Korea's Financial Giants Enter Crypto as Mirae Asset Clears Korbit Deal While Naver-Dunamu Tie-Up Stalls

South Korea's financial establishment is moving to claim a stake in the country's regulated cryptocurrency market, but deal size and market structure are producing starkly different regulatory outcomes.

Part A: What Happened

Mirae Asset Clears Korea's First Financial-Group Crypto Takeover

Korea's Fair Trade Commission (FTC) approved Mirae Asset Consulting's acquisition of Korbit on July 9, clearing the country's first takeover of a licensed won-based cryptocurrency exchange by an affiliate of a major financial conglomerate.

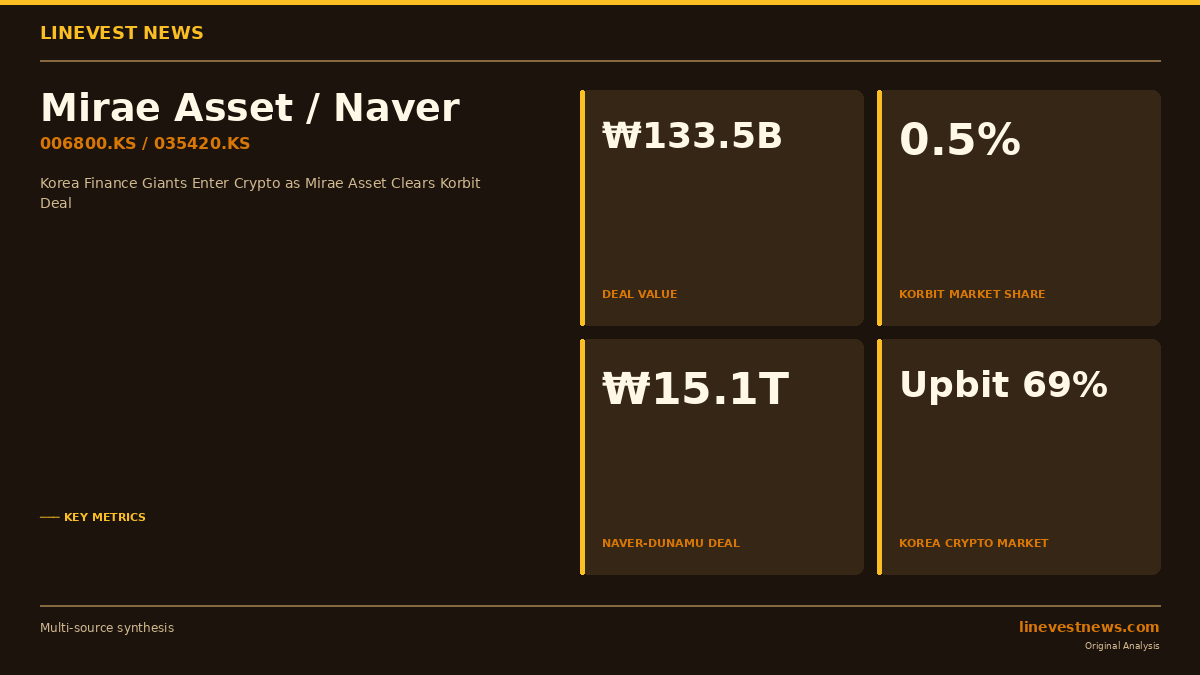

The deal values Korbit at approximately ₩133.5 billion (USD 88.8 million), with Mirae Asset Consulting acquiring a 92.06% stake comprising 26.91 million shares. The FTC determined the transaction posed minimal competitive risk — a straightforward conclusion given Korbit's position in the market: the exchange holds roughly 0.5% of South Korea's retail cryptocurrency trading volume, far behind Upbit's dominant 69% and Bithumb's 28%.

The agreement was originally signed in February 2026 and navigated the antitrust review process in under five months.

Naver-Dunamu Merger Pushed to December

The contrasting picture emerges when comparing the Korbit deal to Naver Financial's proposed acquisition of Dunamu, the operator of Upbit, Korea's dominant exchange. That transaction — valued at roughly ₩15.1 trillion (USD 10 billion) for Dunamu against a Naver Financial valuation of ₩4.9 trillion — remains mired in regulatory review.

The deal's completion deadline has been extended twice, most recently to December 31, 2026, after the original June 30 target and a subsequent September 30 extension both proved unworkable. A pivotal shareholder meeting has been rescheduled to November 19.

The FTC has solicited antitrust opinions from 18 brokerage firms, with industry participants raising concerns that a combined Naver-Upbit entity would control an outsized share of both simple payment flows and virtual asset trading. Adding complexity, regulators are examining whether Naver meets shareholder eligibility requirements under evolving digital asset legislation, and Dunamu carries a prior regulatory blemish: a three-month partial business suspension issued under Korea's Special Financial Transaction Information Act.

Part B: Korea Market Impact

Mirae Asset (006800.KS): Building a Digital Asset Platform

For Mirae Asset, the Korbit acquisition is less about immediate revenue — Korbit's 0.5% market share generates limited transaction fees at current volumes — and more about acquiring licensed infrastructure ahead of Korea's developing digital asset regulatory framework.

Mirae Asset Group's stated roadmap for Korbit encompasses stablecoins, custody services, real-world asset tokenization, digital payments, and storage solutions. A Mirae Asset official framed the strategic rationale plainly: "Digital assets are no longer a short-term investment vehicle for certain investors, but a new asset class in the global financial industry."

The group's asset management division, with roughly ₩400 trillion in assets under management, provides a client base and distribution network that Korbit — previously a standalone exchange competing on volume alone — could not have accessed independently. The integration may allow Mirae Asset to offer tokenized fund products and stablecoin settlement rails to institutional and high-net-worth clients.

Mirae Asset Consulting is also not alone in the space: Korea Investment & Securities has indicated its own interest in the crypto sector, suggesting incumbent brokerages view exchange ownership as a structural requirement to participate in Korea's coming digital asset product market.

Naver (035420.KS): High Stakes, High Scrutiny

The Dunamu deal's scale is the primary driver of its regulatory difficulty. Upbit processes roughly 69% of Korea's retail cryptocurrency volume, and a Naver-backed entity owning that share would represent a level of market concentration that antitrust regulators across jurisdictions have historically resisted.

Beyond antitrust, the pending Digital Asset Basic Act introduces structural uncertainty. If passed in its current form, the legislation could impose mandatory shareholding limits on cryptocurrency exchange operators — a provision that would require Naver Financial to restructure the deal terms before or immediately after closing.

Upbit's market position also makes the deal's strategic logic more compelling for Naver and more concerning for regulators simultaneously. Naver Pay, which processes daily mobile payment volumes of approximately ₩736 billion across its e-commerce ecosystem, would connect to an exchange that handles the dominant share of Korean won-crypto conversion — a cross-market integration that has drawn specific scrutiny from the FTC.

Korea Crypto Market Structure

The differential treatment of these two deals illustrates the emerging principle in Korea's crypto regulation: transactions that add institutional-grade risk management and capital backing to small, struggling exchanges are welcome; transactions that concentrate market power at dominant platforms face proportionally higher scrutiny.

Korbit ranked fourth in a five-exchange won-based market; Upbit is the market. The FTC's speed on one and deliberateness on the other reflects that distinction rather than any broader uncertainty about financial groups entering the asset class.

For Korea's KOSPI-listed financial sector, the underlying dynamic is positive. The Virtual Asset User Protection Act, which took effect in 2024, provided the compliance framework that made institutional ownership of exchanges legally viable. If the Naver-Dunamu deal closes by year-end, Korea will have its three largest regulated exchanges — Upbit, Bithumb, and Korbit — all held by or connected to mainline financial institutions, a transformation from the independent operator model that defined the 2017–2022 crypto cycle.

Sources: Korea Times · KED Global · Seoul Economic Daily · Korea Herald