Korea's Courts Are Rewriting Platform Antitrust Rules — And Coupang Holds the Biggest Liability

As Naver's algorithm case returns to Seoul's appellate bench and KakaoMobility's fine is reversed, Korea's highest court is carving out a more permissive standard for self-preferencing that sets it apart from Europe.

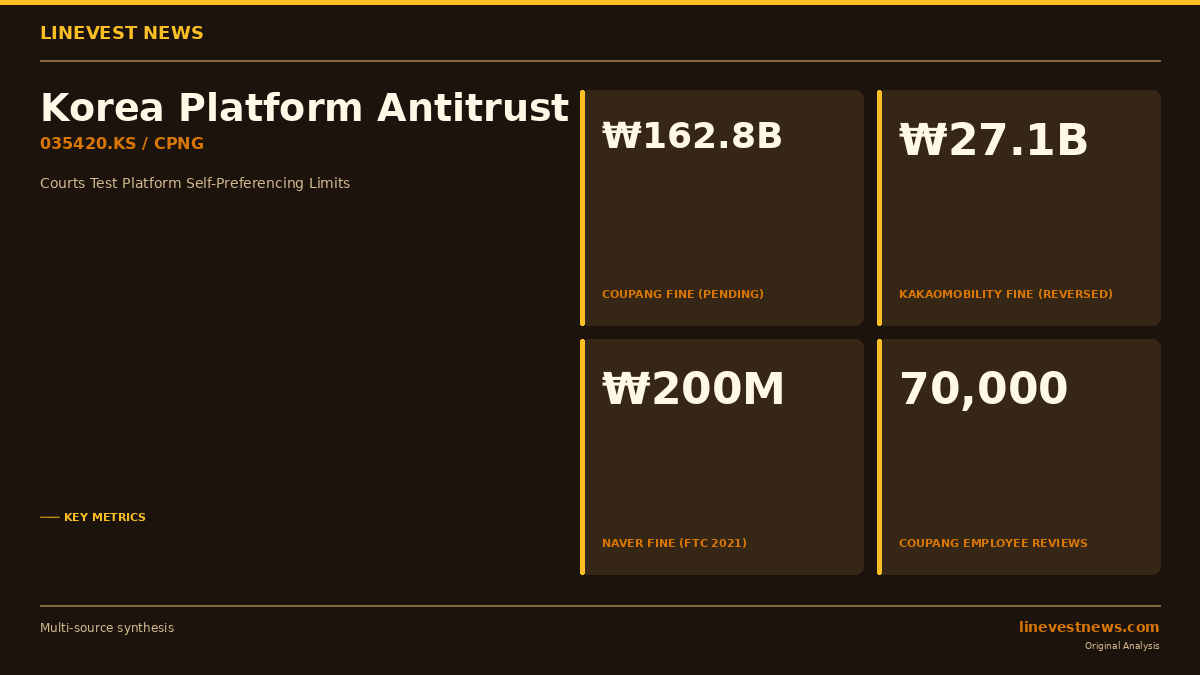

TL;DR

- Korea's Supreme Court (Nov 2025) ruled platform self-preferencing is not automatically illegal — it needs a rationality test, narrowing FTC enforcement power

- Naver's video search algorithm case opened its remand hearing on July 8 at Seoul High Court; FTC is challenging the Supreme Court's factual premise

- KakaoMobility won a full reversal of its ₩27.1 billion fine at appellate level; FTC has appealed to the Supreme Court

- Coupang carries the heaviest exposure: ₩162.8 billion (~USD 118 million) in pending fines at Seoul High Court, compounded by fake-review allegations against its own employees

- Korean enforcement trajectory diverges significantly from the EU Digital Markets Act, reducing structural antitrust risk for most Korean platform investors — with Coupang as the notable exception

Part A: Three Simultaneous Battles Over Who Controls the Algorithm

Naver: A ₩200 Million Fine That Could Set the National Precedent

Korea's Fair Trade Commission (FTC) opened the first enforcement salvo in January 2021, citing Naver (035420.KS) for adjusting its video search algorithm so that NaverTV content ranked higher than rival platforms. The corrective order came with a ₩200 million (approximately USD 145,000) fine — small in dollar terms but enormous in precedent weight.

Naver contested the ruling in court. In February 2023, the Seoul High Court upheld part of the FTC's position. Naver appealed to the Supreme Court.

In November 2025, the Supreme Court remanded the case back to Seoul High Court, partially reversing Naver's loss. The Supreme Court's reasoning was significant: Naver had granted extra search ranking points only to NaverTV videos that had passed an additional internal quality-screening process (the "테마관" thematic channel vetting). The court held that applying a quality filter before boosting content carries "some rationality and a possibility of enhancing consumer utility" — and therefore cannot be automatically treated as anticompetitive.

On July 8, 2026, the Seoul High Court held the first hearing of the remand (파기환송심) before the Administrative Sixth Division (Chief Judges Kim Min-gi, Choi Hang-seok, Park Young-ju). The FTC did not concede. Prosecutors argued the Supreme Court's factual assumption was flawed: the bonus points were tied to NaverTV thematic channel membership, not to individual video quality assessments. If the FTC can prove its interpretation on remand, Naver's partial win at the Supreme Court could unravel.

KakaoMobility: ₩27.1 Billion Fine Reversed — Awaiting Supreme Court Verdict

The FTC levied a ₩27.1 billion fine against KakaoMobility in February 2023, alleging the company had adjusted KakaoT's taxi dispatch algorithm from 2019 onward to route calls preferentially to KakaoT Blue franchise taxis at the expense of independent drivers.

KakaoMobility appealed. In May 2025, the Seoul High Court ruled in KakaoMobility's favor, canceling both the corrective order and the full ₩27.1 billion fine. The FTC has appealed that ruling to the Supreme Court, which is now the deciding forum. The outcome could either validate KakaoMobility's algorithmic business model or impose a harder antitrust standard across Korean platform logistics.

Coupang: ₩162.8 Billion and the Fake-Review Complication

Coupang (CPNG, NYSE) faces the largest financial exposure of the three. In 2024, the FTC imposed a ₩162.8 billion (~USD 118 million) fine for two alleged violations:

- Manipulating its search algorithm to rank Coupang's private-label (PB) products above competitors without corresponding quality justification

- Directing approximately 70,000 employee-written positive reviews to PB products, allegedly misleading consumers

Coupang's legal position: placing PB products prominently is standard retail merchandising, legally indistinguishable from how physical supermarkets shelf their own brands. On the employee reviews, Coupang argues 70,000 reviews represent just 0.3% of the 25 million total PB reviews on the platform, and employee reviewers actually gave lower average ratings than general consumers.

The case is currently at Seoul High Court, where both the Naver and KakaoMobility appellate precedents will exert gravitational force on the judges.

The Legal Standard Taking Shape

Seoul-based antitrust attorneys quoted in legal industry analysis point to a consistent doctrinal direction emerging from Korean courts: self-preferencing alone does not establish illegality. The burden on the FTC has shifted. Regulators must demonstrate both that the platform had anticompetitive intent and that the conduct actually restricted competition or distorted consumer choice.

"Platform operators have a core right to determine, within their own service environment, which products or content to prioritize," said one attorney specializing in IT regulation. "But that business judgment must be backed by demonstrable evidence of a rational, consumer-benefit rationale."

Part B: What This Means for Investors in Korean Platform Stocks

Reading the Liability Map

| Company | FTC Fine | Current Status | Investor Risk |

|---|---|---|---|

| Naver (035420.KS) | ₩200M | Remand at Seoul High Court | Low financial exposure; behavioral remedy possible |

| KakaoMobility (Kakao 035720.KS subsidiary) | ₩27.1B | FTC appealing to Supreme Court | Moderate; Kakao's own equity depends on outcome |

| Coupang (CPNG, NYSE) | ₩162.8B | Seoul High Court — not yet ruled | High — represents ~6 months of FY2025 net income |

Naver's fine is financially immaterial. Even an adverse ruling on remand would not impose costs that move Naver's earnings meaningfully. The risk is behavioral: if the FTC obtains a structural remedy requiring Naver to redesign its algorithm architecture, the impact on NaverTV's competitive positioning could be more significant than the penalty itself.

KakaoMobility is non-listed, but its performance flows through Kakao Corp (035720.KS). The Supreme Court's upcoming ruling is the key binary event: a Kakao victory would accelerate the platform-permissive trend; an FTC victory would signal that even algorithmic dispatch systems face hard legal exposure.

Coupang's situation is the most complex. The ₩162.8 billion fine alone is material — it approximates Coupang's reported Q4 2025 net income. More importantly, the fake-review component introduces a dimension the other cases don't have. Courts have consistently viewed algorithmic prioritization as a business strategy question; they view employee-directed consumer deception differently. Coupang's argument that 70,000 reviews represent a rounding error assumes reviewers behaved identically to general consumers — an argument the FTC will contest.

Korea vs. EU: A Structural Divergence in Platform Risk

The Korean Supreme Court's November 2025 ruling creates a marked divergence from Europe's Digital Markets Act (DMA), which designates specific large platforms as "gatekeepers" subject to per se prohibitions on self-preferencing regardless of consumer benefit arguments. European platforms like Google, Apple, and Meta cannot use a rationality defense — the conduct itself triggers liability.

Korea has implicitly rejected that approach. The Supreme Court's framework requires the FTC to prove harm, not merely demonstrate preference. For foreign investors holding Korean platform stocks, this divergence is material: the structural antitrust liability that has depressed valuations of European tech firms is less likely to materialize in the Korean legal environment.

That said, the Korean framework is not permissive in absolute terms. The Coupang case demonstrates that fake-review conduct — the type of deception that goes beyond algorithmic business judgment — will still attract significant penalties. Investors should separate two distinct categories of platform conduct: (1) algorithm-as-strategy, where Korean courts lean permissive; and (2) consumer deception through fabricated data, where enforcement remains firm.

The Ripple Effects: What Comes After the Verdicts

Three outcomes are running in parallel, and the sequencing matters. If the FTC wins at the Supreme Court in KakaoMobility before the Naver remand concludes, the FTC may revive more aggressive arguments in Seoul High Court. If the KakaoMobility Supreme Court ruling again favors the platform, the Naver case almost certainly resolves in Naver's favor on remand — and Coupang gains a powerful algorithmic-preferencing defense (though not a defense against the fake-review charge).

For Coupang investors, the scenario to monitor is a split verdict: Seoul High Court may uphold the ₩162.8B fine on the review-manipulation count while partially excusing the algorithm-preferencing count under the evolving Naver precedent. That would put actual cash outflows around ₩80–100 billion — material but more digestible than the full liability.

The broader Korean platform sector — including NHN (181710.KS), KAKAO (035720.KS), and NAVER (035420.KS) — continues to trade below Western peers partly on regulatory uncertainty. The current appellate cycle is producing a more structured, less aggressive enforcement framework than feared. For investors with long KOSPI tech exposure, the direction is favorable.

Sources: Chosun Biz — 법조 인사이드 알고리즘 자사 우대