Uber Technologies has agreed to acquire Germany-listed Delivery Hero SE for €41.50 per share in cash, a deal valuing the company at $14.8 billion — and placing South Korea's dominant food-delivery platform, Baemin (배달의민족), under American ownership for the first time.

TL;DR - Uber offers €41.50/share cash (~$14.8B total; $13.7B net of existing stake) - Premium: ~127% over Delivery Hero's unaffected three-month average (pre-May 8, 2026) - Baemin = Korea's #1 food-delivery app, 15.24M weekly active users, ~60%+ market share - KFTC scrutiny expected: previously imposed conditions on Delivery Hero's 2019 Woowa Brothers deal - Expected close: H2 2027; SSW Partners acquires 14 overlapping markets for $1.6B separately - Coupang Eats (CPNG) is the primary rival — the duopoly now enters a new chapter

Part A — The Deal

Price, Premium, and Structure

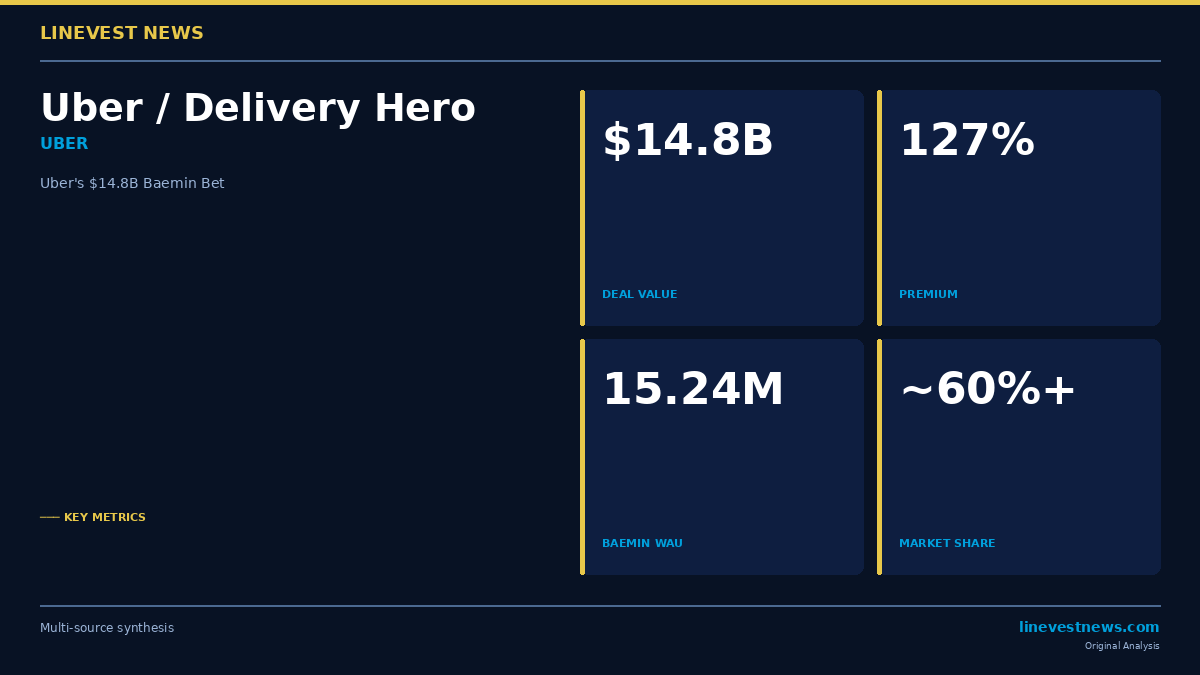

Uber announced on July 16, 2026 that it will pay shareholders €41.50 per share in cash, representing approximately a 127% premium over Delivery Hero's unaffected three-month average share price prior to May 8, 2026, and roughly 34% above the three-month average before the formal announcement.

The total equity value stands at $14.8 billion; Uber's net outlay is approximately $13.7 billion after accounting for its pre-existing stake in Delivery Hero. The company has secured irrevocable commitments covering 16.68% of Delivery Hero shares, which, combined with its existing holdings, pushes its total economic interest above the 53% threshold required for deal approval.

To fund the transaction, Uber has arranged a bridge loan of roughly €14 billion.

| Metric | Value |

|---|---|

| Offer price per share | €41.50 (cash) |

| Total deal value | ~$14.8B |

| Net cost to Uber | ~$13.7B |

| Premium (vs. pre-May 8 avg) | ~127% |

| Bridge loan | ~€14B |

| Expected closing | H2 2027 |

Carve-Outs

In a parallel transaction, SSW Partners — a New York-based investment firm — will acquire Delivery Hero's operations in 14 overlapping markets (including foodora in Austria, Norway, and Sweden, and Yemeksepeti in Turkey) for approximately $1.6 billion. These are markets where Uber Eats and Delivery Hero's brands competed directly, and separating them helps ease antitrust risk.

Strategic Rationale

The combined entity would span 99 markets, with projected 2025 gross bookings of $236 billion. Uber frames the deal as a means to extend its super-app ecosystem — integrating Baemin's food-delivery scale with Uber's ride-hailing network and Uber One subscription platform.

Part B — What the Uber-Baemin Deal Means for Korea

Baemin's Dominant Position

Baemin (operated by Woowa Brothers Corp.) is not merely a participant in Korea's food-delivery market — it is the market. As of May 2026, the platform recorded 15.24 million weekly active users, versus 8.45 million for Coupang Eats. Together, the two apps command 88.3% of Korea's delivery app market, the highest duopoly concentration on record.

Baemin's individual market share is estimated above 60%. Despite a period of customer churn to Coupang Eats in early 2026 (driven by aggressive promotional spend from Coupang), Baemin retained its structural lead among both consumers and partner restaurants.

| Platform | Weekly Active Users (May 2026) | Est. Market Share |

|---|---|---|

| Baemin (Delivery Hero) | 15.24M | ~60%+ |

| Coupang Eats | 8.45M | ~28% |

| Others (Yogiyo, etc.) | — | ~12% |

KFTC: Déjà Vu?

Korean antitrust law will almost certainly put this deal under scrutiny. The Korea Fair Trade Commission (KFTC) previously granted conditional approval when Delivery Hero first acquired Woowa Brothers in 2019 — a transaction that was itself considered highly concentrated given Baemin's share at the time.

With Uber now folding Baemin into a global platform that also operates in adjacent markets, KFTC may revisit conditions around pricing practices, rider compensation, and restaurant exclusivity arrangements. The regulator has grown more assertive on digital platforms, as evidenced by its 2026 proceedings against major Korean tech companies.

Uber has publicly committed that "Korea is one of Uber's core markets, and our commitment to long-term investment in Korea remains unchanged." The company's stated top priority is "Baedal Minjok's stable business continuity and sustainable growth." Whether the KFTC treats these pledges as adequate behavioral remedies — or demands structural ones — will shape the integration timeline.

Coupang: Opportunity or Threat?

For Coupang (NYSE: CPNG), the deal is a double-edged development.

On one hand, Uber's global capital and operational infrastructure could strengthen Baemin's competitive position relative to Coupang Eats, especially in the Uber One subscription bundle. On the other hand, KFTC-mandated behavioral conditions could level the playing field in key areas (e.g., restaurant exclusivity clauses) where Baemin has historically had an edge.

Coupang Eats has been the faster-growing platform in Korea over the past 12 months, partly due to Coupang's warehouse-and-logistics integration (Rocket Delivery cross-sell) and promotional budgets. If regulatory scrutiny delays or restricts the Uber-Baemin integration, the competitive vacuum benefits Coupang Eats in the near term.

Coupang's shares (CPNG) are the most liquid instrument for investors seeking exposure to Korean food delivery; no Korean-listed pure-play equivalent exists.

Uber Eats + Baemin: Synergy or Brand Clash?

Uber Eats does not operate in South Korea independently. The acquisition of Baemin is Uber's entry into the Korean market through the category-leader route, rather than organic launch. Uber has explicitly stated it will invest in Baemin's brand — suggesting it will keep the Baemin identity intact rather than convert to Uber Eats branding, at least in the near term.

This matters for partner restaurants and delivery riders, who have long-standing contractual and trust relationships with the Baemin platform. A rapid brand change would risk churn at a structurally critical moment.

Deal Risk: Timeline and Regulatory Calendar

With a H2 2027 closing target, both Korean and EU antitrust reviews must proceed concurrently. The European Commission will scrutinize the deal under EU merger regulations, while KFTC will run a parallel domestic review. SSW Partners' concurrent acquisition of the 14-market carve-out adds complexity to the EU's assessment of Delivery Hero's footprint.

For investors, the key dates to watch are: (1) formal filing with Korea's KFTC (likely Q4 2026); (2) EU merger filing (concurrent); (3) Delivery Hero shareholder vote (no firm date yet, but Uber has secured >53% irrevocable commitments, making approval near-certain).

Investor Takeaway

| Dimension | What to Watch |

|---|---|

| KFTC review | Conditions on restaurant exclusivity, rider pay, pricing — precedent from 2019 Woowa approval |

| Baemin brand | Uber has signaled "no change" to Baemin identity in Korea |

| Coupang (CPNG) | Near-term integration uncertainty at Baemin benefits Coupang Eats share gains |

| Uber (UBER) | Gross bookings expansion into 99 markets; Korea is strategically central to Asia Pacific footprint |

| Closing risk | H2 2027 is 12-18 months out; deal breaks are rare at 127% premium, but regulatory conditionality is real |

Sources: The Korea Herald · KED Global · Seoul Economic Daily · Bloomberg · TechCrunch · Seoul Economic Daily – Market Share

This article is for informational purposes only and does not constitute investment advice. LineVest News is an independent publication not affiliated with any brokerage or issuer.