Samsung Life Insurance (032830.KS), South Korea's largest life insurer by assets, is pivoting from a decade of conservative stewardship to an aggressive capital-deployment stance—and the trigger is unmistakably the chipmaking juggernaut next door.

Part A: The Rally That Filled the Coffers

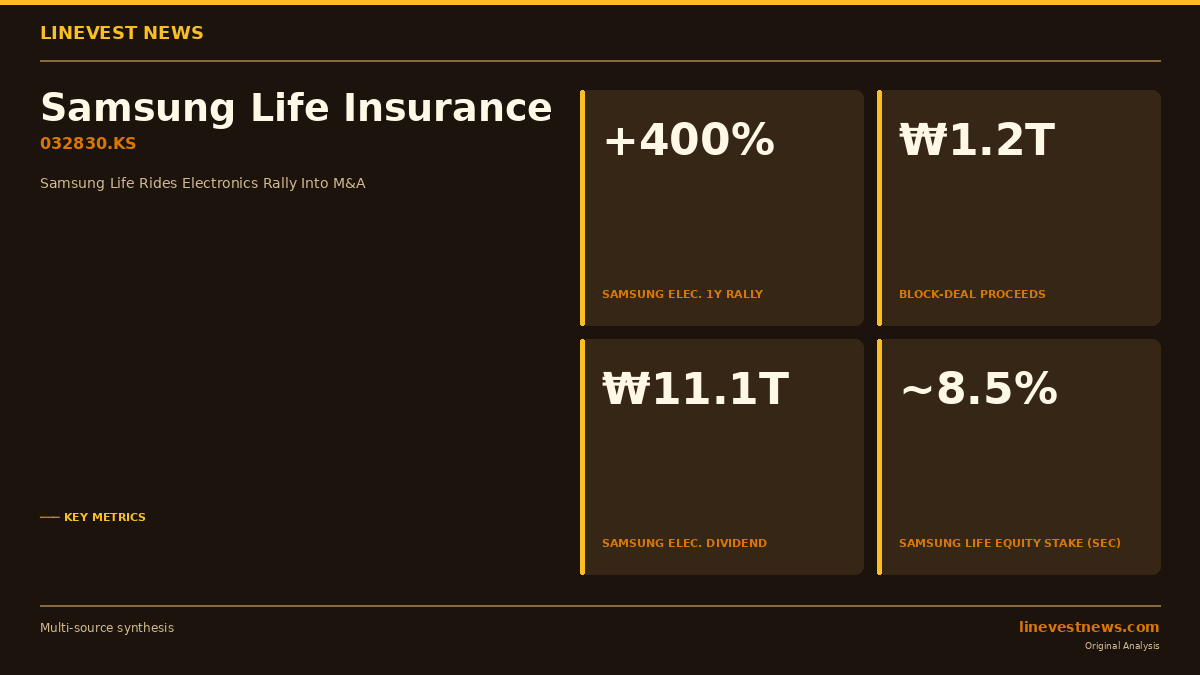

Samsung Electronics (005930.KS) shares have surged nearly 400% over the past year, climbing from roughly ₩50,000 to above ₩300,000. The move, fueled by an AI-driven memory supercycle and a sharp re-rating of South Korea's chip sector, has created a windfall for the electronics giant's largest institutional shareholder: Samsung Life.

Under South Korea's Financial Industry Structure Improvement Act (금산법), financial companies are barred from holding more than 10% of a non-financial subsidiary. As Samsung Electronics repurchased and cancelled treasury shares, Samsung Life's effective stake automatically crept upward—threatening to breach that 10% ceiling. In March 2026, Samsung Life sold 0.11% of Samsung Electronics, approximately 6.24 million shares, through a block deal. The transaction raised more than ₩1.2 trillion (approximately USD 820 million at current rates).

A second stream of inflows is imminent. Samsung Electronics confirmed at its March 2026 annual general meeting a total FY2026 dividend of ₩11.1 trillion—₩9.8 trillion in regular dividends and ₩1.3 trillion in special dividends. Kiwoom Securities estimates the electronics group's 2024–2026 cumulative free cash flow consensus has widened to ₩265 trillion, projecting that Samsung Life's earnings could increase by as much as ₩6 trillion by 2027.

Part B: From Passive Holder to Active Deal-Maker

Armed with fresh capital, Samsung Life is moving quickly. Industry sources say the insurer has entered the preliminary bidding for KDB Life Insurance (KDB생명), a mid-sized insurer put on the block by the state-owned Korea Development Bank. Samsung Life has formed a dedicated M&A integration team—a clear signal of serious intent, given that earlier frontrunners were Korea Investment Holdings and Heungkuk Life Insurance.

Samsung Life's management publicly foreshadowed this shift. At a recent investor relations event, the company said it would deploy surplus capital for overseas M&A in insurance and asset management, diversification of investment assets, and exploration of the senior-living business segment—a clean break from its historical posture of holding Samsung Electronics stock and collecting dividends.

Samsung Securities Is Next in Line

Investors are equally focused on what this means for Samsung Securities (016360.KS), 29.6%-owned by Samsung Life (including related parties). Samsung Securities' equity capital exceeded ₩8 trillion as of end-March 2026, clearing the threshold required to operate installment-payment note and integrated management account (IMA) businesses—profit-rich product lines that mega-brokers covet.

The capital race among Korean securities firms is intensifying: NH Investment Securities raised ₩650 billion via a rights offering in 2025 and received an additional ₩400 billion from NongHyup Financial Group in June 2026. KB Financial Group recently approved a ₩1 trillion equity injection into KB Securities, which would lift its equity base to approximately ₩9 trillion. Samsung Life is non-committal on specific timelines, but its official position—"we will comprehensively review options in line with shareholder-value enhancement and company growth principles"—leaves the door open.

Broader Ripple Effects

Samsung Life sits at the apex of Samsung's financial group: it holds 100% of Samsung Asset Management, 71.8% of Samsung Card, and 19.6% of Samsung Fire & Marine Insurance, in addition to its Samsung Securities stake. A more aggressive Samsung Life creates a flywheel effect across the conglomerate's financial subsidiaries.

For foreign investors assessing the Samsung group, the structure offers an underappreciated read-through: as Samsung Electronics continues to generate record cash flows through the AI memory supercycle, a non-trivial portion of that economic value will migrate to Samsung's financial subsidiaries through dividends, block deals, and secondary-market transactions—before eventually flowing to end shareholders. Samsung Life's current solvency ratio remains above regulatory guidance (K-ICS framework), providing the balance-sheet room to pursue deals without undermining policyholder protection.

Sources: Chosunbiz · Kiwoom Securities research