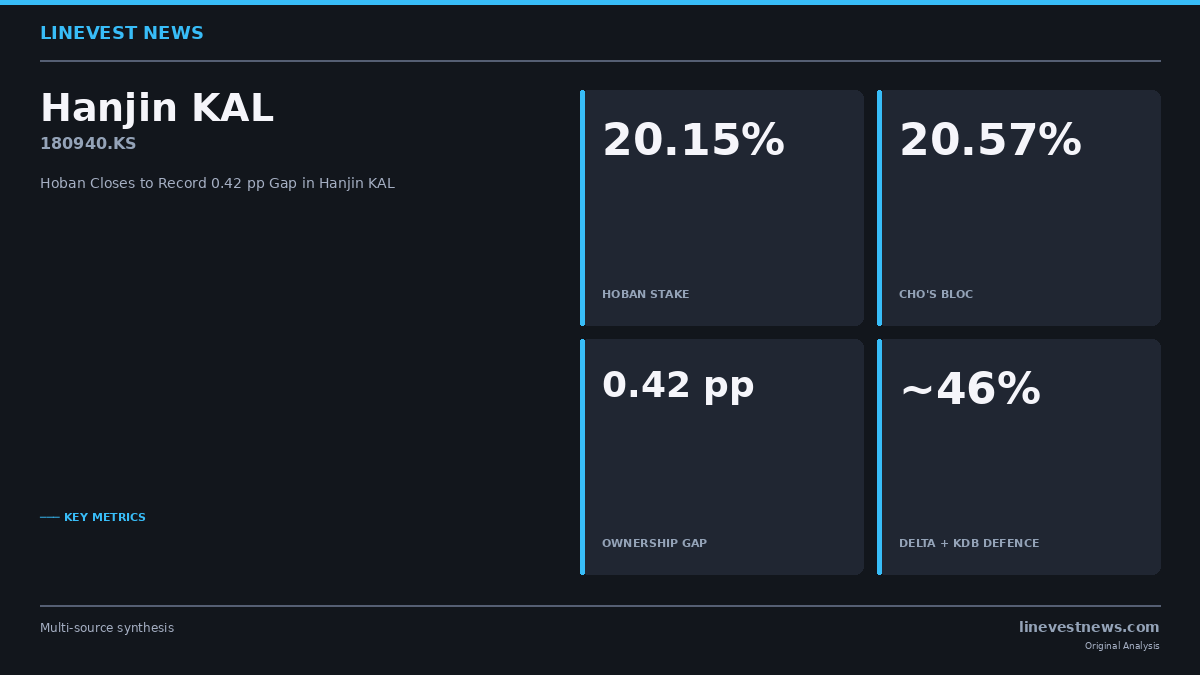

TL;DR - Hoban Group lifted its Hanjin KAL (180940.KS) stake to 20.15% on July 11 after purchasing 1.13 million shares in the open market - Walter Cho's controlling bloc sits at 20.57% — a gap of just 0.42 percentage points, the slimmest margin on record - Cho's defence alliance (Delta Air Lines 14.9% + Korea Development Bank 10.56%) controls roughly 46% combined, providing a substantial buffer - National Pension Service (NPS) at 5.46% is the pivotal swing bloc that neither side controls - If Hoban ever triggers a full proxy contest, Hanjin KAL's role as holding company for Korean Air (003490.KS) could face board-level disruption just as the airline digests its Asiana integration

Part A: What Happened

Hoban Group, the Korean conglomerate known for construction and hospitality, disclosed on July 11, 2026 that it had purchased an additional 1.13 million shares of Hanjin KAL (180940.KS) on the open market, lifting its collective stake across four affiliates to 20.15% from the prior 18.46%.

The breakdown by affiliate:

| Affiliate | Stake |

|---|---|

| Hoban Construction | 11.50% |

| Hoban Hotel & Resort | 8.34% |

| Hoban Industrial | 0.17% |

| Hoban Co. | 0.15% |

| Total | 20.15% |

Hanjin KAL is the holding company at the apex of Hanjin Group, which controls Korean Air (003490.KS), Korea's flagship international carrier.

Walter Cho — chairman of Hanjin Group and CEO of Korean Air — holds a personal stake of 5.78%, and his broader controlling bloc, including Delta Air Lines' 14.9% and Korea Development Bank's 10.56%, commands roughly 46% combined of Hanjin KAL.

Despite that defence, the gap between Hoban and Cho has now compressed to a barely perceptible 0.42 percentage points — a record low since Hoban first emerged as a major shareholder in 2022.

Hoban's regulatory filing stated the transaction was "purely an investment" and that the group "does not seek management control."

Part B: Market and Investor Implications

A Pattern of Deliberate Escalation

Hoban has been quietly building its Hanjin KAL position across multiple transactions:

| Year | Transaction | Stake After |

|---|---|---|

| 2022 | Acquired KCGI Private Equity's stake | ~15% |

| 2023 | Purchased 5.85% from Pan Ocean | ~18.46% |

| July 2026 | Open-market purchase (1.13M shares) | 20.15% |

This escalating acquisition pattern bears a structural resemblance to Hoban's 2015 foray into Kumho Industrial (then the parent of Asiana Airlines), where the group accumulated 6.16% before eventually retreating. That attempt never reached a formal proxy contest — but the trajectory raises questions about whether Hoban's repeated "investment-only" framing understates its longer-term strategic ambitions.

Cho's Defences Remain Strong

Despite the narrowing gap, Walter Cho's position appears difficult to dislodge at any coming annual general meeting (AGM). The full ownership picture:

| Shareholder | Stake | Role |

|---|---|---|

| Hoban (total) | 20.15% | Challenger |

| Walter Cho (personal) | 5.78% | Incumbent |

| Delta Air Lines | 14.9% | Allied to Cho |

| Korea Development Bank | 10.56% | Allied to Cho |

| Cho's bloc combined | ~46% | Controlling |

| National Pension Service | 5.46% | Swing voter |

Delta Air Lines's 14.9% stake functions as a strategic cross-shareholding linked to the carriers' transatlantic alliance, not a passive financial investment. Delta has historically backed Cho's board slate. Similarly, Korea Development Bank's block reflects the government-backed lender's involvement in Hanjin's prior debt restructuring — not a position likely to switch alignment lightly.

NPS: The Pivotal Swing Bloc

At 5.46%, the National Pension Service (NPS) is the most consequential undecided party. Korea's NPS has publicly committed to applying stewardship codes at large-cap KOSPI companies — including voted opposition to governance-deficient proposals. If Hoban were to mount a formal proxy fight with a credible board slate, NPS's vote could prove pivotal in any close contest.

For now, there is no public indication that NPS has aligned with Hoban.

Korean Air: Post-Asiana Integration Overhang

The governance uncertainty at the Hanjin KAL holding level creates a secondary risk factor for Korean Air (003490.KS) shareholders. Korean Air completed the long-contested acquisition of Asiana Airlines in 2024, following regulatory approvals from the EU, US DOJ, and Japan's JFTC, and is currently in an integration phase covering fleet harmonisation, route rationalisation, and labour relations across two legacy carriers.

Any board-level disruption at Hanjin KAL — even short of a control change — could complicate Korean Air's ability to execute integration decisions that require board confidence and long-horizon capital commitments.

That said, with Cho's ~46% alliance intact, a near-term control shift weighs as unlikely. The more plausible scenario is sustained market speculation ahead of Hanjin KAL's next AGM, typically scheduled in March of each year.

Sector Context

Hanjin KAL is thinly covered by foreign equity analysts relative to KOSPI peers, and the corporate structure — a holding company whose principal asset is the country's dominant airline — is opaque to most international investors. With Korean Air now the consolidator of the domestic aviation market following the Asiana deal, holding-company governance matters more than it once did.

Hoban's escalating presence keeps that structure under scrutiny and may set up an extended, low-intensity shareholder confrontation similar to past Korean conglomerate proxy skirmishes.

Sources: - Korea Herald — Hoban tops 20% in Hanjin KAL, narrows gap with Cho

This article is for informational purposes only and does not constitute investment advice. LineVest News is not a registered investment adviser.