Emart139480.KS

About Emart

Emart is Korea's largest hypermarket operator and the retail workhorse of the Shinsegae group, running big-box stores, the warehouse club Traders, specialty formats built around its No Brand private label, and the Emart24 convenience chain. Its consolidated reach extends to e-commerce through SSG.com and Gmarket, to food service and hotels, and to a controlling interest in the company that operates Starbucks in Korea. The group shares Samsung founding-family roots, and Emart is led by one sibling of the controlling Chung family while department-store operator Shinsegae is separately listed. Grocery-led store sales remain the cash engine funding the broader portfolio.

Investors approach Emart as a sum of parts under repair: a mature hypermarket core defending against online grocery rivals, e-commerce ventures whose path to profitability shapes group value, and steady contributors like the Starbucks operation. Structural questions include leverage taken on for acquisitions, potential asset sales or listings within the portfolio, and regulation that restricts large-store operating days to protect small merchants. The family division of retail assets between siblings defines the governance map. Domestic consumption is the overriding macro driver.

Emart's story begins inside Shinsegae: the group opened Korea's first discount store under the Emart name in Seoul's Changdong district in 1993, betting that hypermarkets would follow department stores as the country's dominant retail format. The bet paid off, and in 2011 Shinsegae split itself in two, spinning the discount store division off as a separately listed Emart. The new company then expanded on multiple fronts, building the Traders warehouse club format, lifting its stake in Starbucks' Korean operation to a controlling majority in 2021, buying the Gmarket e-commerce platform that same year, and earlier exiting its store network in China.

Hypermarket economics rest on purchasing scale and traffic: Emart buys grocery volume no domestic store rival can match, layers on private labels such as No Brand and Peacock that capture extra margin, and uses fresh food to draw the visits that sell everything else. The consolidated model routes that traffic advantage into adjacent formats, with Traders offering a low-price warehouse alternative, Emart24 pursuing convenience, and SSG.com and Gmarket extending the franchise online, fulfilled partly from store back rooms. Property ownership beneath many stores anchors the balance sheet, while competitive pressure concentrates in online grocery, where dedicated e-commerce players attack the core basket.

Company profile by LineVest editorial. Journalism, not investment advice. Commission a full DART-based report on Emart →

Emart coverage

2 articles Premium

PremiumE-Mart (139480.KS) Q1 2026: Operating Profit Hits 14-Year High While Net Income Slips 5%

E-Mart (139480.KS) Q1 2026: Operating Profit Hits 14-Year High While Net Income Slips 5%

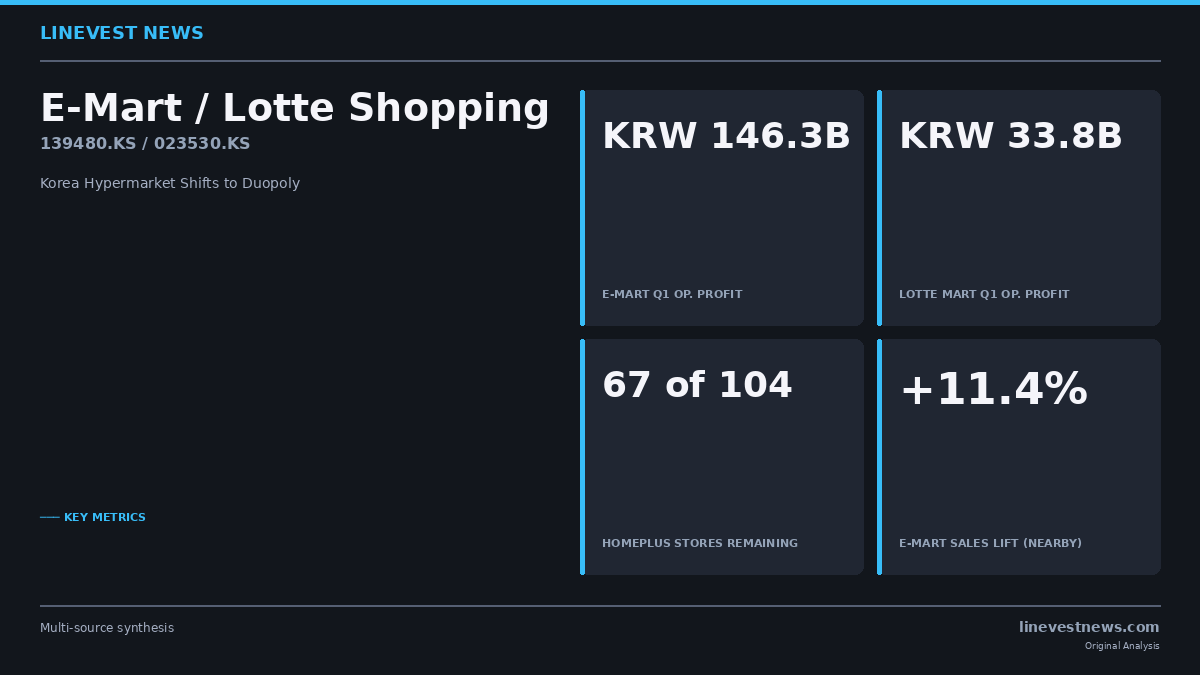

E-Mart and Lotte Shopping Race to Lock In Homeplus Customers as Korea Hypermarket Shifts to Duopoly

With Homeplus closing 37 stores in June, E-Mart and Lotte Shopping are already posting double-digit nearby-store sales gains. Korea's hypermarket sector is restructuring to a duopoly — and the full benefit has yet to hit Q2 earnings.

Frequently asked questions

What does Emart do?

Emart is Korea's largest hypermarket chain, selling groceries and general merchandise through big-box stores, the Traders warehouse club, and Emart24 convenience stores. Consolidated operations include the SSG.com and Gmarket e-commerce platforms, the company operating Starbucks in Korea, food service, and hotel interests.

Who controls Emart?

Chung Yong-jin, part of the family that controls the Shinsegae group and a descendant of Samsung's founding family, is the controlling shareholder of Emart. The group's retail assets were divided within the family, with his sibling overseeing the separately listed Shinsegae department store company.

How can foreign investors get exposure to Emart?

Emart lists on the Korea Exchange's KOSPI market under ticker 139480. Foreign investors can purchase shares through brokers providing Korean market access after registering, and the stock appears in Korea retail and large-cap index funds. Its department store counterpart, Shinsegae, trades separately under its own code.

Answers are editorial summaries for general information, not investment advice.

Go deeper than the headline

You just read what happened. Here's how to read what it means.

The Korean market week, in one email

Every Saturday: the week's key KOSPI & KOSDAQ stories, earnings and foreign flows — picked from our daily coverage. Free, no card required.

Want it every morning before the open? LineVest Daily — $2.99/mo →

Full report on Emart

We read Emart's latest DART filing in full — financials under K-IFRS, governance, and what it means for the stock. PDF in your inbox within 3 hours.

$12 · one-time

Get the Emart reportFollow the whole market

Reading several Korean stocks a week? Read every analysis article the moment it publishes — full daily KOSPI & KOSDAQ coverage plus the 90-day archive.

$9.99 · monthly

SubscribeIndependent journalism based on primary DART filings — not investment advice. No brokerage affiliation.