HD Hyundai Energy Solutions (322000.KS) Posts Record Q1 Profit as Solar Cycle Turns, Revenue Near-Doubles

HD Hyundai Energy Solutions (KOSPI: 322000), South Korea's second-largest solar module maker, reported a dramatic first-quarter turnaround in its Q1 2026 regulatory filing with DART on May 15, 2026. The company swung from operating losses to an 18.2% operating margin — one of the highest among non-Chinese solar manufacturers globally — as three tailwinds converged: domestic policy support, pre-tariff U.S. pull-forward demand, and a structural recovery in solar module pricing.

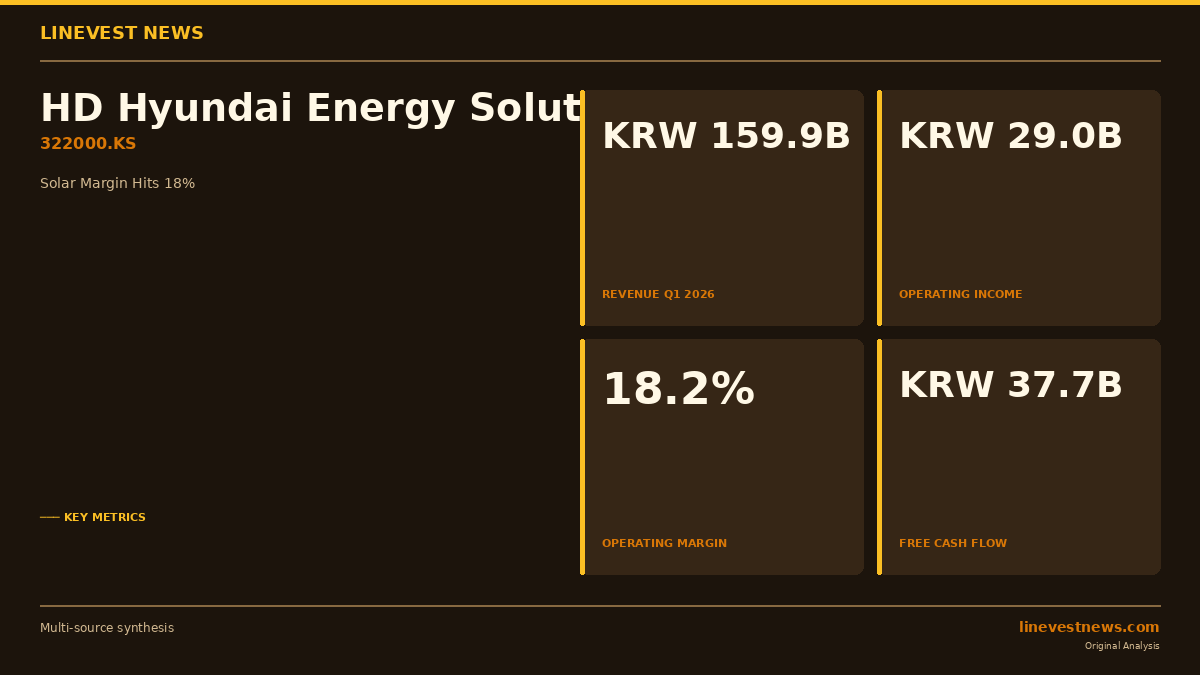

Part A: Q1 2026 Financial Summary

Consolidated revenue surged 87.6% year-on-year to KRW 159.9 billion (USD 116.7 million) from KRW 85.3 billion (USD 62.2 million) in Q1 2025. Operating income swung from a loss of KRW 3.0 billion to a profit of KRW 29.0 billion, pushing the operating margin to 18.2% — a 21.8 percentage-point improvement. Net income followed, turning from a loss of KRW 1.1 billion to a profit of KRW 22.3 billion (net margin: 13.9%).

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Revenue | KRW 85.3B | KRW 159.9B | +87.6% |

| Operating Income | -KRW 3.0B | +KRW 29.0B | Turnaround |

| Operating Margin | -3.6% | 18.2% | +21.8pp |

| Net Income | -KRW 1.1B | +KRW 22.3B | Turnaround |

| Operating CF | -KRW 2.5B | +KRW 39.2B | Turnaround |

Three catalysts drove the revenue jump: (1) domestic module market share expanded from 26.6% to 34.2%, supported by South Korea's new low-carbon module tax credit; (2) pre-tariff demand from U.S. distributors nearly tripled North American revenue to KRW 53.3 billion (from KRW 20.1 billion); and (3) average Mono PERC module prices recovered to USD 0.09/W from USD 0.07/W.