China's CXMT filed for a CNY 29.5 billion ($4.1 billion) initial public offering on Shanghai's STAR Market — and buried in the 800-page prospectus is a data point that matters more to investors in Seoul than in Shanghai: there is no high-bandwidth memory investment plan.

What the Filing Says

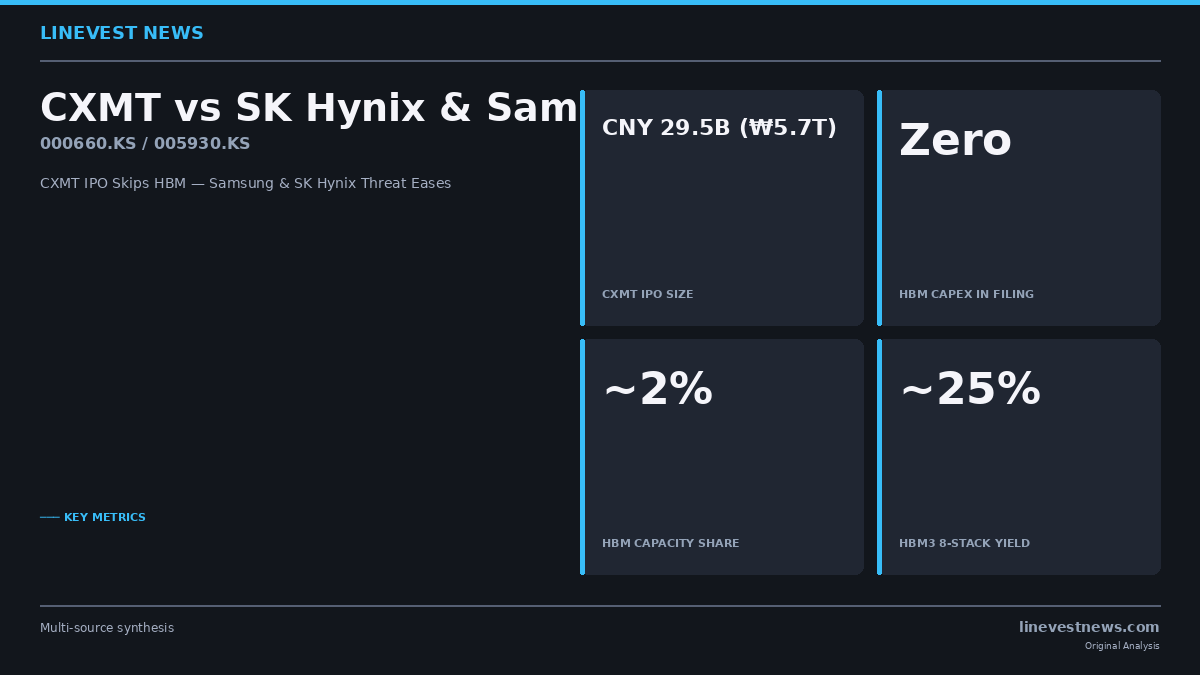

Changxin Memory Technologies (CXMT), China's largest DRAM manufacturer, submitted its prospectus to the Shanghai Stock Exchange in early July 2026. The entire CNY 29.5 billion proceeds — equivalent to roughly KRW 5.7 trillion — are earmarked for two purposes: upgrading existing commodity DRAM production lines and funding next-generation DRAM research and development. HBM does not appear as a separate capex category anywhere in the document.

The finding was first flagged by SemiAnalysis, a semiconductor research firm, which reviewed the filing's Chinese-language text line by line. "There is no HBM equipment investment project, and no mention of HBM whatsoever," SemiAnalysis noted in its report. "The core of this IPO is reinforcing conventional DRAM manufacturing and technology — there is no near-term commitment to HBM capacity expansion."

CXMT's customer list, disclosed in the filing, reinforces this picture. Its five largest clients — Alibaba Cloud, Tencent, ByteDance, Lenovo, and Xiaomi — are all buyers of standard DDR5 and LPDDR5 modules for servers, laptops, and mobile devices. No AI accelerator maker or HBM customer is listed. In 2025, roughly 99% of CXMT's revenue was derived from commodity DRAM.

Part A: Where CXMT Stands on HBM

CXMT is not standing still on HBM. It assembled a small-scale HBM packaging line in late 2025 and reportedly supplied test samples of an eight-layer HBM3 stack to Huawei. But scale and yield remain formidable obstacles.

SemiAnalysis estimates that CXMT's HBM-designated capacity stood at approximately 5,000 wafers per month at end-2025, out of a total installed base of roughly 265,000 wafers per month — a share of under 2%. That figure is projected to rise to 30,000 wafers per month by end-2026 and 55,000 wafers per month by end-2027 under a base-case scenario. However, those projections reflect organic ramp plans, not the stepped-up investment that a dedicated HBM capex line in the IPO filing would have signaled.

Yield is the more pressing issue. Industry sources cited in the SemiAnalysis report estimate that CXMT's HBM3 eight-stack product is achieving a composite yield of roughly 25%. For comparison, SK Hynix, the global market leader in HBM, targets and largely achieves yields above 60% on its HBM3E production runs. At 25% yield, CXMT's cost per usable die would be prohibitive for any customer outside China's domestically subsidized AI supply chain.

Technical constraints compound the challenge. Through-silicon via (TSV) stacking — the core process that interconnects DRAM dies in an HBM stack — requires advanced equipment subject to U.S. export controls. CXMT appears on the U.S. Department of Defense and Department of Commerce restricted-entity lists, meaning it cannot legally import leading-edge lithography and TSV bonding tools from Western suppliers. Making HBM investment plans explicit in an IPO filing could also invite additional regulatory scrutiny, which may partly explain their absence.

Part B: What This Means for Samsung and SK Hynix

For Korean memory investors, CXMT's filing removes — or at least defers — the most alarming scenario: a sudden, capital-intensive Chinese push into the HBM market funded by a massive equity raise.

SK Hynix (000660.KS) holds an estimated 70%-plus share of the global HBM market by revenue and is the primary supplier of HBM3E to Nvidia for its H200 and next-generation Blackwell GPU platforms. The company's Q2 2026 preliminary results, released last week, showed the extent to which HBM has reshaped its earnings profile: operating profit reached KRW 430 billion on a standalone basis, recovering from the prior quarter's EV-related weakness at its battery-adjacent customer base. HBM average selling prices remain a multiple of equivalent-density commodity DRAM.

Samsung Electronics (005930.KS) reported an industry-record Q2 2026 operating profit of KRW 89.4 trillion, driven in large part by HBM3 ramp and AI memory demand from hyperscaler customers. Its foundry division is separately recovering. Both companies have flagged CXMT's HBM ambitions as a medium-term risk in recent IR materials — the muted capex picture from the IPO filing provides a degree of near-term relief.

The relief, however, is conditional. Several risk factors remain:

State Funding Bypass: CXMT's IPO proceeds represent one channel of financing. China's national semiconductor fund (Big Fund III, totaling approximately CNY 300 billion) and provincial government vehicles in Hefei — where CXMT's fabs are located — could theoretically fund a parallel HBM expansion that never appears in public equity filings. Industry observers note that HBM investment could be kept off-balance-sheet precisely to avoid triggering additional U.S. sanctions.

Longer Horizon Risk: One senior industry executive quoted by Chosun Biz cautioned that "CXMT's HBM capacity could grow more than tenfold from current levels by 2027 or 2028." If that trajectory materializes, pricing pressure in the HBM market would intensify regardless of what the current IPO filing shows.

Commodity DRAM Cannibalization: Even if CXMT never cracks HBM, its CNY 29.5 billion investment in commodity DRAM capacity — DDR5, LPDDR5, and GDDR6 — will add roughly 30,000 to 50,000 wafers per month to global supply over the next 18 months. That puts downward pressure on the lower-margin portion of Samsung's and SK Hynix's revenue mix.

The Investment Case

The net read for Korean memory investors is cautiously positive in the near term. CXMT's decision — or inability — to commit IPO capital to HBM preserves the existing oligopoly structure: SK Hynix, Samsung, and Micron hold all commercially viable HBM capacity for the foreseeable future. The pricing umbrella over HBM3E and the emerging HBM4 generation remains intact.

The medium-term picture is murkier. Investors would be wise to monitor the Big Fund III disbursement schedule and any disclosure updates CXMT files in the months following its Shanghai debut — projected for Q3 2026. The absence of HBM in this prospectus is reassuring, but it is a snapshot, not a guarantee.

Sources: Chosun Biz · SemiAnalysis (via Chosun Biz)