TL;DR - TSMC Q2 2026 revenue: $40.2 billion (record quarter), operating margin: 60.3% - Net income: approximately $22.4 billion (₩32.5 trillion), exceeding analyst consensus - FY2026 capex guidance raised to $60–64 billion (from ~$56 billion) - New $100 billion US Arizona commitment; cumulative US investment ~$265 billion - FY2026 revenue growth target upgraded to "slightly more than 40%" - Korea read: SK Hynix HBM demand sustained; Samsung Foundry OPM gap structural

Part A — What TSMC Reported

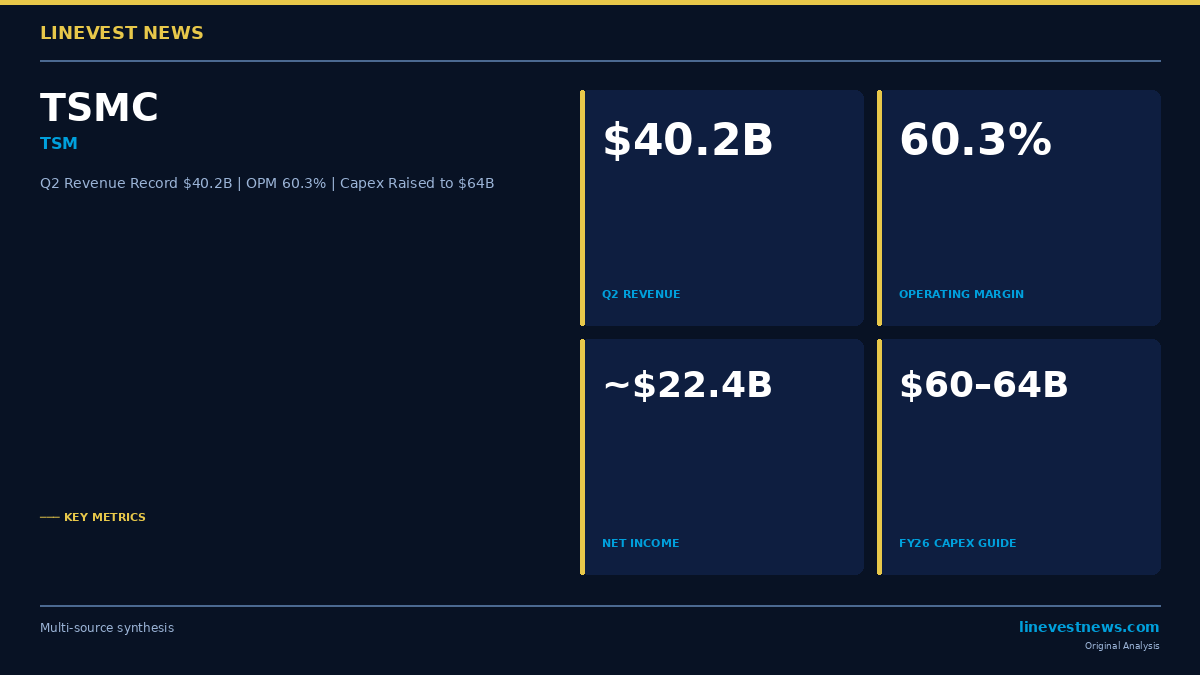

Taiwan Semiconductor Manufacturing Co. (NYSE: TSM) delivered a record second quarter on Wednesday, posting revenue of $40.2 billion for the April–June 2026 period — the strongest quarter in the company's history. Operating margin reached 60.3%, and net income came in at approximately $22.4 billion (₩32.5 trillion), well above analyst expectations that had centered around $20.1 billion.

The results confirm that AI-driven demand for advanced semiconductor processes has not peaked, contrary to concerns earlier in the year about potential inventory corrections. Demand was particularly strong for TSMC's 3-nanometer process, which underpins Nvidia's latest GPU and AI accelerator lineup, as well as for Apple's A-series and M-series chips.

Capex and US Investment

Management raised full-year 2026 capital expenditure guidance to $60–64 billion, up from a prior range of approximately $56 billion — a signal that TSMC expects demand to outpace current installed capacity. Separately, TSMC announced an additional $100 billion investment in its Arizona operations, bringing cumulative US commitments to approximately $265 billion (₩391.7 trillion). The Arizona expansion encompasses advanced wafer fabrication, CoWoS packaging facilities, and R&D centers.

Forward Guidance

Full-year 2026 revenue growth was upgraded to "slightly more than 40%" from the prior guidance of "30%-plus" — a meaningful upward revision. Management noted continued AI chip demand strength for Q3 while flagging that rising input prices could weigh on margins at the margin.

Part B — Korea Market Implications

SK Hynix: The Hidden Beneficiary of TSMC's AI Pipeline

TSMC's record quarter is not simply a Taiwan story. A significant portion of TSMC's volume growth stems from CoWoS advanced packaging, which integrates High Bandwidth Memory (HBM) directly with AI accelerators. SK Hynix (000660.KS) — which supplies roughly 50–60% of global HBM3E output, primarily to Nvidia — is structurally linked to the TSMC growth curve.

When TSMC raises capex and upgrades its Q3 outlook, it signals that Nvidia and its peers are continuing to place CoWoS orders, which in turn sustains SK Hynix HBM purchase orders. TSMC's incremental capex of $4–8 billion implies additional CoWoS capacity — most of which pairs with HBM3E and the emerging HBM4 standard that SK Hynix is first to qualify.

SK Hynix shares staged a significant recovery in the past week following KB Securities' analyst note projecting further upside. TSMC's Q2 results reinforce the demand-side argument underpinning that target.

| Korean Name | TSMC Linkage | Mechanism |

|---|---|---|

| SK Hynix (000660.KS) | CoWoS packaging client | HBM3E/HBM4 supply to Nvidia, AMD |

| Hanmi Semiconductor (042700.KQ) | TC Bonder for HBM stacking | Equipment demand from HBM supply chain |

| Samsung Electronics (005930.KS) | Foundry competition | DRAM tailwind intact; foundry gap widening |

Samsung Foundry: The Structural Gap Becomes Arithmetic

TSMC's 60.3% operating margin is not merely impressive — it represents a structural moat. Samsung Electronics (005930.KS) reported Q2 2026 operating profit of ₩89.4 trillion, a record, but the vast majority derived from its memory and System LSI divisions. The foundry segment continues to operate at a fraction of TSMC's profitability.

TSMC's pricing power — reflected in a 60.3% OPM — allows it to invest in next-generation 2-nanometer and below nodes at a pace Samsung's foundry unit struggles to match without diverting cash from other divisions. Samsung has publicly committed to regaining advanced foundry market share by 2027 through its GAA (Gate All Around) 2nm-class process. However, TSMC's $60–64B annual capex — roughly double Samsung's total semiconductor capex — means the technology gap is unlikely to close quickly.

For Korea-based investors, the Samsung foundry narrative remains a long-term structural story rather than a near-term catalyst. Samsung's Q3 upside is anchored in memory, not foundry.

AI Capex Cycle Duration Signal

TSMC's capex raise and $100B Arizona commitment are among the clearest signals yet that the AI semiconductor investment cycle is extending, not contracting. Earlier concerns that 2026 would see a demand peak — reminiscent of the 2021 DRAM bubble — have not materialized.

For Korean chip investors, this matters in two ways:

- Memory pricing support: Sustained AI GPU production → sustained HBM demand → HBM ASP support for Samsung DRAM and SK Hynix DRAM businesses alike.

- Equipment and materials uplift: TSMC capex feeds equipment and materials orders, a subset of which flows through Korean advanced-materials suppliers (CMP slurries, photoresist precursors, thermal interface materials).

Valuation Context

TSMC's record quarter arrives as KOSPI semiconductor stocks have already repriced materially in July 2026. The key question for investors is whether TSMC's guidance further re-rates Korean names or whether positive news is largely priced in following the recent rally.

- SK Hynix (000660.KS): Trading at elevated multiples post-July recovery, but AI HBM demand durability — now underscored by TSMC's capex commitment — remains the core bull argument.

- Samsung Electronics (005930.KS): Memory tailwind intact; foundry gap is a structural headwind that near-term earnings do not fully surface.

Key Financials

| Metric | Q2 2026 | Detail |

|---|---|---|

| Revenue | $40.2B | Record quarter |

| Operating Margin | 60.3% | Above analyst estimates |

| Net Income | ~$22.4B (₩32.5T) | Exceeded consensus ~$20.1B |

| FY2026 Capex Guidance | $60–64B | Raised from ~$56B |

| Additional US Investment | $100B | Cumulative US commitment ~$265B |

| FY2026 Revenue Growth Guide | "Slightly >40%" | Upgraded from "30%-plus" |

This article is journalism, not investment advice. LineVest News is an independent outlet with no brokerage affiliation. Past performance of referenced securities does not guarantee future results.

Sources: - ET News — TSMC Q2 Record Revenue, $100B US Investment - Yahoo Finance — TSMC Raises Capex and Revenue Forecast on AI Demand - Yahoo Finance — TSMC Long-Term Gross Margin Guidance Signals Confidence