-discussed Korean legislation that would force insurers to mark and potentially reduce large affiliate equity holdings is the single biggest structural swing factor. Demographic decline and a saturated protection market cap organic growth, pushing the story toward capital management. Interest-rate levels drive both investment yields and the economics of legacy high-guarantee policies. Insurance capital rules govern payout capacity, and the company's dividend orientation attracts yield-focused holders.

Founded in 1957 as Dongbang Life Insurance, the company was acquired by the Samsung Group in 1963 and grew into Korea's dominant life insurer during the country's high-growth decades, when rising incomes drove demand for savings-type policies. It was renamed Samsung Life Insurance in 1989 and remained privately held within the group until a landmark 2010 initial public offering, then one of Korea's largest ever. The company anchors the group's financial wing, with stakes in Samsung Fire & Marine, Samsung Card, and asset-management units arranged beneath it, while its historic shareholding in Samsung Electronics makes it a load-bearing pillar of family control.

The insurer gathers premiums through one of Korea's largest exclusive agent forces, plus bank counters and digital channels, and earns profit from mortality and expense margins on protection products and from investment spreads on the assets backing long-duration liabilities. Under current insurance accounting, the stock of future profit embedded in in-force policies, the contractual service margin, is the metric analysts follow, and health-focused protection products build it faster than savings business. Asset management earns fees through subsidiaries. With the domestic market mature, growth levers are product mix, overseas investments, and capital efficiency, while the vast bond portfolio ties results to interest-rate movements.

Company profile by LineVest editorial. Journalism, not investment advice. Commission a full DART-based report on Samsung Life Insurance →

Samsung Life Insurance coverage

2 articles

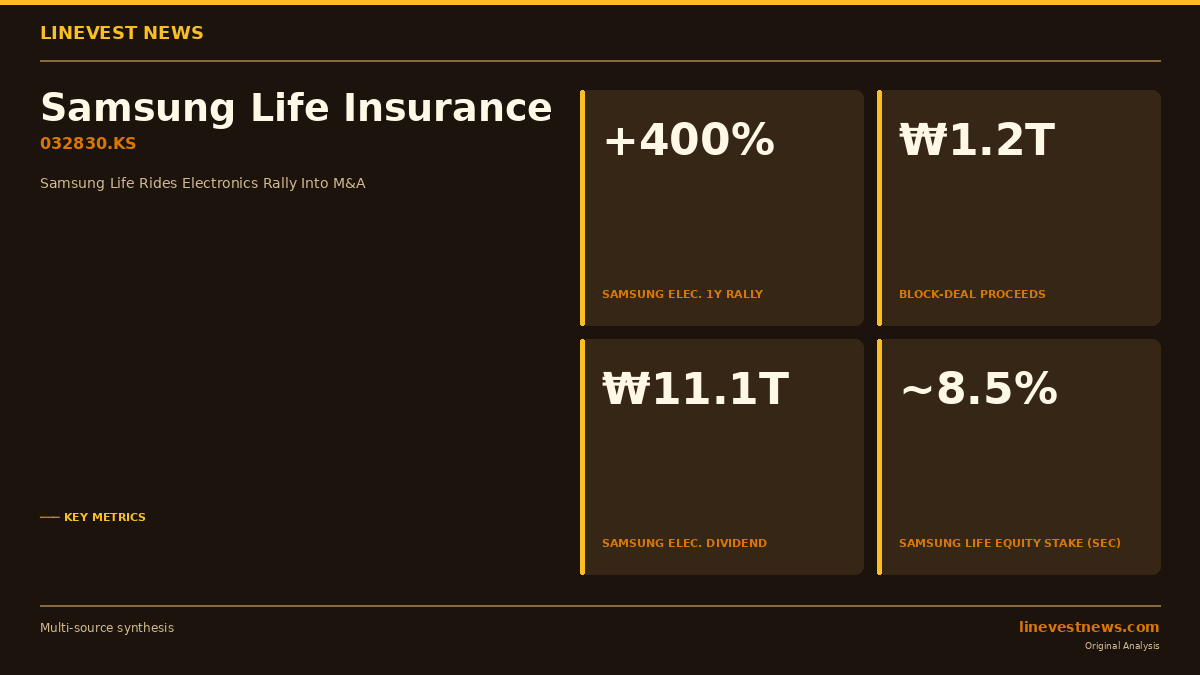

Samsung Life Turns Samsung Electronics' ₩1.2 Trillion Block Deal Into an M&A War Chest

Samsung Life Insurance converts record Samsung Electronics block-deal proceeds into M&A firepower, bidding for KDB Life and positioning Samsung Securities for an IMA push.

Premium

PremiumSamsung Life (032830.KS) Q1 2026: ₩18T Capital Surge as Profit Jumps 89%

A bond-revaluation tailwind lifted equity by nearly a third in a single quarter, even as core insurance margins held steady.

Frequently asked questions

What does Samsung Life Insurance do?

Samsung Life is South Korea's largest life insurer, selling death protection, health coverage, savings, and annuity products through a large agent network, banks, and digital channels. It manages an extensive investment portfolio backing its policy liabilities, controls asset-management subsidiaries, and holds a pivotal equity stake in Samsung Electronics.

Who controls Samsung Life Insurance?

The founding Lee family and Samsung C&T together hold the controlling interest, a structure central to the Samsung Group because Samsung Life's stake in Samsung Electronics helps secure family control of the flagship. Institutional and retail investors hold the remainder following the company's 2010 public listing.

How can foreign investors get exposure to Samsung Life Insurance?

Samsung Life trades on the Korea Exchange under ticker 032830. It maintains no overseas depositary receipts, so foreign investors typically buy the Seoul-listed shares via brokers with Korean market access or hold Korea-focused ETFs and regional insurance funds in which the company appears.

Answers are editorial summaries for general information, not investment advice.

Go deeper than the headline

You just read what happened. Here's how to read what it means.

The Korean market week, in one email

Every Saturday: the week's key KOSPI & KOSDAQ stories, earnings and foreign flows — picked from our daily coverage. Free, no card required.

Want it every morning before the open? LineVest Daily — $2.99/mo →

Full report on Samsung Life Insurance

We read Samsung Life Insurance's latest DART filing in full — financials under K-IFRS, governance, and what it means for the stock. PDF in your inbox within 3 hours.

$12 · one-time

Get the Samsung Life Insurance reportFollow the whole market

Reading several Korean stocks a week? Read every analysis article the moment it publishes — full daily KOSPI & KOSDAQ coverage plus the 90-day archive.

$9.99 · monthly

SubscribeIndependent journalism based on primary DART filings — not investment advice. No brokerage affiliation.