The European Union has confirmed definitive anti-dumping duties on passenger car and light truck tires manufactured by Korean companies in China, imposing a 29.9% levy on Kumho Tire and Nexen Tire while Hankook Tire & Technology escapes with a minimal 3.4% rate—a divergence that reflects years of strategic investment choices that now separate the sector's winners from its most exposed players.

Part A: The Regulation

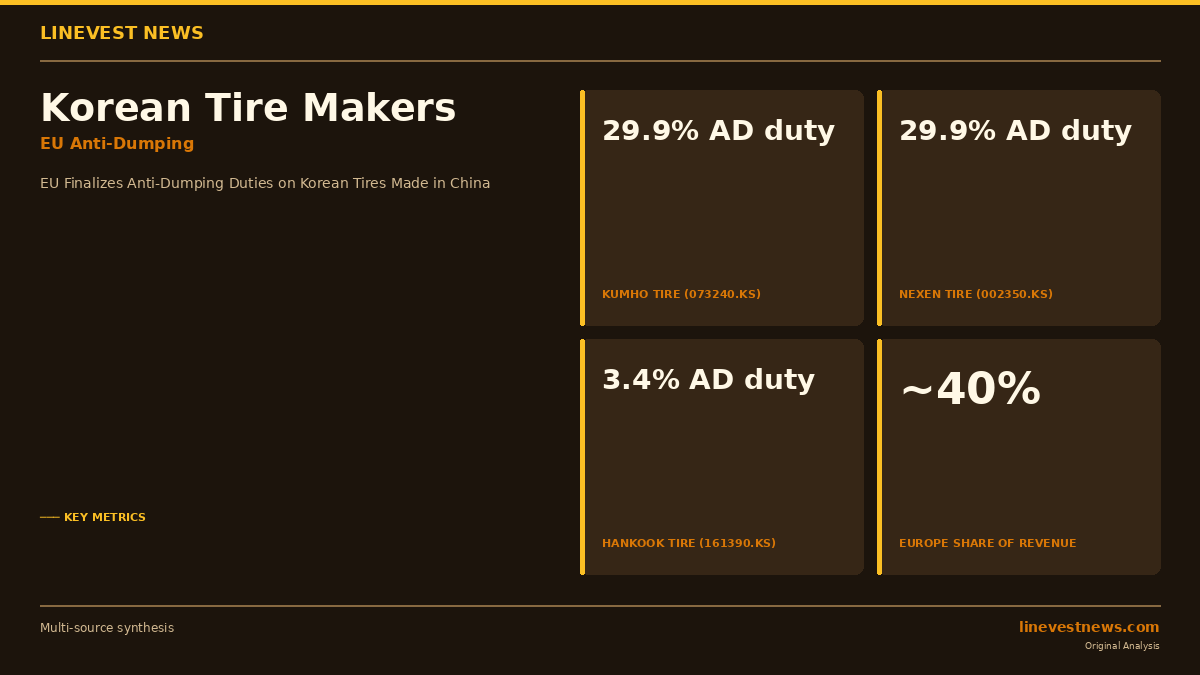

The EU's finalization follows a two-year investigation triggered by a petition from the Coalition Against Unfair Tire Imports in April 2024, which argued that low-cost Chinese-manufactured tires—including those produced by Korean companies operating plants in China—were undercutting European rivals. The EU's standard 4.5% import duty stacks on top of the anti-dumping rate, bringing the effective tariff to 34.4% for Kumho and Nexen and 7.9% for Hankook.

The regulation targets passenger vehicle and light truck tires. Europe represents roughly 40% of the combined revenue of Korea's three main listed tire makers, making the duties among the most significant regulatory events for the sector in years.

Part B: Company-Level Impact on KOSPI

Hankook Tire & Technology (161390.KS) emerges as the clearest beneficiary of the differentiated ruling. The company's Hungary plant, operational since 2007 and recently expanded to approximately 18 million units of annual capacity, means that Chinese-origin tires account for only about 30% of its European sales—a substantially lower share than either rival. The 3.4% anti-dumping rate (total burden 7.9%) confirms that Hankook's decade-long localization strategy has insulated its European franchise from the penalty tier now applied to less-prepared competitors.

Kumho Tire (073240.KS) faces the sharpest near-term headwind. Approximately 50% of its European tire sales are manufactured in China, leaving a material revenue stream exposed to a 34.4% combined tariff. The company has indicated plans to raise Korean and Vietnamese production and complete a planned Poland plant by 2028, but the interim period—before European supply chain capacity is in place—will compress margins. Kumho has said it will file formal objections before the duties become permanent, though overturning definitive EU anti-dumping findings is rarely achieved in full.

Nexen Tire (002350.KS) occupies a middle position. Its Chinese production accounts for roughly 15% of European sales, a smaller footprint than Kumho but still subject to the same 29.9% rate. Nexen intends to maximize utilization at its Czech Republic plant and has separately announced plans for a fifth overseas manufacturing facility to diversify its supply base. The Czech operation's capacity constraints limit Nexen's short-term flexibility within Europe.

Investment Implications

The duties crystallize a structural divergence in competitive positioning that investors should price into sector weightings:

- Hankook (161390.KS): Clear relative winner. Hungary plant capacity and 7.9% effective rate position it to gain European market share as Chinese imports face steeper headwinds industry-wide.

- Kumho (073240.KS): Most exposed. With ~50% of EU volume from China and a 34.4% tariff, near-term margin compression is unavoidable. The Poland plant timeline (2028) creates a multi-year earnings overhang.

- Nexen (002350.KS): Moderate exposure. Smaller China reliance (15%) limits damage, but the same 29.9% rate applies; Czech plant maximization buys partial relief.

The broader read-across is that European revenue exposure—once a straightforward growth driver for Korean tire makers—now carries a bifurcated risk profile depending on where tires are actually built. Companies that delayed investing in European or Southeast Asian capacity will carry higher tariff costs for at least two to three years as restructuring unfolds.

Sources: KED Global · Seoul Economic Daily – Tariff Rates · Seoul Economic Daily – Nexen Fifth Plant · AJU Press