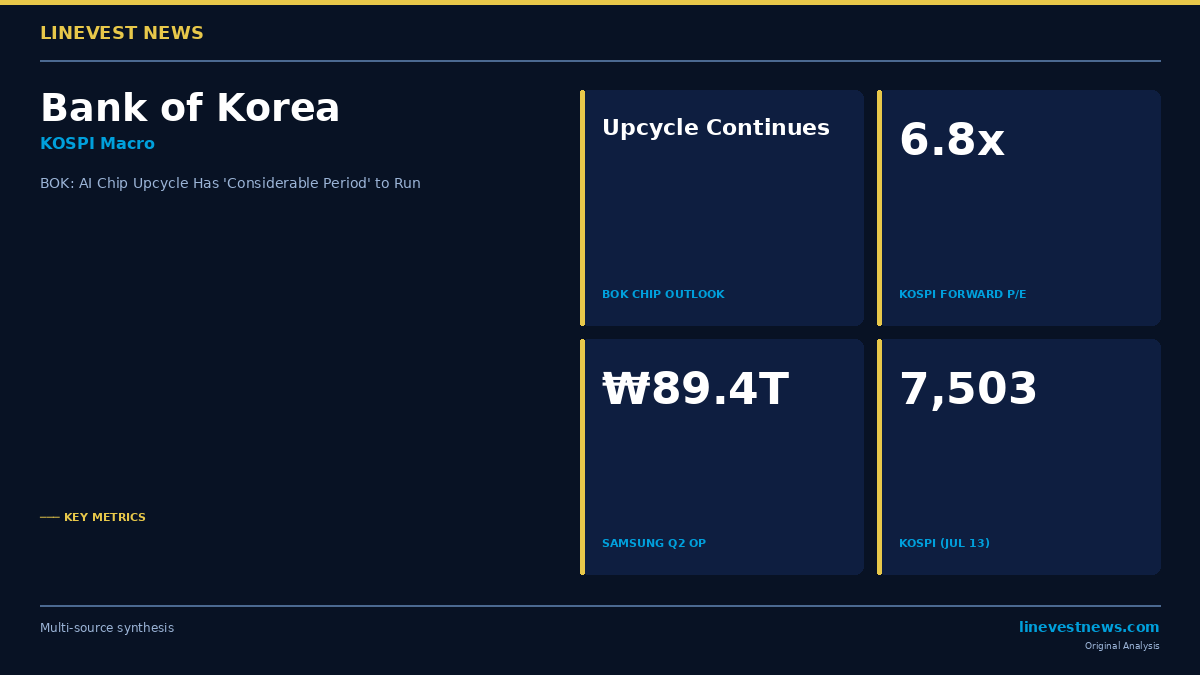

TL;DR - The Bank of Korea submitted an analysis to the National Assembly on July 13, 2026 maintaining the AI chip upcycle will continue for a "considerable period" - BOK identifies high-bandwidth memory (HBM) supply constraints as the structural differentiator from past cycles — custom products limit capacity expansion - JPMorgan, Goldman Sachs, and Morgan Stanley forecast the global semiconductor market remains robust through at least 2027 - Context: Samsung Electronics fell 9%+ and SK Hynix shed ~15% in recent weeks despite record-level earnings - KOSPI 12-month forward P/E near 6.8x — levels not seen since the 2008 global financial crisis

Part A — The BOK Report

The Bank of Korea submitted a policy brief to the National Assembly's Economics Committee on July 13, 2026, offering its official view on the current artificial intelligence semiconductor cycle. The report pushes back explicitly against market concerns that chipmakers are approaching a cyclical peak.

"While semiconductor demand has surged significantly due to investments in artificial intelligence infrastructure, the pace of supply expansion has been slow," the central bank stated.

The BOK identified custom products — most critically high-bandwidth memory (HBM) — as a structural constraint on supply growth. Unlike commodity DRAM that can be ramped through standardized processes, HBM requires multi-layer stacking and advanced packaging technology, fundamentally slowing capacity addition timelines. "The pace of supply expansion is more constrained than in the past, as the market is led by custom products such as high-bandwidth memory," the report noted.

The central bank's view aligns with major global investment banks. JPMorgan, Goldman Sachs, and Morgan Stanley have each generally forecast that the global semiconductor market will remain robust through at least 2027, citing AI infrastructure buildout as the primary demand driver.

The BOK did acknowledge uncertainty, noting risk around "the pace and scope of AI technology adoption, as well as its profitability" — a nod to ongoing debate about whether hyperscaler AI capital expenditure will generate the returns required to sustain demand.

Part B — Investment Analysis: KOSPI Semiconductor Stocks at a Crossroads

Why the Timing Matters

The BOK's official defense of the chip upcycle arrives during one of the most severe stretches for KOSPI semiconductor equities. Samsung Electronics (005930.KS) shed over 9% on July 2 when KOSPI circuit breakers were triggered, despite reporting record second-quarter operating profit of approximately ₩89.4 trillion (approximately $59.9 billion at ₩1,490/USD) — the highest ever quarterly figure in the company's history. SK Hynix (000660.KS) fell nearly 15% in recent sessions and lost an additional 4.36% on the morning of July 13, even as its freshly listed U.S. ADR (SKHY) closed its first day of Nasdaq trading at $168 against a $149 offering price — a 12.7% first-session premium that signals strong demand from U.S. institutional investors.

The divergence — ADR premium rising while the Korean parent falls — illustrates the gulf in sentiment between domestic and international investors, and underscores precisely why the BOK's analysis is relevant to foreign KOSPI holders.

Valuation Context: KOSPI at GFC-Level Discounts

The KOSPI 12-month forward price-to-earnings ratio has compressed to approximately 6.8 times — near the '-2 standard deviation' level below the 10-year average of roughly 10.2 times. Domestic strategists note that the last time valuations were this compressed was October 2008, during the peak of the global financial crisis. Historically, in every instance where KOSPI's forward P/E fell below this level, the index produced positive returns over 4, 13, 26, and 52-week horizons.

| Metric | Current Level | 10-Year Average | GFC 2008 Low |

|---|---|---|---|

| KOSPI 12M Forward P/E | ~6.8x | ~10.2x | ~6.0x |

| Samsung (005930.KS) Q2 OP | ₩89.4T | — | — |

| KOSPI (July 13 AM) | 7,503 | — | — |

| KRW/USD | 1,501.40 | — | — |

BOK's Structural Argument: Why This Cycle Differs

Traditional semiconductor downturns occur when supply overshoots demand — chipmakers add capacity aggressively, prices collapse, and margins compress. The BOK argues that HBM disrupts this playbook in two ways:

Supply cannot be rapidly ramped. HBM production requires bonding multiple DRAM dies with through-silicon vias (TSV) and advanced packaging. This is a fundamentally different — and slower — process than scaling commodity DRAM, making it structurally harder to flood the market.

Demand is qualitatively different. Unlike smartphone-era DRAM, which served millions of consumer devices, AI HBM demand is concentrated in hyperscaler data centers where the economics of substitution are weak. Nvidia's GPUs, for example, are architecturally designed around HBM bandwidth — there is no commodity DRAM alternative.

SK Hynix holds the commanding position in HBM3E, the current-generation product used in Nvidia's H200 and H100 series processors, with Samsung Electronics working to recover its competitive position.

Monday's Market: Sector Rotation Signals Selective Confidence

Monday's intraday KOSPI recovery to 7,503 (+0.37%) showed clear sector rotation. The laggards were the semiconductor names:

| Stock | Monday AM Move |

|---|---|

| SK Innovation (096770.KS) | +8.36% |

| LG Energy Solution (373220.KS) | +4.45% |

| Hyundai Motor (005380.KS) | +3.72% |

| Samsung Electronics (005930.KS) | +0.70% |

| SK Hynix (000660.KS) | -4.36% |

The rotation toward EV and battery names suggests some institutional investors are reducing chip exposure while adding to beaten-down EV supply chain stocks — not a dismissal of the BOK's thesis, but a tactical repositioning ahead of clearer earnings signals.

Risk Factors

The BOK's optimistic baseline carries three key risks: - AI ROI uncertainty: If enterprise AI deployments fail to produce measurable returns, hyperscalers may slow data center expansion in 2025–2026, denting HBM demand - Geopolitical overlay: US-Iran tensions escalated over the weekend, contributing to KOSPI's negative open on July 13 — a reminder that macro shocks can override sector fundamentals - Rate environment: The Bank of Korea is widely expected to raise its policy rate at the July 16 Monetary Policy Committee meeting — the first hike since 2023. While a rate hike signals economic confidence, it also adds cost-of-capital pressure to highly indebted tech supply chains

Investor Takeaway

The Bank of Korea's report represents a policy-level endorsement of the AI chip supercycle narrative. For foreign investors holding KOSPI semiconductor positions, the central bank's analysis — backed by JPMorgan, Goldman Sachs, and Morgan Stanley's 2027+ forecasts — reinforces the thesis that the current selloff is driven by sentiment rather than deteriorating fundamentals. At KOSPI forward P/E levels near 2008 crisis lows, the risk-reward for long-term holders appears asymmetric, provided AI adoption continues on its current trajectory.

The July 16 BOK rate decision and upcoming Q2 detailed earnings from Samsung Electronics and SK Hynix will be the next key data points for reassessing this thesis.

Sources: Korea Herald — BOK report · Korea Herald — KOSPI rebound