South Korea is quietly reversing course on natural gas. After years of pledging to shrink liquefied natural gas's role in the country's power mix under long-term decarbonisation targets, Seoul is now reconsidering — driven by an electricity gap that no renewable build-out can close fast enough for the country's AI and semiconductor ambitions.

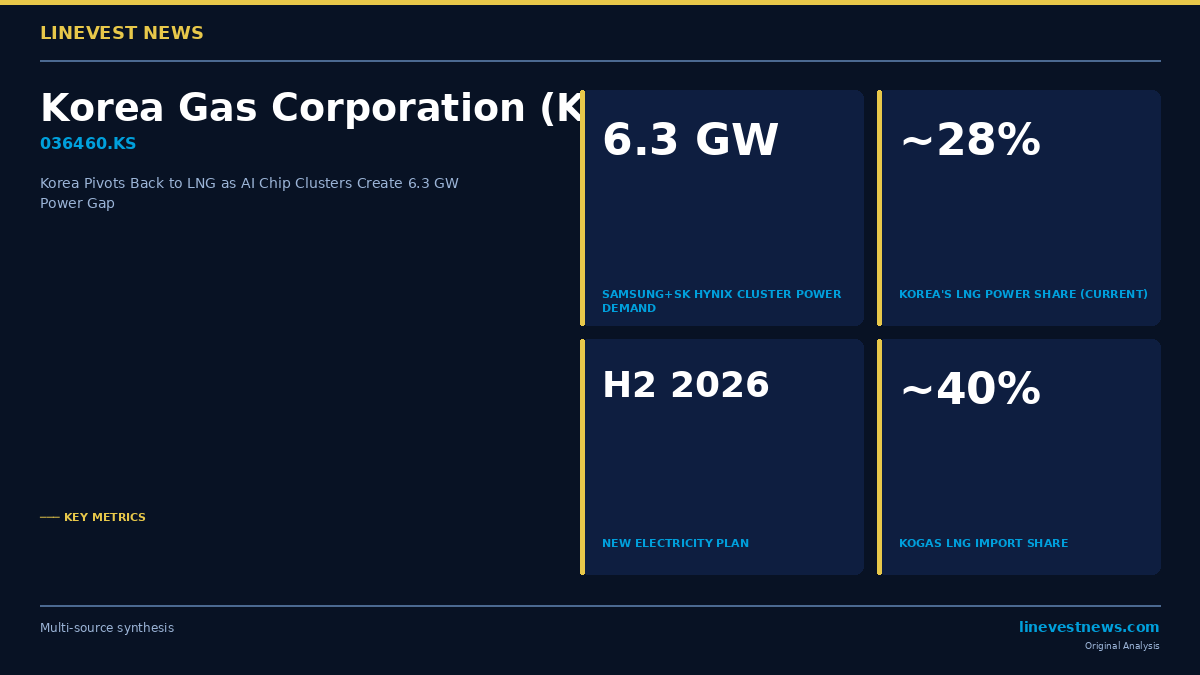

The Ministry of Trade, Industry and Energy is expected to propose a sharp increase in LNG's share of the power mix in the forthcoming 11th Basic Plan for Long-Term Electricity Supply and Demand, due later this year, according to The Korea Times. The plan would also consider deploying LNG combined-cycle generation to meet part of the 6.3-gigawatt power demand from Samsung Electronics (005930.KS) and SK Hynix's (000660.KS) planned semiconductor cluster in Korea's southwestern Honam region.

The 6.3 GW Problem

Advanced semiconductor fabs are among the most power-hungry industrial facilities on earth. A leading-edge DRAM or HBM production campus requires continuous, near-perfectly clean electricity at extremely stable voltage and frequency — any interruption of even milliseconds can destroy billions of won in product in an instant.

The Samsung–SK Hynix cluster envisioned for the Honam region, which would cluster advanced memory and logic capacity alongside AI data centre infrastructure, has flagged a power requirement of 6.3 gigawatts. For context, Korea's total installed power capacity is roughly 145 GW, and the country's winter peak load is around 90 GW. The cluster's demand alone would exceed the generating capacity of several mid-size countries.

Renewable energy — the government's preferred decarbonisation vehicle — cannot meet this need on its own. Solar generation drops to near zero at night and falls sharply in winter, while Korea's geography limits large-scale wind development. Grid-scale battery storage helps at the margins but cannot provide the sustained, 24-hour baseload that semiconductor fabs require.

LNG combined-cycle plants, by contrast, can be built in roughly two to three years, ramp up and down within minutes to balance intermittent solar and wind, and run at high capacity factors when industrial demand is constant. That flexibility has moved LNG back onto policymakers' priority list.

Part A: Policy Shift

The 10th Electricity Supply and Demand Plan, adopted in the previous administration, had targeted reducing LNG's share of Korea's power generation mix, which currently stands at approximately 27–30% of the total, as part of a broader shift toward renewables and a conditional nuclear expansion. That target is now under review.

Officials are assessing whether LNG combined-cycle plants, which can be co-located with or near large industrial loads, can bridge the gap between what renewables can deliver and what the semiconductor cluster actually needs. The proposal under review would allow LNG to serve as a firm, dispatchable backup behind a renewable-heavy grid — a "swing fuel" model similar to what Germany and Japan adopted after their respective energy crises.

No formal decision has been announced, and the 11th Electricity Plan is expected to be debated through the second half of 2026.

Part B: Korea Market Implications

KOGAS: Volume Upside

Korea Gas Corporation (KOGAS, 036460.KS) handles approximately 40% of Korea's LNG procurement through its long-term supply contracts and regasification terminals, making it the most direct listed beneficiary of any upswing in domestic LNG demand.

KOGAS has seen its share price under pressure in recent years as the government's clean-energy push raised structural demand concerns. A formal policy declaration that LNG will maintain or expand its role would remove a significant overhang. Higher LNG throughput volumes translate directly into higher regulated-asset revenues for KOGAS, whose domestic tariff structure is set on a cost-plus basis by the government.

KOGAS also operates LNG import terminals and pipelines and has been expanding its international LNG trading desk. If Korea's domestic demand floor rises, KOGAS gains negotiating leverage in renewing long-term supply contracts — currently priced with some downside risk baked in.

KEPCO: A Two-Edged Sword

Korea Electric Power Corporation (KEPCO, 015760.KS), the state-owned utility, operates most of Korea's power plants through its generating subsidiaries and buys power from independent producers. Higher LNG dispatch is a double-edged sword for KEPCO.

On the positive side, LNG power plants are dispatchable and can command higher capacity-market prices than intermittent renewables. KEPCO's generating subsidiaries (including KEPCO KPS, 051600.KS, which maintains power plant equipment) would see higher utilisation.

On the negative side, KEPCO purchases LNG fuel at global market prices, and its retail tariffs are regulated by the government, which has been slow to raise them despite the global energy price surge of 2022–2024. If LNG commodity prices remain elevated and the tariff freeze continues, KEPCO's balance sheet could worsen — KEPCO already carries one of the largest corporate debt loads in Korea at approximately KRW 206 trillion.

Semiconductor Makers: Reliability Over Cost

For Samsung Electronics and SK Hynix, grid reliability matters more than marginal electricity cost. Advanced HBM (High Bandwidth Memory) production — SK Hynix's defining product for the AI chip boom — requires cleanroom environments with zero unscheduled power interruptions. Samsung's DRAM and NAND fabs have similar requirements.

Both companies are known to invest heavily in on-site backup power. The broader policy question is whether Korea's main grid can deliver the stability and redundancy that leading-edge fabs require. A firm LNG baseload layer under a renewable-heavy grid would meaningfully reduce the risk of brownouts that could cost fabs hundreds of billions of won per incident.

LNG Shipping: Latent Demand Signal

Korea is already the world's second or third-largest LNG importer by volume. If domestic demand expands to support semiconductor clusters, Korean shipping companies with LNG carrier exposure — including Pan Ocean (028670.KS), which operates an LNG segment generating margins above 44% — stand to benefit from tighter LNG freight markets over the medium term.

Energy Transition Tension

The policy reversal reflects a broader tension running through Korea's industrial strategy. The country has simultaneously committed to aggressive carbon-neutrality targets and to dominating the global AI-chip supply chain — two ambitions that pull in opposite directions on energy policy. How that tension resolves will have lasting implications for power-sector capex, KOGAS's contract pipeline, and the cost base of Korea's semiconductor champions.

Sources: Korea Times · Ministry of Trade, Industry and Energy (electricity planning) · Company filings (KOGAS, KEPCO, Samsung Electronics, SK Hynix)