TL;DR - South Korea's FSC tripled the minimum deposit for Samsung and SK Hynix single-stock leveraged ETFs from ₩10 million to ₩30 million (~USD 20,300), effective August 5, 2026 - New single-stock leveraged ETF listings are halted immediately; minimum trading unit rises 20-fold to 20 shares by November - So-called "SamNick" funds (Samsung + SK Hynix) attracted ₩7.34 trillion (~$4.96 billion) in total net inflows in a single month — while the underlying stocks fell 19–25%, pushing the 2× products down 45–48% - The FSC projects the combined SamNick market will shrink from ~₩12 trillion (~$8.1B) to ₩4–5 trillion post-regulation

What the FSC Did

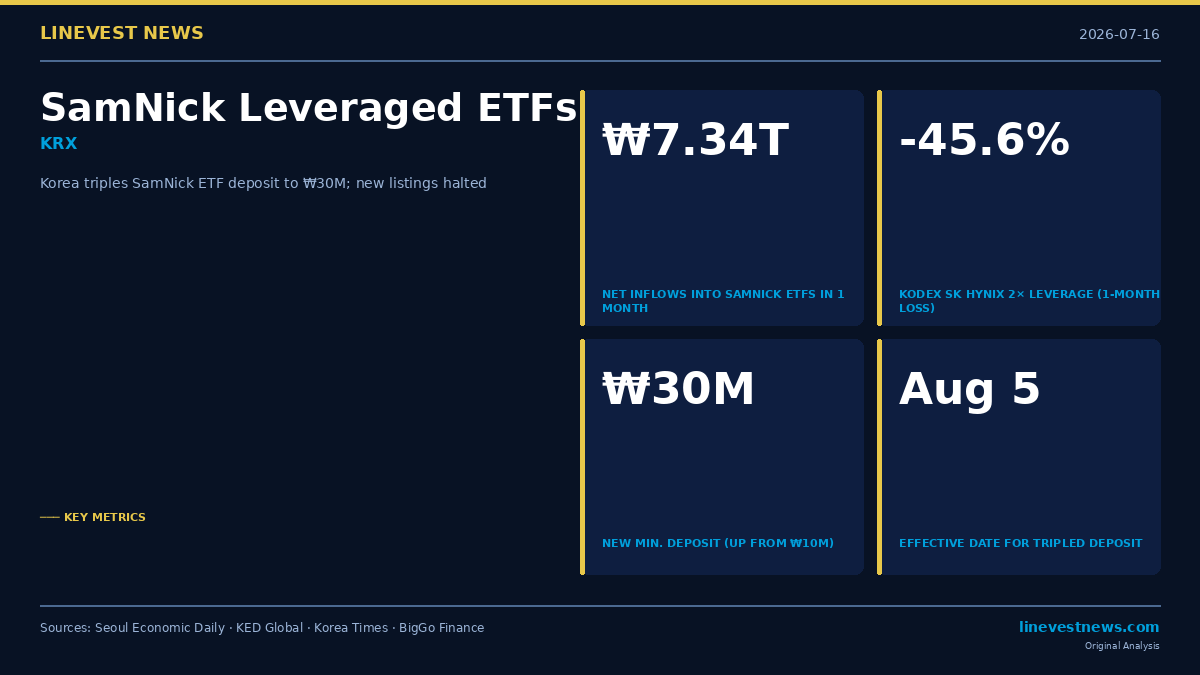

On July 16, 2026, South Korea's Financial Services Commission (FSC), presided over by Finance Minister and Deputy Prime Minister Koo Yun-cheol, announced sweeping restrictions on single-stock leveraged and inverse exchange-traded funds — products that had been live for just 50 days.

Launched on May 27, 2026, sixteen single-stock leveraged and inverse ETFs tied to Samsung Electronics (005930.KS) and SK Hynix (000660.KS) quickly became the defining retail trade of mid-2026 Korea. Dubbed "SamNick" — a portmanteau of "Samsung" and "Hynix" — the products allowed retail investors to bet 2× on their semiconductor convictions without a derivatives account.

Regulatory changes at a glance:

| Measure | Before | After | Effective Date |

|---|---|---|---|

| Minimum cash deposit | ₩10M (~$6,800) | ₩30M (~$20,300) | Aug 5, 2026 |

| Deposit form accepted | Cash + substitute securities | Cash only | Aug 19, 2026 |

| Minimum trading unit | 1 share | 20 shares | Nov 2026 |

| Pre-trade training | 2 hours | 3 hours (re-test if score <60) | Aug 2026 |

| Liquidity provider tracking error | 3% | 2% | Immediate |

| New single-stock leveraged ETF listings | Allowed | Halted | Immediate |

FSC Director Byun Je-ho stated that the cash-only deposit requirement is "expected to significantly contribute to easing demand" beyond the threshold increase alone. The regulatory action involved the FSC, Financial Supervisory Service (FSS), Ministry of Finance, Bank of Korea, and Korea Exchange (KRX).

Why This Matters — and What Comes Next

The Numbers Behind the Crackdown

The scale of the retail rush into SamNick funds explains why regulators acted in under two months. According to Korea Exchange data compiled by Seoul Economic Daily, the 16 products attracted ₩7.3364 trillion (~$4.96 billion) in total net inflows between June 16 and July 15, 2026.

Top SamNick ETF inflows (June 16–July 15, 2026):

| ETF | Net Inflow | Approx. USD |

|---|---|---|

| KODEX SK Hynix Single-Stock Leverage | ₩3.4472T | $2.33B |

| KODEX Samsung Electronics Single-Stock Leverage | ₩1.5083T | $1.02B |

| TIGER SK Hynix Single-Stock Leverage | ₩1.4271T | $0.96B |

| TIGER Samsung Electronics Single-Stock Leverage | ₩693.8B | $0.47B |

The KODEX SK Hynix product logged the largest net inflow of any ETF listed in Korea during the period. Individual retail investors were the primary buyers, accumulating ₩4.24 trillion net into SK Hynix leveraged products and ₩1.61 trillion net into Samsung leveraged products. The ₩7.34 trillion aggregate spans all 16 products in the SamNick family, including inverse instruments and purchases by a broader set of market participants.

The Loss Column

The money poured in even as the underlying stocks fell sharply. Between June 16 and July 16:

| Instrument | Return (1 month) |

|---|---|

| SK Hynix (000660.KS) | −19.49% |

| Samsung Electronics (005930.KS) | −24.33% |

| KODEX SK Hynix Single-Stock Leverage | −45.60% |

| KODEX Samsung Electronics Single-Stock Leverage | −48.44% |

Both products fell below their launch price of ₩20,000 per unit. A retail investor who placed ₩30 million into the KODEX SK Hynix Leverage ETF on June 16 held approximately ₩16.3 million by July 16 — a paper loss of roughly ₩13.7 million in 30 days.

What the ₩30 Million Floor Actually Does

The tripled deposit requirement is blunt by design. At ₩30 million (~USD 20,300), the deposit is equivalent to several months of take-home pay for most Korean salaried workers, and roughly a full year of savings for many middle-income households. The FSC's stated goal is to limit access to investors with genuine risk capacity.

The shift to cash-only collateral is the sharper constraint. Previously, investors could post existing equity or bond holdings as substitute securities, allowing a fully invested portfolio to access 2× leverage without liquidating positions. Under the new rules, ₩30 million in idle cash must be set aside before purchasing a single unit of a SamNick ETF.

The FSC projects the combined SamNick market — currently approximately ₩12 trillion (~$8.1 billion) — will contract to ₩4–5 trillion once the full ruleset is in force by November 2026.

Implications for International Investors

For non-Korean investors accessing Korea's chip sector, the FSC rules have no direct application: the deposit requirements apply only to KRX-listed leveraged products accessible through Korean brokerage accounts. However, three indirect signals matter:

1. A retail sentiment gauge goes quiet. SamNick fund flows served as a real-time indicator of domestic investor appetite for semiconductor stocks. If the ₩12T pool contracts to ₩4–5T, a visible "retail conviction" signal in the KOSPI diminishes — potentially reducing reflexive buying support during selloffs.

2. Rotation to unleveraged Korea proxies. Bloomberg reported that the iShares MSCI South Korea ETF (EWY) logged a record $281 million single-day inflow on July 16, the same day the leveraged ETF rules were announced, as investors rotated into the unleveraged benchmark vehicle.

3. Tighter tracking means truer price discovery. The liquidity provider tracking error tightened from 3% to 2%, which means SamNick ETFs will more faithfully mirror intraday moves in 000660.KS and 005930.KS — reducing basis risk for arbitrageurs who use the products as hedging instruments.

The Broader Pattern

The SamNick crackdown follows a familiar Korean regulatory cycle. Korea introduced single-stock leveraged ETFs in May 2026 — later than most developed markets — and is already among the fastest to restrict them. Seoul Economic Daily noted that regulators invoked lessons from the 2010s derivatives market dislocations, when aggressive retail positioning in structured products contributed to market instability.

For investors tracking the KOSPI, the key calendar:

| Date | Event |

|---|---|

| Aug 5, 2026 | New ₩30M deposit minimum effective |

| Aug 19, 2026 | Cash-only collateral requirement effective |

| Nov 2026 | Minimum trading unit rises from 1 to 20 shares |

This article is for informational purposes only and does not constitute investment advice. All figures are sourced from Korea Exchange, FSC announcements, Seoul Economic Daily, KED Global, Korea Times, and BigGo Finance. Exchange rate used: approximately ₩1,480/USD 1.

Sources: - Korea tightens rules on single-stock leveraged ETFs — KED Global - Samsung-Hynix Single-Stock Leverage ETFs Draw 7 Trillion Won — Seoul Economic Daily - South Korea Slams Brakes on 'SamNick' Leveraged ETFs — BigGo Finance - Korea triples single-stock leveraged ETF deposit — Korea Times - South Korea Halts New Listings of Single-Stock Leveraged ETFs — Bloomberg - Korea ETF (EWY) Record Inflow Fuels SK Hynix Proxy Play — Bloomberg