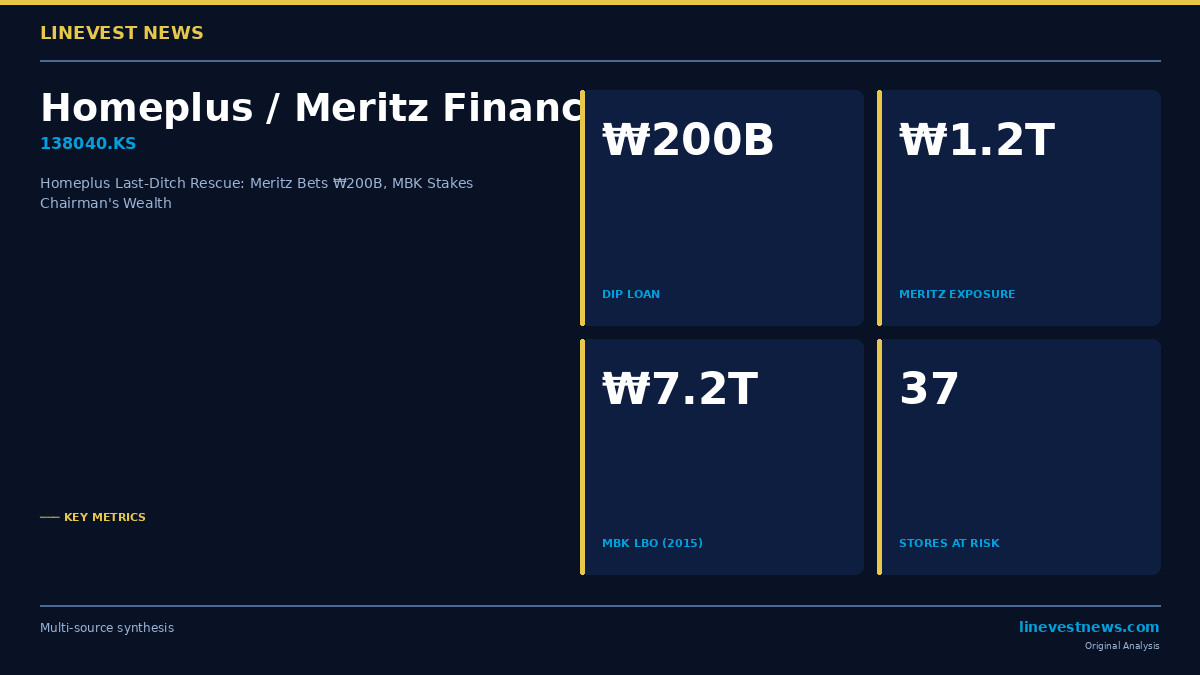

TL;DR - Meritz Financial Group approved a ₩200 billion (~USD 135 million) debtor-in-possession loan on July 16, 2026, giving Homeplus a narrow window to appeal the Seoul court's July 3 termination of its rehabilitation. - MBK Partners chairman Kim Byung-ju agreed to provide a full personal guarantee for the loan — an extraordinary concession that signals how desperate the rescue had become. - Meritz (138040.KS) carries roughly ₩1.2 trillion in total Homeplus exposure; its NPL ratio had already risen to 6.9% at end-2025, and a disorderly liquidation would accelerate further deterioration.

Part A — What Happened

A Hypermarket Giant on the Edge

Homeplus was once South Korea's second-largest hypermarket chain. At its peak it operated 146 stores. Today it has 67 — and on the week of July 14, 2026, all of them briefly went dark.

The proximate cause was a funding standoff. Homeplus entered court-led rehabilitation in March 2025 after its leveraged balance sheet — a legacy of MBK Partners' ₩7.2 trillion (~USD 5.7 billion) leveraged buyout in 2015 — could no longer sustain rising fixed costs estimated at ₩1.21 trillion annually. After 16 months, the Seoul Bankruptcy Court terminated the restructuring process on July 3, ruling that the retailer had failed to secure the minimum ₩200 billion in operating funds required under its turnaround plan. Thirty-seven stores were left temporarily closed, 12,000 direct employees and over 1,000 indirect workers faced an uncertain future.

The ₩200 Billion Deal

On July 16, 2026, Meritz Financial Group — Homeplus's largest creditor — formally approved the ₩200 billion debtor-in-possession loan. The loan was described by the court and both parties as the bare minimum needed to sustain operations and file a credible rehabilitation appeal.

The critical sticking point had been collateral. Meritz initially demanded full guarantees, citing exposure and liability concerns. MBK Partners ultimately agreed: both the firm and chairman Kim Byung-ju will jointly guarantee the entire ₩200 billion. A National Assembly hearing on the wider crisis is scheduled for July 27.

With the July 20, 2026 appeal deadline looming, Homeplus said it would file its appeal on Monday. If the Seoul Bankruptcy Court accepts the restart, 37 temporarily closed stores would reopen on schedules to be worked out with partner companies. NS Shopping's acquisition of the Homeplus Express convenience format received antitrust clearance in June 2026.

| Milestone | Date |

|---|---|

| MBK Partners acquires Homeplus (LBO) | 2015 |

| Court rehabilitation filing | March 2025 |

| Seoul court terminates rehabilitation | July 3, 2026 |

| All stores briefly shut nationwide | July 14, 2026 |

| Meritz approves ₩200B DIP loan | July 16, 2026 |

| Appeal deadline | July 20, 2026 |

| National Assembly hearing | July 27, 2026 |

Part B — Market and Investment Analysis

Meritz Financial Group: The Creditor in the Crosshairs

Meritz Financial Group (138040.KS) is the most directly exposed listed company in this saga. Its ~₩1.2 trillion total exposure to Homeplus has been the overhang on the stock since early 2025. The group's consolidated non-performing loan ratio already surged to 6.9% at the end of 2025 — a sharp deterioration attributed to Homeplus and soured domestic and overseas alternative investments — before this latest episode unfolded.

Meritz's core units, Meritz Fire & Marine Insurance and Meritz Securities (capital base ₩7.8 trillion as of March 2026), remain profitable. The group also recently launched a ₩280 billion bond sale, partly to manage its balance sheet in the context of this exposure. The key question for investors is whether the DIP loan leads to a genuine rehabilitation — in which case the ₩1.2 trillion is slowly recovered — or a protracted legal dispute that accelerates provisioning.

The personal guarantee from MBK's Kim Byung-ju changes the risk calculus. If the rehabilitation is approved and succeeds, Meritz's exposure is backstopped by both the PE firm and its chairman's personal assets. If the court declines the appeal, Meritz faces a contested liquidation with ₩1.0 trillion in Korean bank claims also in the queue (₩900 billion secured).

MBK Partners: Korea's Most Costly LBO in the Making

MBK Partners entered Homeplus at a ₩7.2 trillion enterprise valuation in 2015 — one of the largest Korean retail buyouts in history. Over the following decade, e-commerce penetration in South Korea accelerated dramatically while hypermarket footfall declined, leaving Homeplus with an oversized, expensive physical network.

The deal is increasingly described in local financial media as one of the costliest in MBK's history. Chairman Kim's decision to provide a personal guarantee — a move essentially without precedent for a founder of a top-tier Asian PE firm — underlines how much political and reputational pressure the firm is under. A National Assembly probe and fraud investigation (though the court declined to issue an arrest warrant in January 2026) add legal dimensions that few PE exits can absorb quietly.

Korean Banking System: The ₩1 Trillion Watch List

Korean commercial banks collectively hold approximately ₩1 trillion in Homeplus exposure, with roughly ₩900 billion on a secured basis. While that figure is manageable against the total assets of Korea's major lenders, a disorderly liquidation — which is what the July 3 court ruling initially threatened — would have required banks to reclassify collateral and accelerate NPL provisions into Q3 2026 results. The DIP loan buys time; it does not eliminate the risk. Investors tracking Korean banking sector names (KB Financial 105560.KS, Shinhan 055550.KS, Hana 086790.KS, Woori 316140.KS) should note that Homeplus exposure remains a tail risk item in near-term earnings calls.

The Structural Retail Story

Homeplus's crisis is, at its core, a story about Korea's rapid shift to online commerce colliding with legacy physical retail infrastructure financed by LBO-level debt. E-commerce platforms led by Coupang (CPNG) and Naver's Naver Plus Store have reshaped the grocery and general merchandise landscape, compressing the pricing and volume metrics that originally justified the Homeplus acquisition.

The sale of Homeplus Express to NS Shopping signals an orderly dismantling of the non-core assets. Whether the remaining 67 hypermarkets can be right-sized into a viable business under court supervision — or whether this rescue is simply delaying an inevitable restructuring — will be the defining question of the next 12 months.

What to Watch

- July 20: Does the Seoul Bankruptcy Court accept Homeplus's appeal and restart rehabilitation? A rejection would trigger an accelerated liquidation process.

- July 27: National Assembly hearing. Political pressure on MBK Partners may increase, and regulatory scrutiny of foreign PE activity in Korean retail is likely to intensify.

- Meritz Q2 2026 earnings: Watch for new provisions against the ₩1.2T exposure and any guidance on NPL trajectory.

- 38 store reopening timeline: Operational restoration is the practical indicator of whether the rehabilitation is real or cosmetic.

Sources: - MBK, Meritz strike last-ditch deal to rescue Homeplus — Korea Times - Meritz to extend emergency loan to keep MBK-owned Homeplus afloat — KED Global - Homeplus plans to reopen closed stores after ₩200B DIP loan — JoongAng Daily - Homeplus secures ₩200B lifeline from Meritz to avert liquidation — Korea Herald - Homeplus Faces Bankruptcy: 12,000 Employees on the Brink — BigGo Finance - Meritz Financial Group Launches ₩280B Bond Sale — BigGo Finance

LineVest News is an independent financial publication. Nothing here is investment advice.