TL;DR

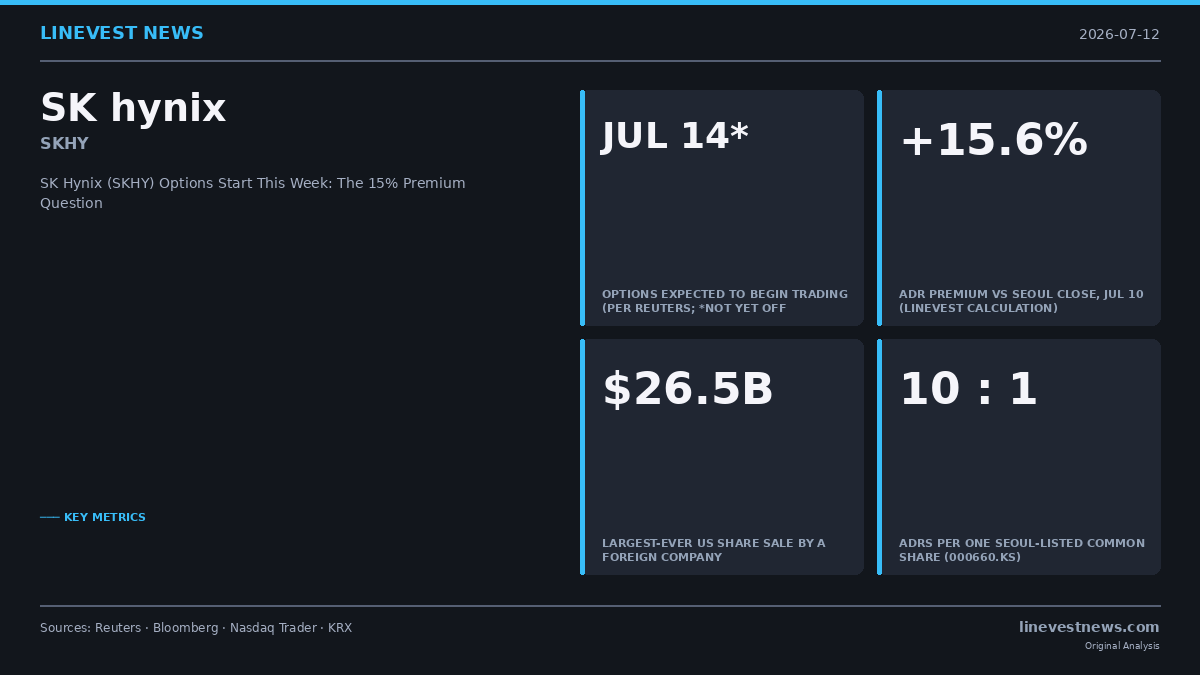

- Options on SK Hynix's Nasdaq-listed ADR (ticker: SKHY) are expected to begin trading as soon as Tuesday, July 14 — two business days after Friday's debut, according to Reuters, citing exchange sources. The exchanges have not yet published an official listing notice.

- 10 ADRs equal 1 Seoul-listed common share (000660.KS). At Friday's close of $168.01, the ADR implies roughly ₩2.52 million per common share — a premium of about 15–16% over the Seoul close of ₩2,180,000.

- Whether that premium holds depends on conversion rules SK Hynix has not publicly finalized. If depositing Seoul shares into new ADRs is restricted, arbitrage cannot close the gap — the pattern that has kept TSMC's US listing at a persistent double-digit premium to Taipei for years.

- The first big test for the new options: SK Hynix's first earnings report as a US-listed name, expected in late July (the exact date has not been confirmed by the company).

What Is Happening

US exchange operators including Cboe Global Markets and Nasdaq expect to list options on SK Hynix's American depositary receipts two business days after the stock's trading debut, Reuters reported on July 10, citing two sources familiar with the matter. Counting from Friday's July 10 debut, that points to Tuesday, July 14; if the exchanges count from Monday's first regular-way session under the permanent SKHY ticker, the start could slip a day. The options will trade under existing regulatory rules and the Options Listing Procedures Plan framework — the same fast-track process that brought SpaceX options to market in June, where they drew record first-day volumes.

The listing they follow was itself a record. SK Hynix priced 177.9 million ADRs at $149 each on July 9, raising $26.5 billion — the largest US share sale ever completed by a foreign company, surpassing Alibaba's $25 billion in 2014. The ADRs opened at $170 on July 10 under the when-issued ticker SKHYV and closed at $168.01, up 12.8% from pricing. The permanent ticker SKHY takes effect from Monday, July 13, per Nasdaq's trader notice. Proceeds are earmarked for manufacturing expansion in Korea and equipment purchases, including EUV lithography scanners.

The derivative ecosystem is forming quickly around the ADR: GraniteShares plans to launch 2× leveraged long and short ETFs (SKUU and SKDD) on July 13 — one day before options are expected to begin trading. (For the debut-day recap, see our earlier coverage: SK Hynix's $26.5B ADR debut.)

The Premium Math Every SKHY Buyer Should Run

A US investor buying SKHY today is not paying the Seoul price. Here is the arithmetic as of Friday's close:

| Metric | Value |

|---|---|

| SKHY close (Jul 10) | $168.01 |

| ADR ratio | 10 ADRs = 1 common share |

| Implied price per common share | $1,680.10 |

| USD/KRW (Jul 10) | ≈ ₩1,500 |

| Implied value in won | ≈ ₩2,520,000 |

| 000660.KS close (Jul 10, KRX) | ₩2,180,000 |

| Implied ADR premium | ≈ 15.6% |

The premium was not born this large. The $149 pricing came in only about 3% above where the Seoul shares were trading; Friday's pop did the rest. Seoul, notably, did not follow — 000660.KS actually slipped 0.3% on Friday. The gap is a New York phenomenon.

Why the Premium Could Persist — or Snap Shut

Under the deposit arrangement, the Korea Securities Depository holds the underlying shares, and ADR holders can surrender ADRs for Seoul-listed stock. The unresolved question — flagged by Bloomberg before the debut and still not publicly answered — is the reverse direction: whether investors can freely deposit Seoul shares to create new ADRs. That single mechanism decides everything. If creation is open, arbitrageurs buy in Seoul, convert, sell in New York, and the premium compresses toward FX and friction costs. If creation is restricted, the premium becomes structural.

The precedent is TSMC, whose NYSE-listed ADRs have traded at a persistent double-digit premium to the Taipei line precisely because the conversion channel is constrained. UBS made the call explicit before the debut, recommending clients buy the ADR and short the Seoul shares — Wall Street is already trading the gap as if it will widen or at least hold.

Options change the texture of this trade in three ways. First, hedging: a US investor holding SKHY at a 15% premium to intrinsic Seoul value can now buy protective puts against both a chip-cycle correction and a premium collapse — two distinct risks stacked in one instrument. Second, implied volatility discovery: the late-July earnings report (date still unconfirmed) will be the first time the market prices SK Hynix event risk in listed US options, and early IV levels will likely borrow from Micron's surface until SKHY builds its own history. Third, price discovery migrates westward: with options, leveraged ETFs, and the ADR all trading in US hours, Seoul's 9:00 AM open increasingly starts where New York left off — the tail beginning to wag the dog.

What It Means for Korea

For 000660.KS holders, the premium is a signpost, not free money. If SK Hynix or Korean regulators later open full two-way fungibility, the premium compresses — likely toward the Seoul price rather than the New York one. Watch three things this week: the official options listing notice (July 14–15), the SKHY-versus-000660 spread on the first days of regular-way trading, and KRX short-sale balances in 000660 as arbitrage positions build against the Seoul line. And note the calendar: the Bank of Korea meets on July 16, and any surprise in the won moves the premium math directly — a 2% currency swing is worth roughly 2 points of premium on its own.

Sources: Reuters via Yahoo Finance (options timing); Bloomberg (offering size, first-day close); Nasdaq Trader Notice DTN2026-11 (ticker schedule); SK hynix Newsroom; Bloomberg, Jun 25 (fungibility); KRX/Google Finance (000660.KS close); TradingEconomics (USD/KRW). Premium calculation is LineVest's own, based on July 10 closing prices and an exchange rate of ₩1,500 per dollar.

This article is journalism, not investment advice. LineVest is not a registered investment adviser.