HLB's Liver Cancer Combo Hits Third FDA Roadblock as China Partner's Plant Fails Inspection

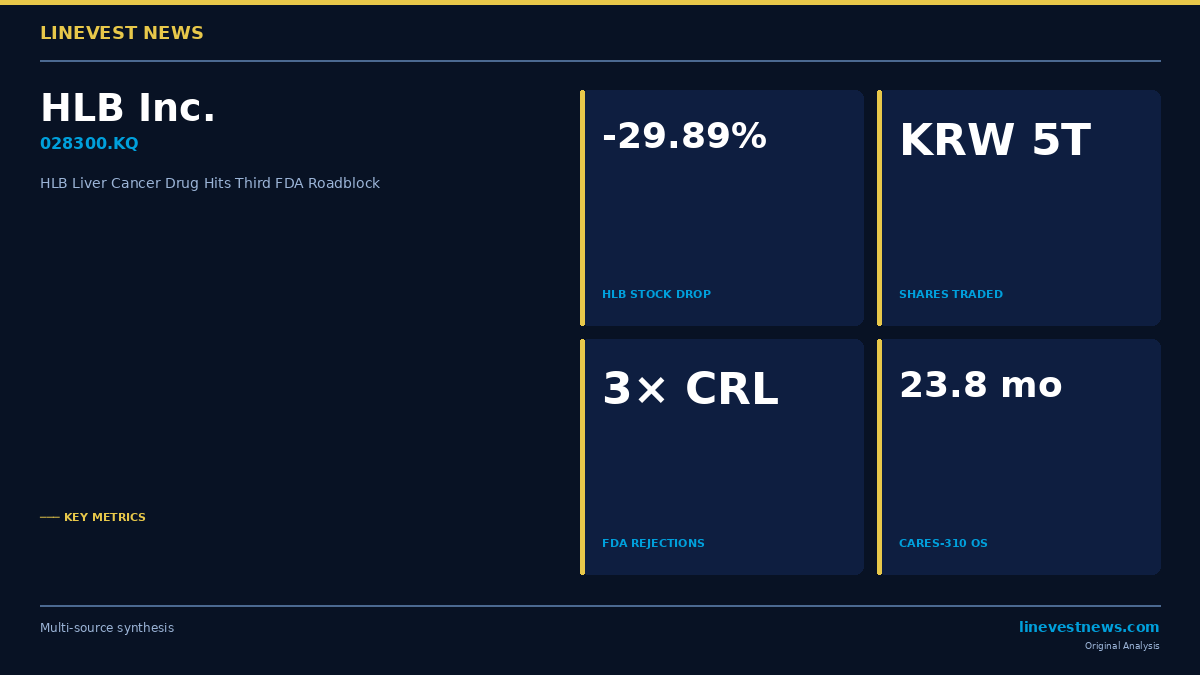

HLB Inc. (028300.KQ) and its U.S. subsidiary Elevar Therapeutics received a third complete response letter (CRL) from the U.S. Food and Drug Administration on July 9, 2026, halting another attempt to win approval for the rivoceranib-camrelizumab combination therapy in unresectable hepatocellular carcinoma (HCC). The repeated setbacks — the third such rejection in just over two years — triggered a cascading sell-off across the entire HLB Group on Korean exchanges, with HLB shares hitting the daily lower limit.

Part A: The Rejection and Its Cause

The CRL targeted rivoceranib's new drug application (NDA), but the FDA's concerns were directed not at the drug's clinical profile but at the manufacturing facility of Hengrui Pharmaceuticals, the Chinese partner that produces both rivoceranib and camrelizumab. During a routine current Good Manufacturing Practice (cGMP) inspection at Hengrui's facility in April 2026, FDA inspectors issued a Form 483 — a document that notifies manufacturers of conditions or practices that may violate regulations.

"This CRL did not identify any deficiencies related to clinical efficacy and safety data, nor any requirement for additional clinical trials," Elevar CEO Kim Dong-gun said in a statement. The FDA indicated it would not approve the NDA until the manufacturing site addressed the cited deficiencies and demonstrated cGMP compliance.

The three CRLs have followed a consistent pattern. The first, issued in May 2024, also cited manufacturing issues at Hengrui's facility. The second, in March 2025, again pointed to the same Chinese plant. In each instance, the FDA declined to question the underlying efficacy or safety data from the CARES-310 phase 3 trial.

CARES-310 Clinical Data Remains Intact

The clinical case for rivoceranib plus camrelizumab is well established. In the CARES-310 randomized phase 3 trial involving 543 patients with treatment-naïve unresectable HCC, the combination produced a median overall survival (OS) of 23.8 months versus 15.2 months for sorafenib (HR 0.64; 95% CI 0.52–0.79; p<0.0001). The 24-month OS rate was 49% for the combination versus 36.2% for sorafenib, with the advantage maintained at 36 months (37.7% vs. 24.8%). The objective response rate was 26.8% versus 5.9%, and median progression-free survival was 5.6 versus 3.7 months. These results have remained uncontested across all three regulatory cycles.

Part B: Korea Market Implications

Immediate Market Reaction

HLB shares, which had been trading at KRW 52,200 before the news broke, fell 29.89% to KRW 36,600 — the daily permissible lower limit on the Korea Exchange — as the market opened on July 10. Approximately KRW 5 trillion (USD 3.7 billion) worth of HLB shares changed hands during the session, reflecting the depth of investor frustration after two years of repeated setbacks.

The damage spread across all listed entities in the HLB Group. On KOSDAQ, shares of HLB Panagene, HLB Pharmaceutical, HLB Life Science, HLB Therapeutics, and HLB bioStep also hit their respective daily lower limits in early trading, indicating that investors have long priced the combination therapy's eventual FDA approval into the group's aggregate valuation.

China CMO Dependency: A Systemic Biotech Risk

The HLB case illustrates a structural vulnerability that extends beyond a single company. Korean biotechs with pipeline assets partly or entirely manufactured in China face an inherent regulatory risk that their clinical data alone cannot resolve. Hengrui's facility has now triggered three consecutive CRLs without any progression toward resolving the underlying cGMP deficiencies, raising questions about the pace of remediation and Elevar's leverage over its Chinese partner's operational compliance.

For KOSDAQ biotech investors, the distinction between a clinically failed drug and a manufacturing-blocked drug matters significantly. The former typically signals the end of a development program; the latter preserves the asset's value but subjects the timeline — and the stock — to factors largely outside the sponsor's control. In HLB's case, the FDA has now twice explicitly confirmed that the clinical data package is acceptable. That validation offers a theoretical floor under the asset's intrinsic value, even as the stock reprices the extended timeline risk.

Path to Approval

HLB stated it intends to consult with the FDA on required remediation steps and pursue resubmission as soon as possible. The resolution path involves Hengrui addressing the Form 483 observations, completing any follow-up inspection, and obtaining FDA confirmation of compliance before a resubmission can be accepted. Historically, Form 483 resolutions have ranged from three months to over a year, depending on the severity and number of observations. Given that two prior CRLs pointed to the same facility, the remediation challenge may be more deeply rooted than a routine quality system correction.

KOSDAQ Biotech Sector Context

HLB had been among the most closely watched KOSDAQ biotechs, with its stock price reflecting cumulative investor confidence in an eventual FDA breakthrough. The ₩5 trillion in share turnover on July 10 underscores the degree to which Korean retail investors had concentrated bets on approval materialization. Korean institutional investors and fund managers now face questions about appropriate position sizing in KOSDAQ names whose regulatory timelines are anchored to Chinese CMO compliance — a risk factor that traditional efficacy-based drug development models do not adequately capture.

Until Hengrui's manufacturing issues are formally resolved and acknowledged by the FDA, rivoceranib-camrelizumab remains clinically validated but commercially indefinite. The outstanding question for investors is not whether the drug works — the CARES-310 data answers that — but whether and how quickly Hengrui can achieve the manufacturing compliance the FDA has consistently required.

Sources: Seoul Economic Daily (English) · Korea Biomed Reporter · Chosunbiz · Hankyung