KakaoPay Securities Secures Investment Dealing License, Poised to Challenge Korea's IPO Underwriting Hierarchy

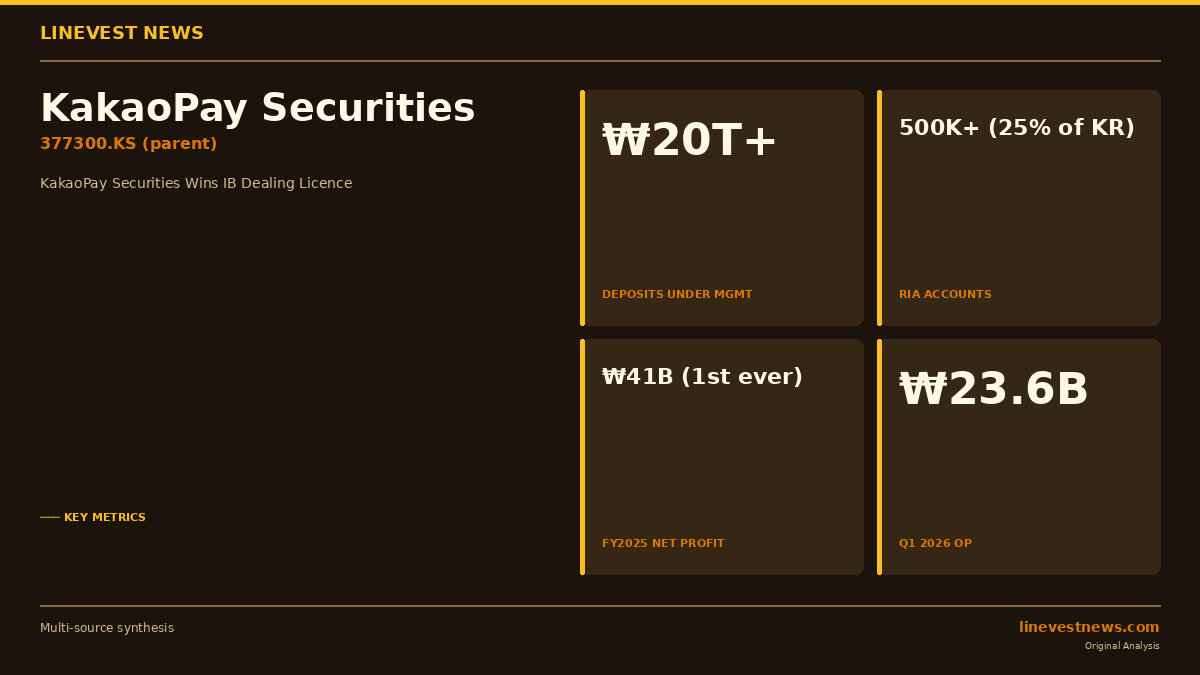

TL;DR - KakaoPay Securities (카카오페이증권) received FSC approval for 투자매매업 (investment dealing) license on July 1, 2026 — announced publicly on July 13 - Moves beyond commission-only brokerage to direct underwriting, trading, and sales of securities for the first time - Deposits under management exceed ₩20 trillion; 500,000+ robo-advisory accounts represent roughly 25% of the Korean industry total - FY2025 marked the firm's first annual net profit (₩41 billion); Q1 2026 operating profit reached ₩23.6 billion - CEO Shin Ho-cheol targets "comprehensive securities firm" status by pairing a 1-million-strong KakaoTalk channel with a growing IB desk

Part A — What the License Grants

KakaoPay Securities Co., a wholly owned subsidiary of KakaoPay Corp. (KRX: 377300), announced on July 13 that the Financial Services Commission formally approved its additional registration for 금융투자업 업무 단위 1-1-1 투자매매업·증권 — Korea's regulatory shorthand for the right to deal in securities on a principal basis — effective July 1, 2026.

Before the licence, the firm could only act as an agent, routing client orders for brokerage commission. Under the new authorisation it may:

| Capability | Previous Status | Post-Licence |

|---|---|---|

| IPO underwriting / syndication | ✗ Prohibited | ✓ Permitted |

| Corporate bond underwriting | ✗ Prohibited | ✓ Permitted |

| ETF liquidity provider (LP) | ✗ Prohibited | ✓ Permitted |

| Proprietary securities dealing | ✗ Prohibited | ✓ Permitted |

| Sales & Trading (S&T) expansion | Limited | Full scope |

| Retail brokerage (commission) | ✓ Permitted | ✓ Continues |

CEO Shin Ho-cheol said the authorisation "provides the foundation to leap forward as a comprehensive securities firm beyond brokerage," and added the company would "combine our large retail user base with IB capabilities to create differentiated synergies."

Scale of the Retail Platform

KakaoPay Securities' brokerage franchise is already substantial for a nine-year-old fintech: - Deposits under management: crossed ₩20 trillion (approx. USD 14.6 billion) in 2026 - Robo-advisory (RIA) accounts: 500,000+, representing approximately 25% of the Korean industry total - Pension savings accounts: 500,000+, giving access to Korea's growing defined-contribution market - KakaoTalk brokerage channel followers: 1 million — a direct retail marketing conduit built on Kakao's messaging super-app

Profitability Turning Point

The regulatory upgrade comes as KakaoPay Securities exits its loss-making startup phase: - FY2025 net profit: ₩41 billion — the company's first full-year profit since acquiring former Baro Securities in 2020 - Q1 2026 operating profit: ₩23.6 billion, suggesting the profitability trajectory is holding heading into the higher-activity spring-summer IPO season

The IB desk currently employs 80–90 professionals, with management signalling a phased hiring plan as deal flow ramps up.

Part B — Market Impact and Investor Implications

A New Challenger in the IPO Underwriting Pyramid

Korea's equity capital-markets business has long been dominated by a small group of bulge-bracket domestic houses: Mirae Asset Securities, KB Securities, NH Investment & Securities, and Samsung Securities account for the majority of IPO bookrunner mandates by deal value. Gaining the investment-dealing licence puts KakaoPay Securities on the regulatory footing needed to compete for a seat in underwriting syndicates for the first time.

The strategic edge is distribution. When a fintech whose app sits on the smartphones of tens of millions of daily payment users can also allocate IPO shares directly to those same customers, the underwriting value proposition changes. Retail tranche fill rates — a perennial headache for issuers in volatile markets — could benefit from a captive, app-native investor base that can subscribe with a few taps.

The KOSPI market context amplifies this timing. Benchmark indices have been running near multi-year highs in 2026, and pipeline activity — including high-profile candidates such as HD Hyundai Robotics and Kakao Mobility — is building. KakaoPay Securities is positioning itself to be relevant before the next wave of large listings clears regulatory review.

KakaoPay vs. Toss Securities: Diverging Fintech Strategies

Korea's two leading fintech-native securities firms are now pursuing clearly different paths:

| Dimension | KakaoPay Securities | Toss Securities (Viva Republica) |

|---|---|---|

| Strategy | IB + retail (domestic-first) | Retail-only + international expansion |

| Focus product | IPO underwriting, bond dealing | Fractional US stocks, US broker-dealer |

| Parent ecosystem | KakaoPay / KakaoTalk | Toss super-app |

| Regulatory push | 투자매매업 licence, Q3 2026 IB ramp | US FINRA broker-dealer licence |

The divergence matters for KakaoPay Corp (377300) shareholders: if the IB strategy translates into recurring underwriting fees — typically 1–3% of deal size — the revenue mix shifts away from commission-driven income that is structurally under pressure as zero-commission models spread.

What This Means for KakaoPay (377300.KS) Investors

Positive factors: - Margin expansion: IB underwriting fees carry structurally higher margins than per-trade brokerage commission - Platform monetisation: existing KakaoPay payment users represent an organic pipeline for IPO subscriptions and bond investment products, deepening Kakao's financial-services revenue per user - Competitive differentiation: no other fintech platform in Korea currently combines scale retail brokerage with a full dealing licence

Risk factors to monitor: - Capital requirements: operating as a principal dealer requires higher net capital ratios under FSS guidelines; this may constrain dividend capacity or require periodic capital injections from parent KakaoPay Corp - Execution risk: building credible IB relationships with corporate issuers takes years; the 80–90 person desk is small relative to incumbent teams of 200–400 at major houses - Regulatory scope expansion: FSS oversight of dealing operations is broader than brokerage-only, including position limits, prop-trading rules, and enhanced suitability requirements

Catalyst Watch

Key near-term indicators to track: 1. First public announcement of KakaoPay Securities as a joint bookrunner on a KOSPI or KOSDAQ IPO — likely H2 2026 if onboarding proceeds on schedule 2. KakaoPay Corp Q2 2026 earnings (July/August) for IB headcount and operating expense trajectory 3. Any FSS inspection or capital guidance following the licence expansion

Disclosure: This article is for informational purposes only and does not constitute investment advice. LineVest News is not a registered investment adviser.

Sources: E-Today (etnews) · Asia Today · Newspim