Shinhan Financial Group055550.KS

About Shinhan Financial Group

Shinhan Financial Group ranks among South Korea's largest bank-holding companies, with Shinhan Bank at its center alongside a credit-card unit that leads the domestic card market, plus securities, life insurance, and asset-management subsidiaries. The group traces its roots to founding investment by the Korean-Japanese business community, an unusual heritage among Korean lenders. Net interest income from bank lending generates most profit, with card fees and capital-markets income providing diversification. Shinhan has also built one of the larger overseas footprints among Korean banks, operating in Vietnam, Japan, and other markets, though domestic business still dominates.

With no controlling shareholder, board composition and chief-executive succession are decided among institutional owners, and foreign investors have long held a substantial share of the register. The structural drivers are those of Korean banking generally: net-interest-margin sensitivity to policy rates, household-lending regulation, and supervisory limits that govern how much capital can be returned. Shinhan was an early mover among Korean banks in adopting quarterly dividends and share cancellations, anchoring its appeal to income-focused funds. Its Vietnamese and other Asian operations offer a modest growth offset to a saturated home market, a differentiator investors weigh against peers.

Shinhan Bank opened in 1982, founded with capital raised from Korean-Japanese businesspeople, making it Korea's first bank established purely with private capital in the modern era. In 2001 it formed the country's first private financial holding company, Shinhan Financial Group, and scale came quickly: the 2003 acquisition of Chohung Bank, whose lineage reaches back to 1897, the purchase of LG Card in 2007 after that issuer's crisis, and the 2019 acquisition of Orange Life, later folded into Shinhan Life. The group thus combines Korea's oldest banking roots with a comparatively young, acquisition-built corporate structure.

Earnings mechanics start with the bank, which gathers low-cost retail and corporate deposits and lends across mortgages, consumer credit, and business loans, earning the interest spread. Shinhan Card, the largest domestic card issuer, adds merchant fees and installment-finance income; securities and insurance units contribute brokerage, underwriting, and protection-product margins. A distinguishing feature is the overseas network, notably Shinhan Bank Vietnam, one of the largest foreign banks there, which gives the group an emerging-market growth channel most Korean peers lack. Customers remain predominantly Korean households and firms, so domestic rate cycles and household-lending rules set the earnings tempo, with capital returns governed by supervisory buffers.

Company profile by LineVest editorial. Journalism, not investment advice. Commission a full DART-based report on Shinhan Financial Group →

Shinhan Financial Group coverage

4 articles

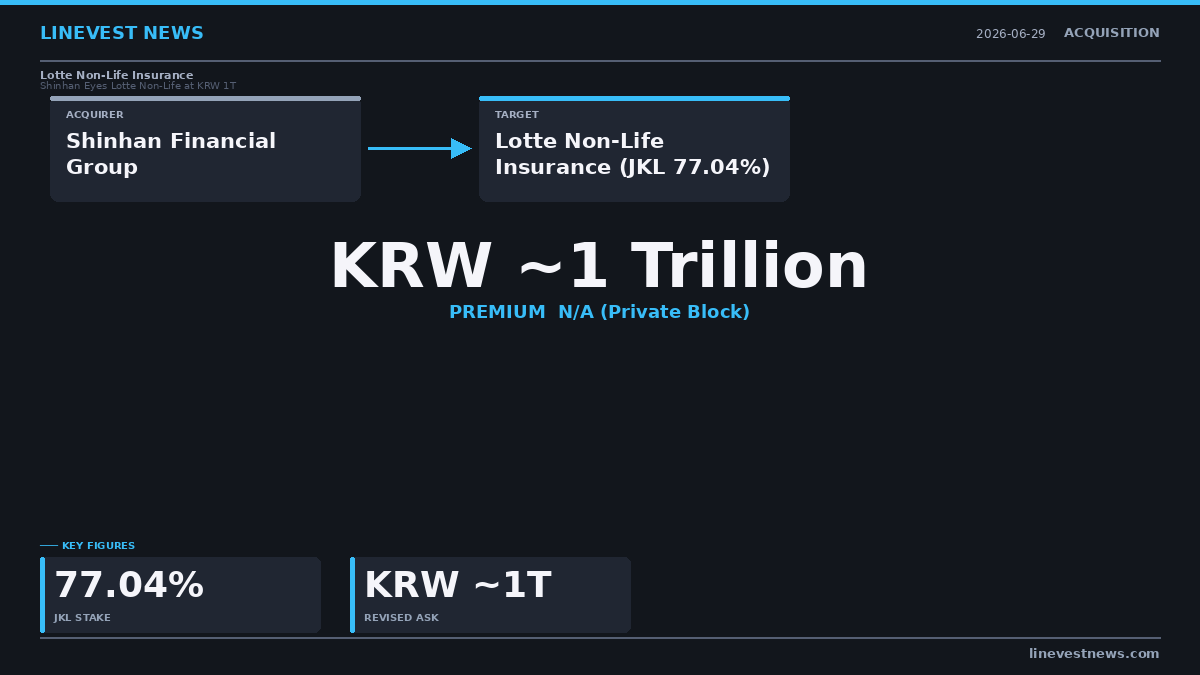

Shinhan Financial Weighs Lotte Non-Life Insurance Buyout at KRW 1 Trillion as JKL Cuts Ask in Half

Shinhan Financial Group reviews acquisition of Lotte Non-Life Insurance at KRW 1 trillion as JKL Partners halves asking price, sending shares to the daily upper limit of +30%.

Shinhan (055550.KS) Embeds AI Into Group Compliance System

Premium

PremiumShinhan Financial (055550.KS) Q1 2026: ₩1.62T Profit Lifted by 26% Non-Interest Surge as NPL Ticks Up

Shinhan Financial Group (055550.KS) — FY2025 Financial Analysis

Frequently asked questions

What does Shinhan Financial Group do?

Shinhan Financial Group is one of South Korea's largest banking groups, built around Shinhan Bank and the country's leading credit-card company, with securities, life insurance, and asset-management subsidiaries. It earns mainly interest income from lending, supplemented by card fees and capital-markets revenue, and operates a notable overseas network including Vietnam.

Who controls Shinhan Financial Group?

There is no controlling shareholder. The register is dominated by institutional investors, including Korea's National Pension Service and long-standing foreign holders, with a heritage bloc of Korean-Japanese investors dating to the bank's founding. Board committees manage CEO succession, a process investors watch closely given the dispersed ownership.

How can foreign investors get exposure to Shinhan Financial Group?

The stock trades on the Korea Exchange under ticker 055550, and American depositary receipts are listed on the New York Stock Exchange. Either route provides direct ownership, while Korea-focused ETFs and Asian bank-sector funds offer indirect exposure, typically holding Shinhan among their larger financial positions.

Answers are editorial summaries for general information, not investment advice.

Go deeper than the headline

You just read what happened. Here's how to read what it means.

The Korean market week, in one email

Every Saturday: the week's key KOSPI & KOSDAQ stories, earnings and foreign flows — picked from our daily coverage. Free, no card required.

Want it every morning before the open? LineVest Daily — $2.99/mo →

Full report on Shinhan Financial Group

We read Shinhan Financial Group's latest DART filing in full — financials under K-IFRS, governance, and what it means for the stock. PDF in your inbox within 3 hours.

$12 · one-time

Get the Shinhan Financial Group reportFollow the whole market

Reading several Korean stocks a week? Read every analysis article the moment it publishes — full daily KOSPI & KOSDAQ coverage plus the 90-day archive.

$9.99 · monthly

SubscribeIndependent journalism based on primary DART filings — not investment advice. No brokerage affiliation.