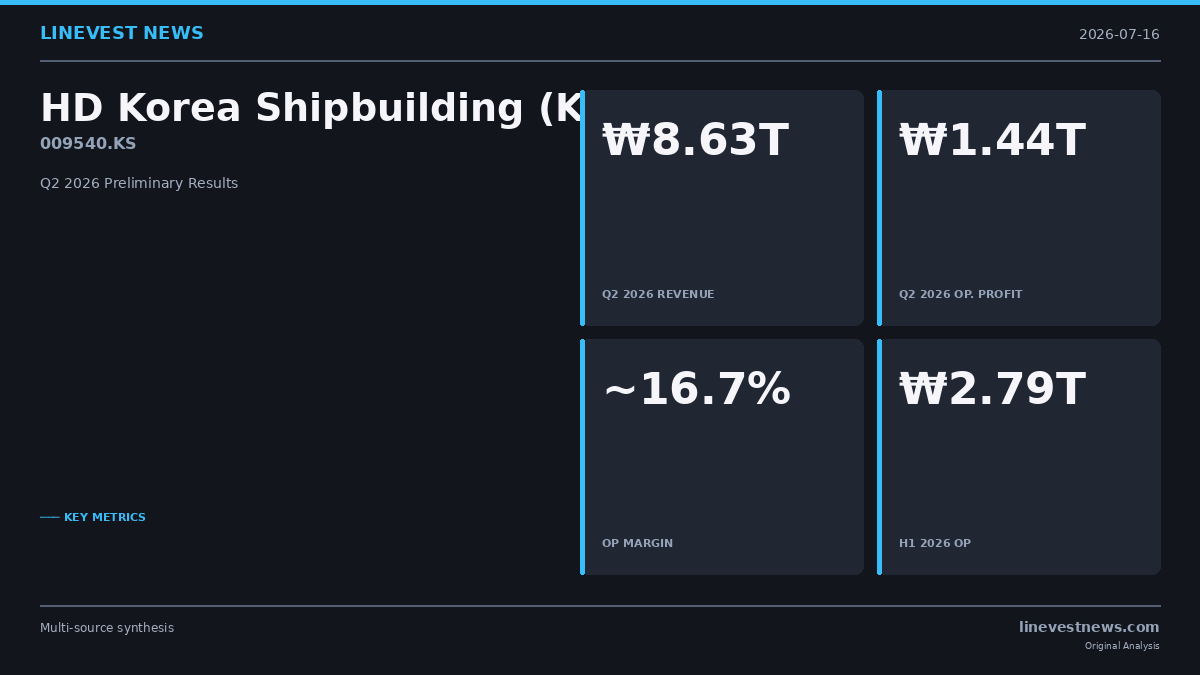

HD Korea Shipbuilding & Offshore Engineering (HD KSOE; 009540.KS) filed a preliminary earnings disclosure (영업잠정실적, 공정공시) with the Korea Exchange on July 16, 2026 (receipt no. 20260716800643), reporting second-quarter 2026 consolidated revenue of ₩8.63 trillion (approximately USD 5.8 billion) and operating profit of ₩1.44 trillion (approximately USD 964 million).

The operating profit figure represents a 50.8% year-on-year increase from an estimated ₩954 billion in Q2 2025, while revenue rose 16.1% from approximately ₩7.43 trillion in the prior-year period. The implied operating margin for Q2 2026 stands at approximately 16.7% — matching the Q1 2026 level and marking the highest sustained profitability in the company's history. A full segment-level breakdown will be released with the official Q2 earnings report on August 18, 2026.

TL;DR - Q2 2026 consolidated revenue: ₩8.63T (+16.1% YoY); operating profit: ₩1.44T (+50.8% YoY) - Operating margin holds at ~16.7%, consistent with Q1 2026 — highest in company history - H1 2026 cumulative operating profit: approximately ₩2.79T - Order intake stands at USD 16.39B, or 70.3% of USD 23.31B annual target, with six months remaining - Analyst consensus: 14 analysts, Strong Buy, 12-month target ₩594,714 (+72% from ~₩346,500)

Part A — The Disclosure

Quarterly Financial Performance

The preliminary results, disclosed under Korea Exchange fair-disclosure rules (공정공시), capture the top-line and operating-profit totals only. Net income and a full balance-sheet update will accompany the August 18 formal announcement.

| Quarter | Revenue (KRW T) | YoY | Operating Profit (KRW T) | YoY | OP Margin |

|---|---|---|---|---|---|

| Q2 2025 (base) | ~₩7.43T | — | ~₩954B | — | ~12.8% |

| Q1 2026 | ₩8.14T | +20.2% | ₩1.356T | +57.8% | 16.7% |

| Q2 2026 (prelim.) | ₩8.63T | +16.1% | ₩1.438T | +50.8% | ~16.7% |

H1 2026 totals: estimated revenue of ₩16.77T and operating profit of approximately ₩2.79T, implying that the company needs roughly ₩2.85T in H2 2026 to reach the consensus full-year forecast of ₩5.64T.

Q1 2026 Segment Breakdown (for Context)

The Q2 segment details will arrive August 18, but Q1 2026 — the most recent full disclosure — illustrates the multi-engine profit structure:

| Segment | Q1 2026 Revenue | YoY | Q1 2026 OP | YoY |

|---|---|---|---|---|

| Shipbuilding (조선) | ₩6.70T | +14.6% | ₩1.111T | +42.1% |

| Engine & Machinery | ₩717.0B | +7.5% | ₩218.1B | +41.3% |

| Offshore & Engineering | ₩457.8B | +183.8% | ₩86.6B | +1,212.1% |

The offshore and engineering recovery — from a near-zero OP base in early 2025 — is a material margin tailwind that investors frequently underweight.

Part B — Korean Market Implications

The Margin Inflection Is Structural, Not Cyclical

Operating profit growing at 3.2× the pace of revenue (+50.8% vs. +16.1%) is the clearest sign yet that HD KSOE is deep into a backlog repricing cycle. LNG carriers contracted at USD 230–260 million per vessel during the 2022–2024 upcycle are now entering the production phase where milestone payments — typically 20–30% of contract value on keel-laying, 30–40% on delivery — flow into revenue. Each LNG carrier delivery at current newbuild prices generates shipbuilding-segment margins that management has guided at 15–17%.

The Q1 2026 confirmation of 16.7% consolidated OP margin, now seemingly sustained into Q2, is significant: it marks the first time HD KSOE has held this margin level for two consecutive quarters. The prior record was a single-quarter peak in 2023 before offshore losses dragged the blended figure down.

Order Book: USD 60B+ Backlog, 70% of 2026 Target Secured

As of mid-July 2026, HD KSOE has signed USD 16.39 billion in new orders across 142 vessels, representing 70.3% of its USD 23.31 billion annual target — ahead of the mid-year pace needed to hit the full-year number.

Backlog composition entering 2026 exceeded USD 60 billion, providing revenue coverage through approximately 2028–2029 at current production cadence. The 2026 additions break down as: - 17 LNG carriers — the highest-margin product; each vessel ~USD 250–260M - 28 container ships — volume-driven, lower margin but broad market exposure - 43 LPG / ammonia / liquid CO₂ carriers — the forward-looking portfolio for shipping decarbonization

The ammonia and liquid CO₂ carrier exposure is notable. As IMO 2030 regulations tighten and regional carbon markets expand, demand for vessels transporting alternative energy vectors is structurally early-cycle. HD KSOE's 43-vessel position in this segment is building optionality without the near-term earnings risk of fully committing to unproven green-fuel propulsion.

Peer Comparison: Big Three Approach ₩10T Combined OP

HD KSOE's Q2 result is the leading component of a broader K-Shipbuilding earnings surge:

| Company | Q2 2026 OP (est.) | YoY | Full-Year Consensus |

|---|---|---|---|

| HD KSOE (009540.KS) | ₩1.438T | +50.8% | ₩5.64T |

| Hanwha Ocean (042660.KS) | ₩521.7B | +40.3% | ₩1.9T |

| Samsung Heavy Industries (010140.KS) | ₩390.2B | +90.5% | ₩1.5T |

| Combined | ~₩2.35T | +52.5% | ~₩9.0–10T |

Samsung Heavy's 90.5% surge reflects the deepest recovery arc: dry-dock re-normalization and first meaningful LNG carrier deliveries from a thin 2022 base. Its margin trajectory, while lower in absolute terms (~12% vs. HD KSOE's ~17%), is likely to narrow the gap through 2027 as its own peak-cycle backlog matures.

The combined ₩9.0–10T full-year industry target, if realized, would represent an industry-wide operating profit record by a wide margin. H1 combined OP for the three yards was approximately ₩3.6–3.7T; H2 needs ₩5.3–6.3T — achievable if delivery schedules remain intact, but demanding.

BoK Rate Hike: Context, Not Catalyst

The Bank of Korea raised the benchmark rate by 25 basis points to 2.75% on July 16, 2026 — the first rate increase since 2023 — citing CPI at 3.1% and broad growth strength. For HD KSOE specifically:

- Translation effect: A stronger won reduces the KRW-equivalent value of USD-denominated orders on the books. HD KSOE contracts almost entirely in USD, so won appreciation — a frequent consequence of rate hikes relative to the Fed — creates translation headwinds on reported revenue

- Financing cost: Higher domestic rates marginally increase working-capital costs for in-production vessels, though HD KSOE's strong operating cash flow and pre-delivery payments from customers structurally limit this exposure

- Net assessment: Rate-hike impact on shipbuilding earnings is second-order relative to backlog repricing and production throughput. The market's attention on July 16 is appropriately focused on the DART preliminary results, not the BoK decision

Investor Takeaway

Fourteen sell-side analysts carry a Strong Buy consensus on 009540.KS, with a 12-month price target of ₩594,714 — approximately 72% upside from the early-July trading range of ₩345,500–346,500. The Q1 2026 earnings beat (EPS of ₩11,930 vs. consensus estimate of ₩10,390, a 14.8% positive surprise) sets a high bar for Q2, which the preliminary ₩1.44T OP number appears to at least meet on operating profit.

Key risks for H2 2026: 1. Delivery schedule compression: Critical components — LNG containment membranes (GTT licenses), dual-fuel engines — face global supply scarcity if shipyard capacity runs at full utilization across Europe and Asia simultaneously 2. Container market softening: A deceleration in global trade volumes would reduce appetite for new container vessel orders, potentially slowing 2027 backlog replenishment 3. Green-fuel technology inflection: If methanol or ammonia propulsion achieves scale faster than expected, the premium for LNG carriers could compress as buyers reassess long-term fuel strategies

For Korean investors, HD KSOE's trajectory underscores why the shipbuilding sector — often dismissed as capital-intensive and cyclical — now commands premium valuations. The combination of multi-year backlog visibility, disciplined order pricing, and margin structure approaching software-sector levels in the high-teen percentages is a qualitative story the numbers are beginning to quantify.

HD Korea Shipbuilding & Offshore Engineering (009540.KS) filed a preliminary earnings disclosure (공정공시) on July 16, 2026 (DART rcept. no. 20260716800643). The full Q2 2026 earnings, including segment breakdowns and net income, are scheduled for release on August 18, 2026.

This article is for informational and journalistic purposes only and does not constitute investment advice. LineVest News is not a registered investment adviser.

Sources: Cyprus Shipping News — Korean Shipbuilders Eye ₩10T Profit · BigGo Finance — South Korea's Big Three Shipbuilders · In The News — HD KSOE Q1 2026 · Financial News Korea — ₩10T Milestone · Yahoo Finance — 009540.KS · DART Disclosure 20260716800643