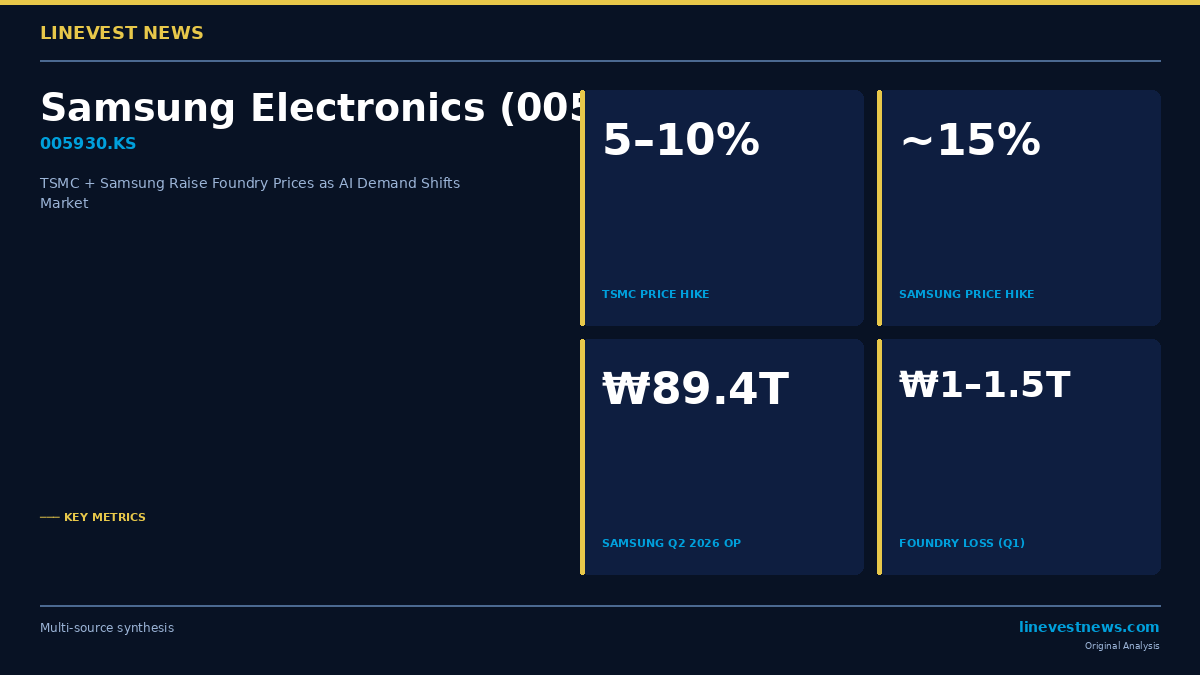

TSMC has formally notified major customers — including Nvidia, Apple and AMD — of wafer price increases of 5–10% across its 3nm, 5nm and 7nm advanced nodes, according to multiple industry sources. Concurrently, Samsung Electronics (005930.KS) has raised supply-side pricing on select advanced processes, lifting rates on 4nm, 5nm and automotive 8nm nodes by approximately 15% for new customers. The back-to-back moves mark what analysts describe as a structural transition in the foundry industry from a buyer's market, which persisted for most of the past decade, to a seller's market shaped by AI-driven demand.

Part A — What Changed and Why

Same-Process Price Increases: A Rarity Turned Norm

Historically, semiconductor foundries would charge a premium when a new process generation launched, then hold prices flat — or gradually lower them — as yields improved and equipment was depreciated. Raising the price of an existing, mature process was considered commercially untenable because it risked customer defection to competing foundries.

That calculus has changed. AI infrastructure spending has caused the demand curve for advanced node wafers to steepen faster than capacity expansions can respond. Simultaneously, the cost of developing the next-generation 2nm process — and procuring the required extreme ultraviolet (EUV) lithography equipment — has grown substantially, requiring higher revenue per wafer to justify continued R&D investment.

Under these conditions, TSMC communicated the 5–10% rate increases to customers in recent weeks. The move follows an earlier round of price adjustments TSMC implemented in 2025. Industry observers note that for the first time, process maturity is no longer the primary driver of pricing — market supply-demand balance and cost recovery on next-generation tooling are.

Samsung's Targeted Rate Adjustment

Samsung's response is narrower in scope. The company is targeting processes where demand is running ahead of available capacity: advanced 4nm and 5nm nodes that serve AI chip designers, and the automotive-grade 8nm node where EV-related orders remain robust despite broader automotive sector softness.

The ~15% figure applies to new contract negotiations rather than existing long-term agreements, a distinction Samsung sources made to soften the optics of the move. Unlike TSMC's broader notification across its customer list, Samsung's adjustment is described internally as a unit price normalization rather than a blanket hike — the company continues to price competitively on nodes where capacity is underutilized.

Samsung's non-memory (System LSI + Foundry) segment has operated at a loss in recent quarters, a persistent drag on consolidated financials even as the Memory division delivered record operating income of ₩89.4 trillion in Q2 2026. Any improvement in foundry pricing power would therefore carry a disproportionate positive effect on Samsung's consolidated margins going forward.

Part B — Korean Market Implications

Samsung's Foundry Division: A Potential Margin Inflection

For investors in Samsung Electronics, the foundry pricing shift opens a secondary earnings lever beyond memory. In Q1 2026, Samsung's DS (Device Solutions) division recorded combined operating income of ₩57.2 trillion, almost entirely memory-driven; the foundry and System LSI segments were estimated to have absorbed losses of ₩1–1.5 trillion in Q1 alone.

If a 10–15% pricing improvement on high-demand nodes translates into even modest volume gains, the arithmetic on foundry profitability improves materially. Analysts tracking Samsung's structure estimate that closing half of the foundry loss gap — moving from a ₩1+ trillion quarterly loss toward break-even — would add roughly 1–2 percentage points to the consolidated operating margin, adding an incremental ₩1.5–3 trillion to full-year income at current revenue scales.

This is not a near-term catalyst; foundry margins move slowly given long production cycles and multi-year wafer supply agreements. But the directional shift from price-taker to partial price-setter is a qualitative improvement in Samsung's foundry competitive position.

Ecosystem Cost Ripple: Nvidia, Apple, AMD Bear Higher Input Costs

The flip side of supplier pricing power is customer cost pressure. Nvidia, which dominates AI GPU supply through TSMC's advanced nodes, will see its per-chip manufacturing cost rise as wafer prices move higher. At Nvidia's current scale — processing hundreds of thousands of advanced-node wafers per quarter — even a 5% price increase represents hundreds of millions of dollars in additional quarterly input cost.

For Nvidia this is manageable: its AI accelerator gross margins have consistently exceeded 70% at prevailing ASPs, leaving ample room to absorb foundry price increases or pass them downstream to hyperscaler customers (Amazon, Google, Microsoft, Meta). However, it sets a floor under GPU pricing that had previously been expected to decline as TSMC's 3nm yields matured.

Apple, TSMC's second-largest 3nm customer, faces similar dynamics ahead of its next iPhone cycle. Any upstream cost increase typically takes 12–18 months to reach the consumer device BOM, dampening the near-term price impact.

For Korean end-users of foundry services — including Samsung's own Exynos team and fabless chip designers in the Korean semiconductor ecosystem — the implication is structurally higher procurement costs for logic chip manufacture, reinforcing the secular trend toward larger captive foundry investments.

Supply Constraint Likely to Persist Through 2027

TSMC's capacity additions at its Arizona Fab 21 (4nm, now 3nm-equivalent) and its Kumamoto, Japan facility (12nm and 16nm; 6nm under construction) remain on schedule but cannot meaningfully relieve the advanced-node crunch before 2026-end at the earliest. Samsung's own Taylor, Texas fab — designed for 4nm and below — remains in ramp, with volume qualification for leading-edge designs expected through 2026.

Until at least one of these capacity expansions reaches full qualification — typically 12–18 months after silicon first passes production, meaning late 2026 or early 2027 at best — AI chip designers will remain structurally dependent on existing nodes at TSMC's existing facilities. In that environment, foundry pricing power is likely to prove durable rather than transient.

For KOSPI investors, the most actionable read-through is that Samsung's foundry segment — long a balance-sheet burden — is entering a period where pricing dynamics are less hostile. Combined with memory's ongoing supercycle and the Q2 2026 blowout results (₩89.4 trillion in operating income), the foundry pricing shift adds a third potential driver of margin expansion that was not legible in Samsung's financials even six months ago.

Sources: Chosunbiz Foundry Report · ETNews Semiconductor Coverage · TrendForce Advanced Node Analysis