Samsung Electronics' dominant semiconductor equipment subsidiary, Semes Co., officially established its first labor union on 15 July 2026, with workers demanding bonuses benchmarked to the parent's far more lucrative semiconductor-division pay scale — and Tokyo Electron Korea has signalled it will follow suit, extending the movement to a major Japan-owned equipment supplier.

TL;DR - Semes (Samsung Electronics 91.54%-owned equipment maker) launched its inaugural union, SEMUL, on 15 July covering all four sites. - Top demand: performance bonuses linked to Samsung's DS semiconductor division — not Semes standalone figures. - Tokyo Electron (TEL) Korea is recruiting members for its own union, taking the movement cross-border. - Semes Q1 2026 operating profit doubled (+106% YoY to ₩96.1B) on revenue of ₩596.3B, yet workers say gains did not flow through.

Part A — The Formation

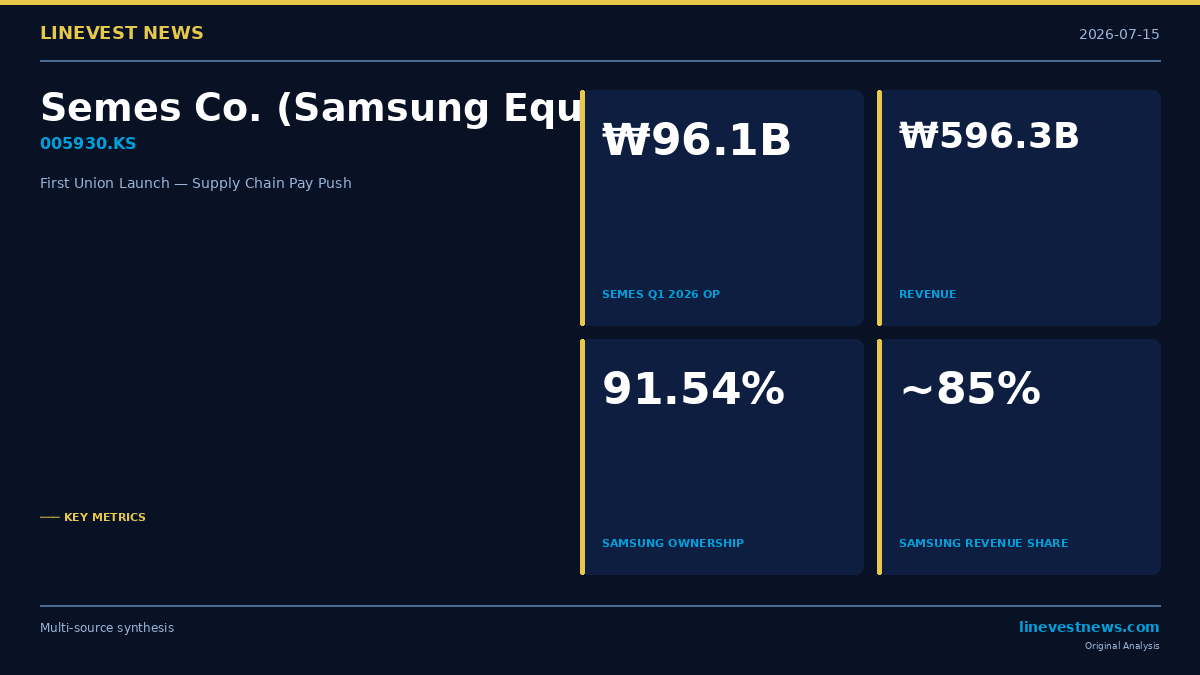

Semes Co., Korea's largest semiconductor equipment maker and a 91.54%-owned subsidiary of Samsung Electronics, formed its first labor union on 15 July 2026. Organizers notified executives and employees across all four business sites — Dongtan, Cheonan, Hwaseong, and Pyeongtaek — of the union's official launch under the name SEMUL (Semes Labor Union).

The company produces wet-cleaning tools (LOTUS, BLUEICE PRIME), photo-track systems (OMEGA-S, OMEGA-K) and etch equipment (Michelan O3, Michelan C4) that are integral to Samsung's advanced front-end and back-end process lines. Samsung Electronics accounts for approximately 85% of Semes revenue.

The union issued a founding statement that it would work with all employees to build "a workplace where the value created by labor is fairly evaluated." Specifically, it announced two central demands: (1) transparent disclosure of the "customer contribution profit" formula that feeds into Semes bonus calculations, and (2) a structural shift to a performance-bonus system explicitly linked to Samsung Electronics' DS (Device Solutions) division benchmarks rather than to Semes' standalone figures.

Within a day of the Semes announcement, Tokyo Electron Korea — the Korean unit of Japan's Tokyo Electron Ltd. (TYO: 8035) — said it would begin recruiting union members, industry sources reported. TEL Korea provides installation, maintenance and process-support services for TEL's advanced deposition, etch and thermal tools used in Samsung and SK Hynix fabs.

Part B — Market Implications

The Bonus Gap Fuelling the Drive

Korea's semiconductor super cycle has created sharply uneven reward distributions inside the supply chain. Samsung Electronics DS division workers are understood to have received performance bonuses many multiples higher than those paid to workers at affiliated equipment and component subsidiaries, whose pay packets are benchmarked only to their own entity's standalone financials.

Semes' results illustrate the gap viscerally. The company posted operating profit of ₩96.1 billion in Q1 2026, up 106% year-on-year, on revenue of ₩596.3 billion (+11% YoY). That profit acceleration directly reflects Samsung's accelerated equipment procurement for HBM and advanced DRAM capacity. Yet because Semes bonuses are calculated against Semes-level metrics — not DS metrics — workers captured only a fraction of the upside that flowed to their Samsung parent-division counterparts.

The demand for "DS linkage" would functionally import Samsung DS's bonus multiplication factor into Semes' compensation structure. Whether Samsung Electronics (the controlling parent) accepts this is the central negotiating question heading into management-union talks expected in August.

Supply-Chain Cost Inflation Now in Focus

For Samsung Electronics (KRX: 005930), the near-term exposure is absorbed within consolidated accounts — Semes is not publicly listed and its labour costs feed into Samsung's semiconductor-segment cost base. Any material wage increases at Semes would surface as (a) modestly higher intra-group procurement costs on Samsung's DS capex line and (b) tighter subsidiary-level margins visible in sum-of-parts valuations.

The broader signal is that labour-cost inflation is propagating downstream through the semiconductor supply chain: chip manufacturers → equipment makers. This timing matters. Samsung's DS division is reported to be in the final stages of equipment vendor selection for its Pyeongtaek P5 fab, with aggregate equipment orders in the double-digit trillion-won range expected to follow. Negotiating a multi-trillion-won procurement cycle while major equipment suppliers are simultaneously managing new union demands adds a fresh variable to Samsung's capital expenditure cost management.

TEL Korea: A Cross-Border Dimension

Tokyo Electron's Korean unit joining the movement introduces an international dimension absent from previous Korean semiconductor labour disputes. TEL Korea engineers support critical deposition, clean and etch process tools in Samsung and SK Hynix fabs. A unionised TEL Korea workforce would have collective bargaining leverage over maintenance and installation schedules — systemic risk that Tokyo Electron Ltd. (8035.T, a $100B+ market-cap global equipment giant) and its Korean customers will need to manage.

What to Watch

| Milestone | Expected Timing | Investor Signal |

|---|---|---|

| First Semes union–management negotiating session | August 2026 | Sets baseline for DS-linked bonus demands |

| TEL Korea formal union registration | Q3 2026 | Confirms cross-border equipment-labour trend |

| Samsung P5 Phase 1 equipment vendor announcement | Q3–Q4 2026 | Clarifies procurement volume and cost exposure |

| Semes Q2 2026 earnings | August 2026 | Tests whether profit growth is shared with labour |

Samsung Electronics (KRX: 005930) remains the primary equity ticker for investors tracking the downstream cost impact. Equity models for Samsung's DS-segment operating margin should now incorporate equipment-supplier labour costs alongside wafer cost deflation, HBM pricing dynamics and the P5 ramp timeline.

All financial figures in Korean won unless stated otherwise. This article is published for informational purposes only and does not constitute investment advice. LineVest News is not a registered investment adviser.

Sources