Fidelity and BlackRock Quietly Cut Korea Chip Stakes as AI Cycle-Peak Debate Sends KOSPI Down 9%

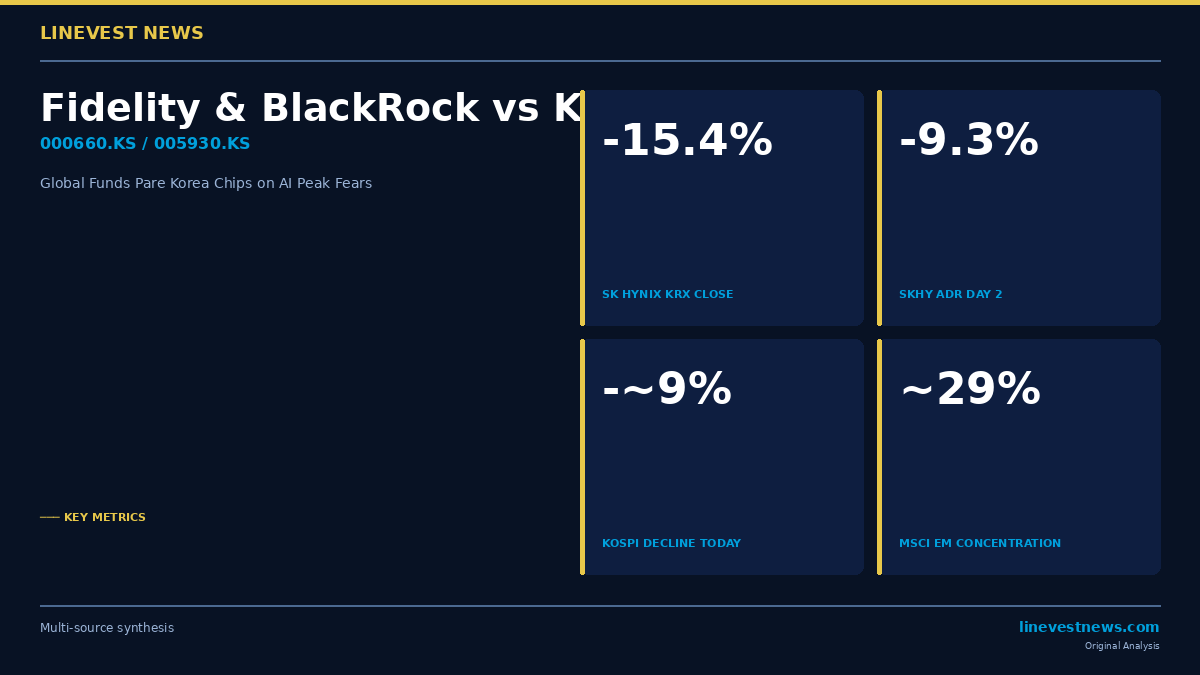

TL;DR - A Financial Times report (July 12) revealed that Fidelity International and BlackRock have trimmed exposure to Samsung Electronics, SK Hynix, and TSMC, citing AI-cycle peak concerns and ballooning MSCI Emerging Markets concentration - SK Hynix (000660.KS) closed down 15.4% at ₩1,845,000 on Monday — its largest ever single-session decline — while its Nasdaq ADR (SKHY) fell 9.3% to USD 152.35 on only its second full trading day, near the USD 149 IPO price - KOSPI tumbled approximately 9% to around 6,836, now more than 25% below the June 22 all-time closing high of 9,114.55 and on course for its worst single-day loss in 18 years

Part A: What the FT Report Found

A Financial Times report published July 12, 2026 revealed that major global asset managers — including Fidelity International and BlackRock — have begun selectively trimming positions in Samsung Electronics (005930.KS), SK Hynix (000660.KS), and TSMC as an AI-driven rally collides with growing concentration and leverage risks.

Caroline Shaw, a multi-asset portfolio manager at Fidelity International, specifically flagged two compounding risks: surging single-stock index concentration and the rapid proliferation of leveraged ETFs tracking the same three names. The combined MSCI Emerging Markets weight of Samsung, SK Hynix, and TSMC has reached approximately 29% — about three times the weighting of India's entire equity market. Within the index, SK Hynix alone carries a larger allocation than Brazil and South Africa combined.

Over the six months to early July, the market capitalisations of all three companies nearly doubled, each approaching roughly USD 1 trillion. Fidelity International and BlackRock declined to quantify the reductions but noted their cautious repositioning was driven by stretched valuations relative to the semiconductor cycle outlook and by the amplification risk created by leveraged products.

Part B: Korea Market Impact and What It Means for Investors

The FT report landed on the eve of what became the sharpest Korean equity session in nearly two decades.

Monday's Cascade

SK Hynix shares fell a record 15.37% to close at ₩1,845,000 (approximately USD 1,230), erasing roughly ₩39 trillion (USD 26 billion) in market capitalisation in a single day. The decline coincided with the second full trading session of SK Hynix's newly listed Nasdaq ADR (ticker: SKHY). After a spectacular debut on July 10 — when it surged 12.8% to USD 168.01, the largest-ever US equity offering by a foreign company at approximately USD 26.5 billion — the ADR fell 9.32% to USD 152.35 on Monday, pulling back to just above its USD 149 IPO price.

The broader KOSPI index fell approximately 9%, settling at around 6,836 and triggering the year's 18th sidecar halt. Monday's decline brought the index more than 25% below its June 22 all-time closing high of 9,114.55.

Why Earnings Estimates Moved Lower

Korea Investment Securities on Monday revised its SK Hynix Q2 2026 operating profit estimate to ₩60.4 trillion (revenue ₩80.9 trillion), roughly 8% below the market consensus of ₩65 trillion. The downgrade cited SK Hynix's particularly high exposure to high-bandwidth memory (HBM), which commands lower average selling prices than standard DRAM due to its customised architecture and customer-specific contracts. HBM4, the next-generation product expected to push ASP recovery, is not forecast to reach meaningful production volumes until Q3 2026. The firm also trimmed full-year 2026 and 2027 operating profit estimates by 9% and 11%, respectively.

The Leverage Amplification Problem

Since May 27, 2026, sixteen single-stock leveraged and inverse ETFs — fourteen long, two inverse — tracking Samsung Electronics and SK Hynix simultaneously debuted on Korean exchanges. They collectively handled an estimated ₩212 trillion (USD 141 billion) in trading volume during the AI rally, and their forced-liquidation mechanics materially amplified Monday's selling. Year-to-date, margin-call forced liquidations in Samsung and SK Hynix alone reportedly exceeded ₩10 trillion. The Financial Services Commission has received cross-party legislative pressure to suspend or deregister the products, though formal delisting would require new primary legislation.

The Bull Argument: Cycle Peak or Temporary Correction?

The bear case — institutional rebalancing plus earnings-estimate cuts — stands against a still-positive fundamental backdrop. According to TrendForce, commodity DRAM contract prices are forecast to rise 13–18% quarter-on-quarter in Q3 2026, with DDR4 spot prices outpacing DDR5 in an unusual dynamic driven by AI-server capacity redirection. Former Intel CEO Pat Gelsinger, now a venture capital executive, stated recently that AI infrastructure demand is "virtually unlimited," with power supply — not chip capacity — the binding constraint. These signals suggest the underlying HBM and server DRAM upcycle remains structurally intact even as the stock prices retreat.

What Foreign Investors Should Watch

For investors holding Korean equities, Monday crystallised a two-sided debate. On one side, global allocators (Fidelity, BlackRock) are reducing semiconductor concentration because index weight and leverage products have inflated exposure beyond fundamental justification. On the other, the actual earnings cycle for memory — HBM4 ramp in Q3, commodity DRAM pricing still rising — remains on track.

The critical data point will be SK Hynix's official Q2 2026 results, expected in late July 2026. If operating profit lands near the lowered KIS estimate of ₩60.4 trillion rather than the original consensus of ₩65 trillion, the earnings-revision cycle may already be priced into Monday's correction. A downside surprise versus even the reduced estimate, however, would validate the institutional sellers' thesis.

For MSCI EM-benchmarked investors specifically, the concentration mechanics mean any further institutional selling of the Samsung-SK Hynix-TSMC triad will have disproportionate index-level knock-on effects for Korean and Taiwanese equities broadly.

This article is published for informational purposes only and does not constitute investment advice. LineVest News is an independent publication and is not affiliated with any brokerage or advisory firm.

Sources: Newsis — FT via Newsis · Chosunbiz — Global fund managers · ETNews — Cycle peak signal · Chosunbiz — KIS earnings estimate