TL;DR - Q2 2026 revenue: ₩251.1B (+39.5% YoY) — all-time record since 1980 founding - Operating profit: ₩130.3B (+51.0%) — record OPM of 51.9% - Drivers: HBM4 TC bonder deliveries + MSVP (panel-level packaging) orders surge - Pipeline: 2nd-Gen Hybrid Bonder prototype Q4 2026; Wide TC Bonder H1 2027 - Risk: revenue concentration in SK Hynix and Micron HBM capex cycles

Part A — What Was Disclosed

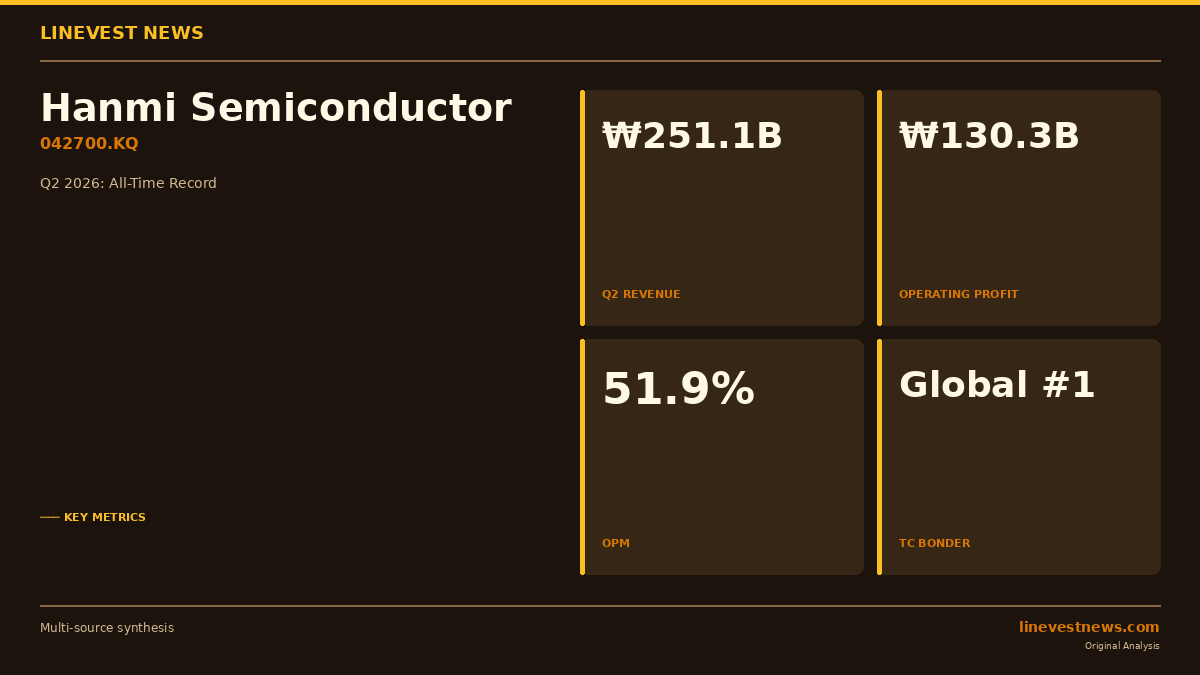

Hanmi Semiconductor (042700.KQ) filed a preliminary earnings disclosure on July 14, 2026, reporting its strongest quarter since the company's 1980 founding.

Financial Highlights — Q2 2026 (Consolidated)

| Metric | Q2 2026 | Q2 2025 | YoY Change |

|---|---|---|---|

| Revenue | ₩251.1B | ₩179.9B | +39.5% |

| Operating Profit | ₩130.3B | ₩86.2B | +51.0% |

| Operating Margin | 51.9% | 47.9% | +4.0%p |

Full income statement (net income, segment detail) to be published with the formal quarterly filing.

Two product lines drove the result:

TC (Thermal Compression) Bonder — stacks DRAM dies using heat and pressure to form High-Bandwidth Memory (HBM) packages. Hanmi holds the global No. 1 position in TC bonder supply. As SK Hynix and Micron entered volume production of sixth-generation HBM (HBM4) this year, new bonder unit deliveries accelerated.

MSVP (Micro-Saw and Vision Placement) — an integrated tool that cuts, cleans, dries, inspects, sorts and loads finished semiconductor packages. Broader adoption of panel-level packaging (PLP) in AI processor packages expanded MSVP order volume in Q2.

Alongside its core HBM tools, Hanmi is supplying three advanced 2.5D packaging tools to global foundries and OSATs: - 2.5D TC Bonder 40 (chip-on-wafer) - FC Bonder 3.5 and FC Bonder 75 (wafer-on-substrate)

Part B — Korea Market Analysis

1. The HBM Equipment Leverage Point

A 51.9% operating margin is rare in capital equipment — most global peers operate in the 20–35% range. Hanmi's margin reflects near-monopoly positioning in TC bonder supply: HBM producers must source these tools from Hanmi before they can scale output.

The forward signal is HBM4E (seventh generation, 12-stack and 16-stack). The company disclosed that preparations for HBM4E production will begin in late 2026 and early 2027, creating a second demand wave before the current HBM4 cycle peaks. Both SK Hynix and Micron have announced large HBM4 capacity expansions; Micron specifically flagged investments in Taiwan, Singapore, the U.S. and Japan.

2. Product Pipeline — Multi-Year Runway

| Product | Target Launch | Application |

|---|---|---|

| 2nd-Gen Hybrid Bonder (prototype) | Q4 2026 | 16-stack+ HBM (~2029 mass production) |

| Wide TC Bonder | H1 2027 | Next-gen high-stack density HBM |

The Hybrid Bonder roadmap targets stacks above 16 dies — configurations that most HBM roadmaps project for 2028–2030. This gives investors a visible order pipeline extending well beyond current HBM4 production.

3. Diversification Into AI System Chips

The three 2.5D packaging tools noted in Part A address AI system chip packaging at global foundries and OSATs, a market not confined to memory makers. This diversification provides partial insulation from pure HBM customer concentration, though memory bonders remain the dominant revenue source.

4. Investor Considerations

Upside factors: HBM4/HBM4E capex is in early ramp; each new HBM generation requires additional bonder units per production line; the TC bonder market expands as die stack counts rise; AI inference buildout extends the demand horizon beyond training capex alone.

Key risks: Hanmi's TC bonder revenue is heavily weighted toward SK Hynix (its largest customer), creating meaningful single-customer concentration. A capex pause, technology shift toward alternative bonding methods, or a competing bonder qualification could disrupt order flow. The 51.9% OPM also sets a demanding sequential comparison base.

Peer context: Dutch peer Besi (BE Semiconductor) trades at approximately 30× forward EV/EBIT; Tokyo Electron at ~25×. If Hanmi sustains record margins, a valuation re-rating is plausible — though the stock has historically been highly reactive to HBM cycle signals from SK Hynix and Micron.

This article is based on Hanmi Semiconductor's preliminary earnings disclosure filed July 14, 2026. Detailed figures (net income, balance sheet, segment breakdown) will be available with the formal quarterly report. All content is journalistic reporting and does not constitute investment advice.

Sources: Chosunbiz (July 14, 2026) · Maeil Business (MK) · ETnews