Samsung Posts Largest Quarterly Profit in History—Then Falls 10%

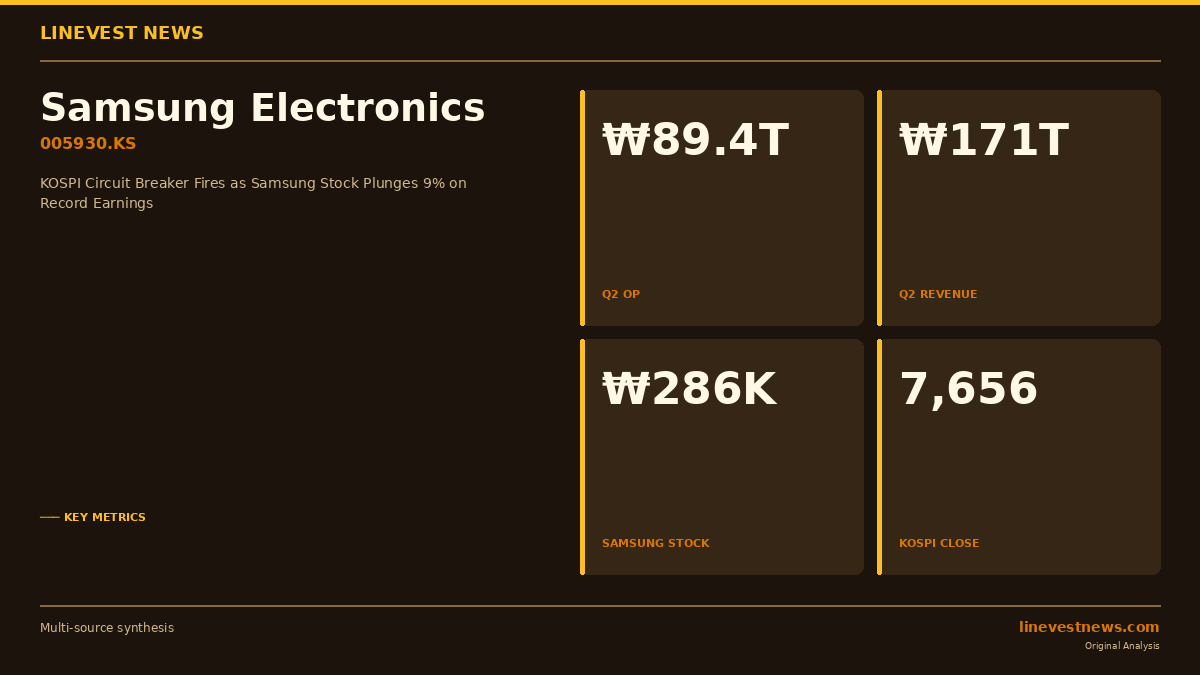

Samsung Electronics on Tuesday reported second-quarter 2026 operating profit of ₩89.4 trillion (approx. USD 58.4 billion), a 1,810.3% surge year-over-year and a 56.2% jump from Q1. Revenue came in at ₩171 trillion, up 129.3% from a year earlier. The results, driven almost entirely by the AI-memory boom, eclipsed Nvidia's previous record quarterly profit of roughly USD 53.5 billion and Apple's peak of approximately USD 50.9 billion—a first for a Korean company against global tech titans.

Yet the stock fell.

What the Numbers Show — Part A

Samsung's headline beat centered on its semiconductor arm. Meritz Securities analyst Kim Sun-woo said the memory segment outperformed consensus estimates by approximately ₩900 billion, crediting Samsung's pricing leadership across both DRAM and NAND as AI-infrastructure spending continued to accelerate into mid-year.

The numbers by segment break down as follows, based on preliminary disclosures and analyst estimates:

| Segment | Q2 2026 (est.) | Margin (est.) |

|---|---|---|

| Semiconductor (DS) | ~₩85–86T revenue | High teens % |

| Device eXperience (DX) — MX, VD/DA | ~₩14–15T revenue | Near-zero to negative |

The DX division—Samsung's mobile, TV, and home-appliance businesses—tells a different story. Kiwoom Securities estimated VD/DA operating profit at ₩142 billion (~1% margin); Hyundai Motor Securities placed it at ₩58 billion (0.4% margin); Meritz flagged a potential operating loss in the segment. The paradox: Samsung's own memory chips are now an input cost for its set businesses. As DRAM prices rise, the TV and appliance units absorb the cost increase without comparable pricing power in consumer markets.

The Market's Verdict — Part B

Circuit Breaker, Sixth of 2026

Despite—or because of—the record headline, KOSPI triggered a market-wide circuit breaker at session open, its sixth halt of the year. Korea Exchange also activated a sell-side sidecar, suspending program trading temporarily. By close, KOSPI had recovered from an intraday low of -8.2% to finish at 7,656.31, down 4.91% on the day.

Samsung Electronics shares closed at approximately ₩286,000–288,000, a decline of roughly 9–10% from the prior session—breaching the closely-watched "30만전자" (₩300,000) floor that had held since mid-May 2026. From its all-time high of ₩380,000 reached in mid-June, the stock is now down approximately 24% in under three weeks.

SK Hynix fell 6.06%, dragging broader semiconductor indices lower alongside peer memory names globally.

Why Did the Market Sell?

Three forces converged:

"Sell the news" dynamics: Samsung's outperformance had been widely anticipated since the Q1 beat and AI pricing commentary. Investors who positioned ahead of the print chose Tuesday as the exit window.

Peak-earnings anxiety: A report attributed to Morgan Stanley—circulated under the headline "Is this the peak?"—flagged risks of a memory price correction in Q3–Q4 2026 as cloud hyperscaler capex enters a seasonal digestion phase. The set-division weakness (near-zero VD/DA margins) reinforced fears that record consolidated profits mask an uneven underlying structure.

Technical and mechanical selling: Leverage ETF rebalancing following a sharp morning gap-down created a compounding loop. Foreign investors net-sold an estimated ₩3 trillion in Korean equities, with semiconductors absorbing the bulk. Hanwha Ocean's failure to secure a major new shipbuilding order added incremental pressure to the broader industrial complex.

KOSPI at 7,656: What It Means

Tuesday's close puts KOSPI approximately 19% below the historic high of roughly 9,400 touched in late May 2026, yet still 62% above year-start levels. The index has now experienced six circuit-breaker events in 2026, versus two in the entire prior year—a signal of elevated volatility as AI-semiconductor repricing works through the market.

For foreign holders, who collectively own roughly 32% of KOSPI market capitalization, the Samsung move is significant: the stock is the single largest weighting (~20%) in the index, meaning a 10% single-day drop mechanically clips ~200 KOSPI index points before any other names move.

Analyst Outlook

Meritz's Kim retained a positive view on Samsung's memory trajectory: "The memory segment outperformed our model by ₩900 billion—pricing leadership in DRAM remains intact." He and peers at Kiwoom noted that HBM (High Bandwidth Memory) order books for the second half remain robust, underpinned by Nvidia, Google, and Microsoft AI server builds.

The bear case, championed by Morgan and a handful of Korean sell-side shops, centers on two variables: (1) the pace of cloud capex after the current build cycle, and (2) whether Samsung's MX and DX divisions can restore positive margins into H2 2026 as memory input costs remain elevated.

Investor Takeaways

For KOSPI-exposed international investors, Tuesday's session surfaces a structural tension inside Samsung's own income statement: the same memory-price supercycle that inflates consolidated profits also compresses the margins of every Samsung business that uses memory chips. Until the set divisions demonstrate independent pricing power—likely requiring new AI-enhanced product lines at premium price points—the DX drag will cap how the market values the consolidated entity. The AI memory wave lifts Samsung's semiconductor arm; it also burdens every other division at the same time.

Sources: Korea Times · Hankyung · Investing.com · etnews · ts2.tech