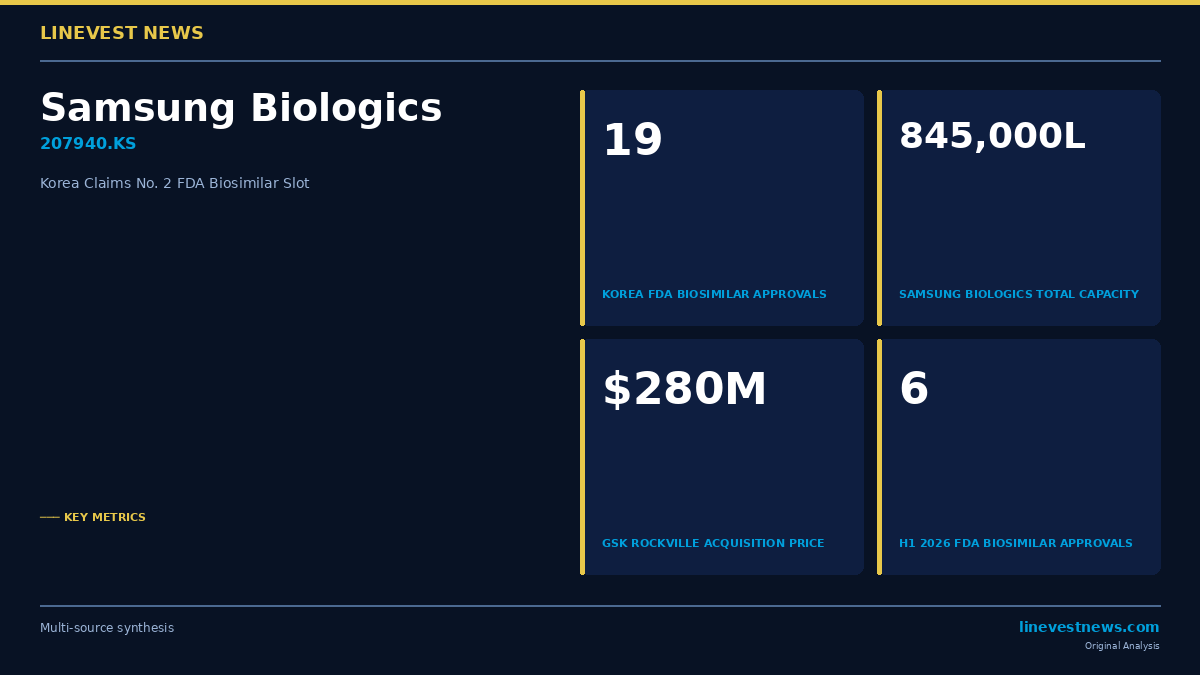

South Korea retained its position as the world's second-largest source of FDA-approved biosimilars as the first half of 2026 delivered a quieter-than-expected six new clearances — a marked step down from the 18 granted in each of 2024 and 2025 — while Samsung Biologics (207940.KS) reinforced its global credentials by completing a $280 million acquisition of GlaxoSmithKline's biologics campus in Rockville, Maryland.

Part A — Regulatory Snapshot

The U.S. Food and Drug Administration published its H1 2026 biosimilar tally on July 1, confirming six approvals against a cumulative portfolio of 87 products cleared since the market opened in 2015. Korea accounts for 19 of those 87 — a 21.8% global share — trailing only the United States (31) and running well ahead of India (12), Germany (8), Switzerland (7), and China (4). Samsung Biologics and Celltrion (068270.KS) are the two Korean anchor companies behind that tally.

H1 2026 Notable Clearances

The six first-half approvals included a milestone: Immgolis (golimumab-sldi) and Immgolis Intri, developed by Bio-Thera Solutions and distributed in the U.S. by Accord BioPharma, became the first-ever biosimilars to reference Johnson & Johnson's Simponi (golimumab) following FDA clearance on May 15. The drug, used across rheumatoid arthritis, psoriatic arthritis, and ankylosing spondylitis, had remained copycat-free since its 2009 approval despite significant market scale. Other H1 approvals included Shionogi's Ennumo (pegfilgrastim-pccg), referencing Amgen's Neulasta for chemotherapy-related neutropenia, and Teva's Ponlimsi (denosumab-adet), referencing Amgen's Prolia.

The headline deceleration is largely structural: the highest-volume reference drugs — Humira (10 biosimilars), Prolia/Xgeva (10), Stelara (8), and Neulasta (8) — have already attracted multiple competitive entrants, reducing the marginal incentive for new filers. Analysts expect the H2 2026 slate to skew toward more complex molecules, including PD-1 and IL-17 inhibitors where clinical bridging requirements remain more demanding.

Part B — Samsung Biologics and the U.S. Pivot

Samsung Biologics Completes $280M GSK Rockville Deal

On March 31, 2026, Samsung Biologics formally completed the acquisition of the former Human Genome Sciences biologics campus in Rockville, Maryland, which GSK had operated since its 2012 acquisition of HGS. The purchase price was USD 280 million (approximately KRW 385 billion at prevailing exchange rates), with more than 500 legacy employees transferred to the new Samsung subsidiary.

The Rockville site adds 60,000 liters of licensed drug substance capacity through two current Good Manufacturing Practice (cGMP) facilities, pushing Samsung Biologics' aggregate global bioreactor volume to 845,000 liters — the largest installed CDMO capacity in the world by a wide margin. The site carries more than 62 regulatory manufacturing approvals from the FDA and EMA, providing immediate production-ready status for multiple commercial programs.

Why the U.S. Footprint Matters

Proximity to major U.S. biotech clients cuts lead times for clinical supply by four to six weeks compared with Korean-based fulfillment, a meaningful advantage in Phase 3 programs on aggressive IND-to-NDA timelines. The domestic U.S. origin argument also resonates commercially: buyers who experienced supply disruptions during 2022–2023 are increasingly inserting contractual preferences for allied-nation manufacturing following legislative scrutiny of non-allied-country CDMOs under the BIOSECURE Act framework. Samsung Biologics expects the Rockville site to command a 15–20% capacity price premium over equivalent Korean-origin batches.

Celltrion's H2 Pipeline

Celltrion is positioned for a busier second half. Its Eydenzelt (aflibercept-jbvf), a biosimilar referencing Regeneron's Eylea — global annual sales above USD 9 billion before the 2024 high-dose shift — received FDA approval in October 2025 and is contractually permitted to launch in the United States on December 31, 2026 under a settlement with Regeneron. In June 2026, Celltrion filed with Health Canada for CT-P55, a biosimilar of Novartis' Cosentyx (secukinumab), covering plaque psoriasis, psoriatic arthritis, and ankylosing spondylitis — a drug franchise generating approximately USD 5.5 billion in annual global sales.

Investor Implications

For Samsung Biologics, the biosimilar approval count functions as an institutional-credibility signal rather than a direct revenue driver: the company's core business model is CDMO services, not proprietary drugs. The Rockville acquisition is primarily a capacity and pricing story. CDMO revenue per liter is structurally higher in the U.S. than in Korea, and the facility diversifies Samsung Biologics' geographic exposure ahead of a potential listing review cycle.

For Celltrion, the Eylea biosimilar launch window — December 2026 — represents the largest new commercial opportunity in the company's pipeline. Aflibercept biosimilars have demonstrated rapid market penetration in European markets where originator exclusivity lapsed earlier; U.S. uptake timelines are historically faster when launch follows settlement rather than litigation.

Korea's 19-approval portfolio, backed by on-the-ground U.S. manufacturing and two active commercial pipelines, positions Samsung Biologics and Celltrion distinctly from most emerging-market CDMO peers at a time when Western pharma buyers are actively diversifying out of Chinese API and fill-finish networks.

Sources: Samsung Biologics — Rockville Acquisition · FiercePharma · PharmaSource · Center for Biosimilars · PharmaShots · Korea Biomed Reporter