TL;DR - ChangXin Memory Technologies (CXMT) priced China's largest-ever semiconductor IPO on July 15 at 8.66 yuan per share, raising 57.9 billion yuan (approximately USD 8.55 billion) — or up to USD 9.83 billion with the full overallotment option exercised - The offering valued CXMT at 579 billion yuan (approximately USD 85.6 billion), drew 212 times oversubscription from 9.4 million investors, and eclipsed SMIC's 2020 A-share chip listing record - SK Hynix's Nasdaq ADR (SKHY) fell approximately 7% and Micron (MU) shed roughly 5% on the announcement; the near-term concern is CXMT deploying proceeds to expand commodity DRAM capacity - Samsung Electronics (005930.KS) and SK Hynix (000660.KS) together control approximately 79% of global HBM supply — a segment where CXMT's own mass-production timeline trails by two to three technology generations

Part A — The IPO: Scale and Context

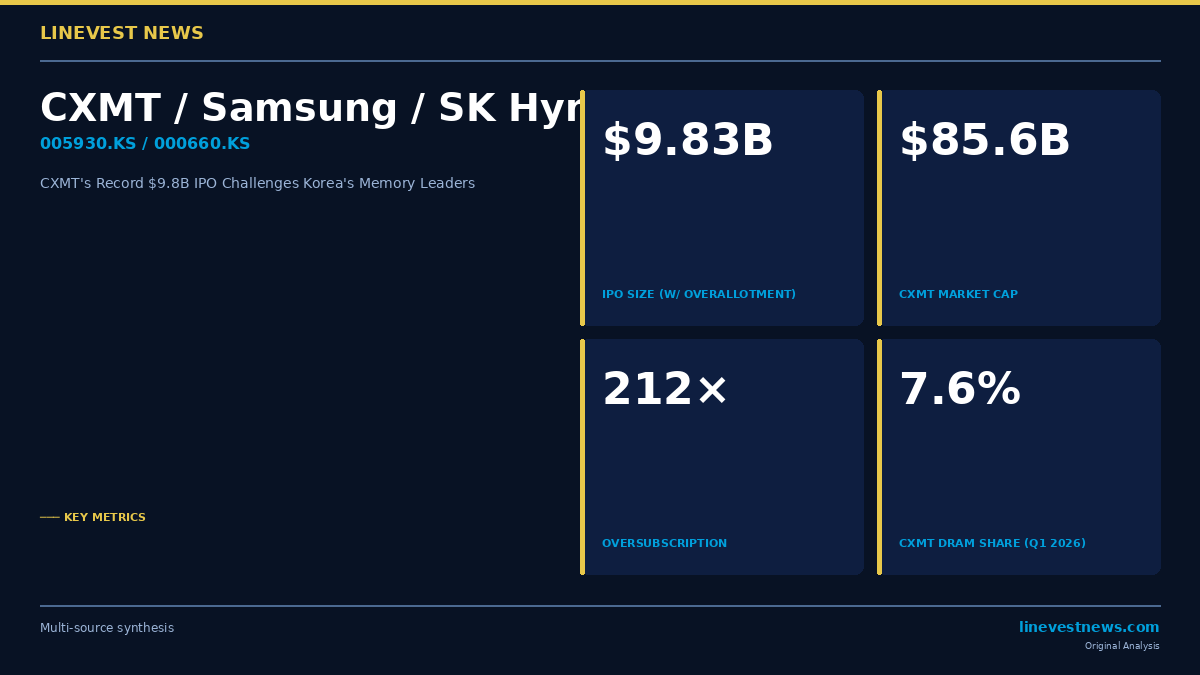

On July 15, ChangXin Memory Technologies formally launched its initial public offering on Shanghai's STAR Market at 8.66 yuan per share. The company is selling approximately 6.7 billion new shares — roughly 10% of its enlarged capital — to raise 57.9 billion yuan (approximately USD 8.55 billion). With the full overallotment option, total proceeds rise to 66.6 billion yuan (approximately USD 9.83 billion).

| Metric | Value |

|---|---|

| IPO price | 8.66 yuan (approx. USD 1.28) per share |

| Gross proceeds (base) | 57.9 billion yuan (approx. USD 8.55 billion) |

| Gross proceeds (w/ greenshoe) | 66.6 billion yuan (approx. USD 9.83 billion) |

| Implied market cap | 579 billion yuan (approx. USD 85.6 billion) |

| Oversubscription | 212× from 9.4 million investors |

| Previous A-share chip IPO record | SMIC, 53.23 billion yuan (2020) |

The final proceeds are nearly double the 29.5 billion yuan CXMT had originally earmarked for investment when it filed its initial prospectus on July 9 — an upward revision that reflects overwhelming demand. The company expects to list on the STAR Market around July 27, 2026.

Proceeds are designated for DDR5 and LPDDR5X production line upgrades and next-generation DRAM research and development.

Part B — Implications for Samsung and SK Hynix

Market reaction: Korea's ADR took an immediate hit

When CXMT's IPO terms became public, SK Hynix's Nasdaq-listed ADR (SKHY) fell approximately 7% in U.S. trading, and Micron (MU) shed roughly 5%. The reflexive sell-off reflects a straightforward concern: CXMT is raising approximately USD 9.8 billion expressly to build more DRAM capacity, and incremental supply from a state-backed Chinese challenger exerts downward pressure on commodity pricing across the industry.

Mapping the battlefield: commodity DRAM

CXMT's business is almost entirely concentrated in mainstream DRAM products. In 2025, more than 98% of its revenue derived from LPDDR and DDR products — including DDR5, LPDDR5X, and related mobile memory. The Q1 2026 global DRAM market share breakdown underlines just how rapidly the company has scaled:

| Company | DRAM Market Share (Q1 2026) |

|---|---|

| Samsung Electronics (005930.KS) | 38.6% |

| SK Hynix (000660.KS) | 28.8% |

| Micron Technology (MU) | 22.4% |

| CXMT | 7.6% |

Source: Omdia via Seoul Economic Daily

CXMT held 4.7% share in Q4 2025 and jumped to 7.6% in Q1 2026 — a near-three-percentage-point gain in a single quarter, suggesting aggressive wafer output expansion is already underway ahead of IPO proceeds being deployed.

Korea's HBM moat

What structurally insulates Samsung and SK Hynix — at least in their highest-margin segment — is the HBM market. High Bandwidth Memory is the wide-bus DRAM architecture at the core of Nvidia's AI accelerators, AMD's Instinct GPUs, and next-generation inference infrastructure. Samsung and SK Hynix jointly supply approximately 79% of the global HBM market.

CXMT acknowledged the gap directly in its IPO prospectus: "Three global competitors maintain technological advantages in HBM." The company's own roadmap targets HBM3E mass production in 2027. By then, Samsung and SK Hynix are expected to be shipping HBM4 in volume. That preserves a roughly two-to-three-generation lead in the segment where memory economics are most favourable.

The commodity risk

Even with HBM protected, Samsung's Device Solutions (DS) Division still derives revenue from standard DDR5 and server DRAM sold to PC and hyperscale OEMs. If CXMT channels IPO proceeds into commodity capacity that reaches market from 2027 onward, it could compress spot prices for those products.

That said, semiconductor fab construction timelines are long. Meaningful incremental wafer starts from CXMT's new capital are unlikely before late 2027 at the earliest, limiting near-term operational impact. The current sell-off in Korean ADRs is more sentiment-driven than a reflection of imminent supply-demand disruption.

Samsung's DS Division reported preliminary operating profit of approximately 53.7 trillion won in Q1 2026, representing roughly 93.8% of the group's total OP — with the vast majority driven by HBM. A commodity pricing headwind, while real, registers as a fractional impact against those numbers.

Key dates for Korea watchers

- July 22 (Tuesday) — SK Hynix Q2 2026 preliminary earnings. Consensus operating profit: approximately 64–65 trillion won. Management commentary on commodity DRAM pricing versus HBM product mix will be the key signal.

- July 27 (expected) — CXMT's anticipated STAR Market trading debut. Post-listing pricing will test whether the USD 85.6 billion valuation holds or runs higher toward the 3–5 trillion yuan targets circulated by some retail investors.

- July 30 (Thursday) — Samsung Electronics Q2 2026 full results and conference call.

CXMT's USD 9.8 billion listing represents the most significant milestone yet in China's national memory programme — a transition from state-subsidy-funded capacity experiment to a company capable of raising nearly USD 10 billion in public equity markets. The commodity DRAM flank warrants monitoring. But until CXMT closes the HBM technology gap — and its own 2027 HBM3E timeline versus Korea's current HBM4 ramp suggests that will not happen soon — Samsung (005930.KS) and SK Hynix (000660.KS) retain dominance in the segment where memory margins are highest.

Sources: South China Morning Post · Nikkei Asia · Seoul Economic Daily · BigGo Finance · TechTimes