Samsung Electronics (005930.KS) has reclaimed the global smartphone market leadership in the second quarter of 2026, surpassing Apple for the first time since Q4 2025, according to Counterpoint Research data released Monday. The reversal comes as Samsung's AI-centric device strategy helped it weather the worst second-quarter smartphone market in 13 years — while the company separately denied a Bloomberg report that it was exploring a U.S. ADR listing.

TL;DR

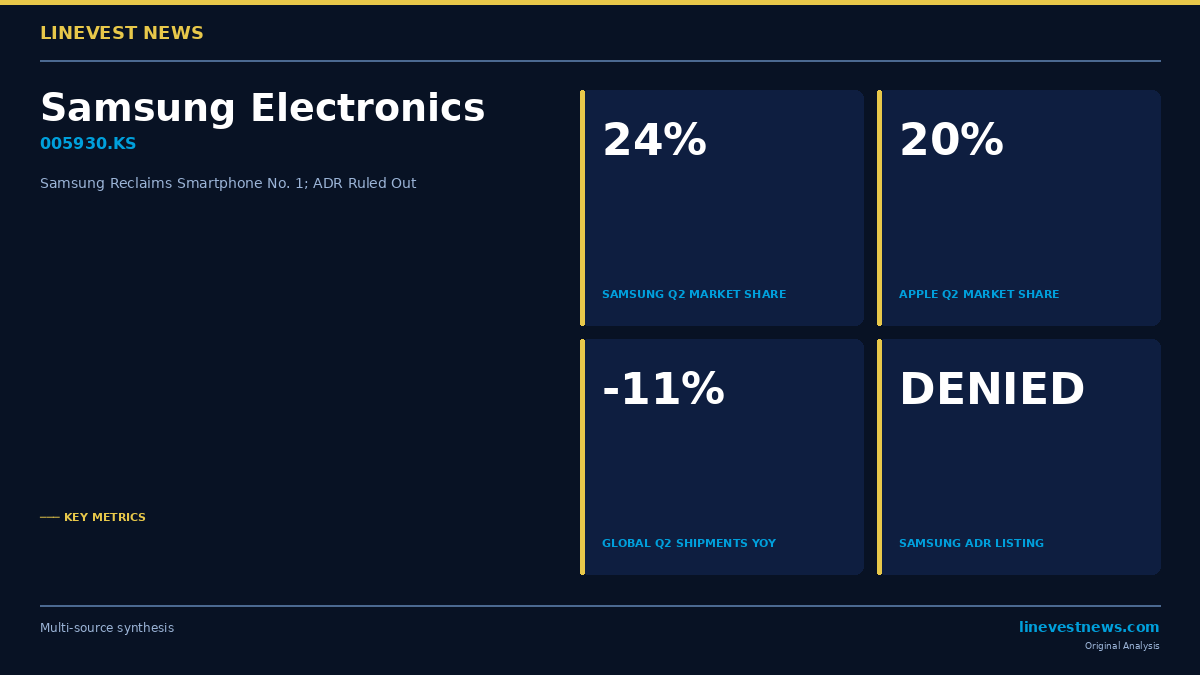

- Samsung returns to No. 1: 24% global smartphone market share in Q2 2026, versus Apple at 20%

- Market in contraction: Global Q2 shipments fell 11% year-on-year — the steepest Q2 decline since 2013

- Cause: AI datacenter memory demand has squeezed DRAM and NAND supply for handsets, driving up smartphone bill-of-materials costs and suppressing consumer demand

- ADR ruled out: Samsung flatly denied a Bloomberg report it was exploring a U.S. depository receipt listing: "We are not reviewing it"

Part A — What Happened

Market Share: Samsung 24%, Apple 20%

Counterpoint Research's preliminary Q2 2026 data show Samsung Electronics capturing 24% of global smartphone shipments, edging past Apple's 20%. The ranking reversal ends a three-quarter run of Apple atop the chart, which had coincided with the iPhone 16 Super cycle and Samsung's underwhelming Galaxy S25 launch in early 2025.

The aggregate market backdrop was stark: global Q2 2026 smartphone shipments shrank 11% year-on-year, the weakest second-quarter performance since 2013. The firm's analysts attribute the contraction primarily to a memory supply crunch driven by AI infrastructure demand — a dynamic that has paradoxically boosted Samsung's DS (Device Solutions) semiconductor division while pressuring the MX (Mobile eXperience) handset business.

| Metric | Q2 2026 | vs. Q2 2025 |

|---|---|---|

| Global shipments (YoY) | –11% | Worst Q2 since 2013 |

| Samsung market share | 24% (#1) | Up from ~20% |

| Apple market share | 20% (#2) | Down from ~23% |

ADR Denial

Bloomberg reported late Sunday (U.S. time) that Samsung had begun preliminary discussions with financial institutions about issuing U.S. American Depositary Receipts — a move that would mirror SK Hynix's record $26.5 billion Nasdaq ADR completed July 10. A Samsung spokesperson on July 14 flatly denied the report: "We are not reviewing it. Our situation is different."

Industry analysts had noted the same day that Samsung's existing ADR program on the over-the-counter market (SSNLF) carries low trading liquidity and lacks the exchange listing that SK Hynix's SKHY now has on Nasdaq. Samsung has historically resisted the disclosure burden of a full U.S. exchange listing.

Part B — Korean Market Implications

The MX Paradox: Volume Share Up, Margins Under Pressure

Samsung's smartphone volume recovery masks a widening profit challenge in the MX division. A Samsung Securities analyst note published July 9 projected FY2026 operating losses for the combined MX and Network units of approximately ₩5.84 trillion — a stunning reversal from a ₩3.41 trillion profit forecast issued at the start of the year. Over 2026–2028, the cumulative projected loss is estimated at ₩24 trillion.

The pressure stems from the same AI-driven memory shortage that is propelling Samsung's DS division. As HBM and high-density DRAM commands premium prices, conventional mobile DRAM and storage NAND for handsets have become increasingly scarce and costly. Samsung's Galaxy S26 series incorporates more on-device AI memory than its predecessor, pushing up per-unit DRAM costs at a time when the company cannot easily transfer that cost increase to consumers.

This creates a structural bifurcation within Samsung's conglomerate: the DS semiconductor segment generated an estimated ₩89.4 trillion in Q2 operating profit (record), while MX absorbs rising input costs from the same supply chain. For equity investors, this means Samsung's headline numbers will continue to be dominated by the memory super-cycle even as the consumer electronics arm contracts in profit terms.

Why Samsung Is Winning Volume Despite Cost Headwinds

Samsung's relative outperformance versus Apple in Q2 units appears driven by three factors:

Galaxy AI differentiation: The Galaxy S26 platform, anchored by Samsung's on-device Gauss 2 model and tighter integration with Google Gemini, has resonated in mid-to-premium Android segments where AI features represent genuine differentiation. DX Division head Noh Tae-moon's July 22 Galaxy Unpacked preview — "The best experience comes not from the smartest model, but from the device that knows you best" — signals Samsung is positioning AI as a platform rather than a spec-sheet feature.

Geographic resilience: Samsung maintains dominant share in Southeast Asia, India, and Latin America, regions where iPhone penetration is structurally capped by price. Apple's strength in North America and China was insufficient to offset Samsung's breadth in the current demand environment.

Apple cycle timing: The Q2 period typically precedes Apple's annual iPhone launch (expected September 2026), creating a seasonal lull in iPhone demand that Samsung benefits from in unit rankings.

The ADR Contrast with SK Hynix — and What It Means

Samsung's denial of ADR ambitions is strategically notable given SK Hynix's record-breaking success: SKHY priced at $149 on Nasdaq July 10, opened 14% higher, and will deploy the ₩39.6 trillion ($26.5B) proceeds toward a new Yongin fab for HBM production.

Samsung's pushback reflects a genuine difference in capital needs: Samsung already carries one of the largest cash and investment portfolios of any listed company globally, and the existing 005930.KS share structure on the KRX is broadly accessible via GDRs. The company does not face the same capital-raise imperative that justified SK Hynix's ADR route.

For KOSPI investors, Samsung's ADR denial removes one potential near-term catalyst while the SK Hynix precedent confirms that Korean chip names can unlock valuation from global capital markets when the business case is specific and concrete.

Investment Takeaway

Samsung Electronics (005930.KS) continues to present a sum-of-parts complexity that rewards analysis at the division level. The DS semiconductor segment's HBM super-cycle is a structural tailwind for 2026–2027. The MX unit's market share recovery in volume terms is real, but masks meaningful margin pressure. The ADR denial removes a short-term re-rating catalyst but is not negative for the underlying business.

The Q2 global smartphone contraction of 11% — the worst since 2013 — is a macroeconomic signal that consumer electronics spending is being displaced by AI infrastructure investment cycles. Korean hardware companies (Samsung, LG Electronics) with the scale to serve both AI infrastructure and consumer markets are relatively insulated versus pure-play handset peers.

Disclosure: This article is for informational purposes only and does not constitute investment advice. LineVest News is an independent publication and holds no positions in the securities discussed.

Sources: - Counterpoint Research Q2 2026 Smartphone Market Share (via ETNews, July 14 2026) - Samsung Denies ADR Listing (MK Economy, July 14 2026) - Global Smartphone Shipments Fall 11% (ETNews, July 14 2026) - Bloomberg: Samsung Exploring ADR (Bloomberg, July 13 2026) - Samsung's AI Phone Strategy at Galaxy Unpacked (Korea Herald, July 8 2026)