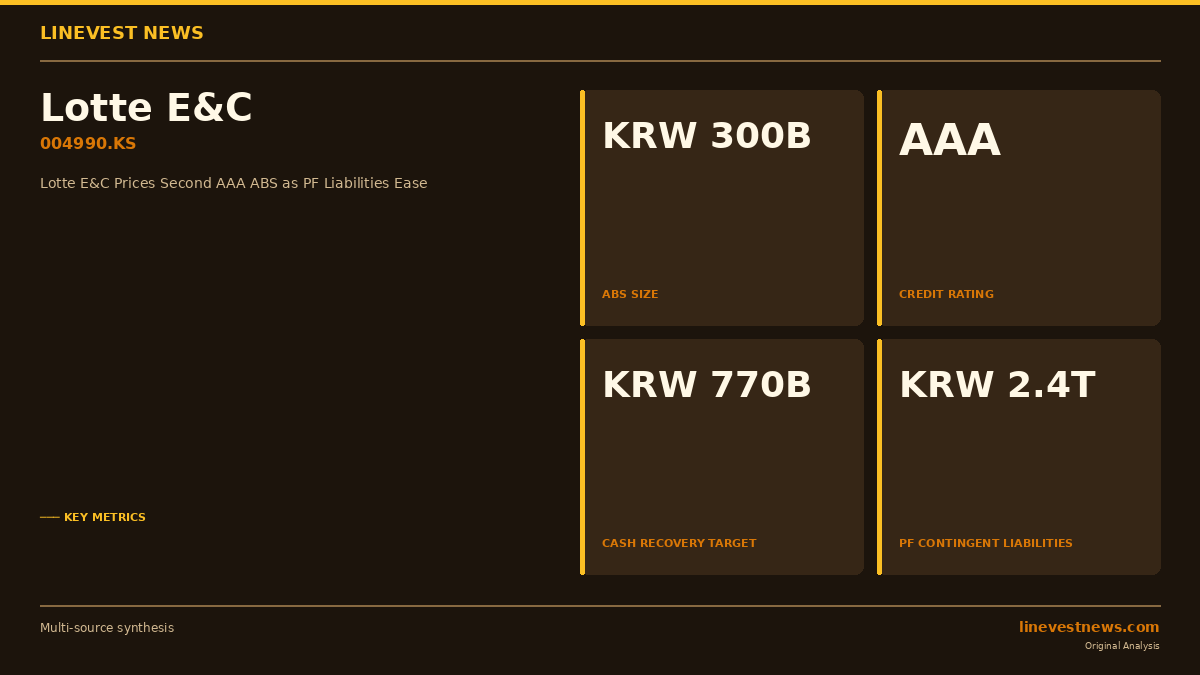

Lotte Engineering & Construction (Lotte E&C) on July 7 priced its second round of asset-backed securities (ABS) totaling KRW 300 billion (approx. USD 216 million), drawing five major Korean financial institutions to underwrite paper that earned a top AAA credit rating — three notches above Lotte E&C's own A0 corporate standing.

What Was Announced

The offering was split evenly: KRW 150 billion with a one-year maturity and KRW 150 billion due in 15 months. Underwriters included KB Securities, Hana Securities, Kiwoom Securities, Samsung Securities, and Korea Investment & Securities.

The collateral pool consists of construction-payment receivables drawn from two categories of project sites: residential housing developments nearing completion, and construction work performed at Lotte Group-affiliated companies' campuses. The deal follows a first ABS issuance in May 2026, which used the same structural template but limited collateral to housing-only receivables. For this second tranche, Lotte E&C expanded the collateral to include group-affiliate construction sites and layered in additional bank credit facilities to achieve the higher AAA threshold — enabling it to borrow at rates well below its A0-implied cost.

Korean Market and Investment Analysis

The back-to-back ABS issuances mark a meaningful rehabilitation in market confidence for Lotte E&C, a builder that was among Korea's most exposed to the 2023–2024 real estate project-financing (PF) liquidity crisis.

Working-Capital Transformation

In normal construction operations, a contractor fronts costs months before collecting payment — the cash cycle typically stretches two to six months after spending. By securitising payment receivables through ABS, Lotte E&C can collect immediately upon spending, effectively eliminating that working-capital drag. The company estimates the two-round ABS program will pull forward KRW 770 billion (approx. USD 556 million) in cash recovery by Q1 2027.

PF Contingent-Liability Trajectory

Project-financing contingent liabilities — the metric Korean investors have used to gauge builders' balance-sheet risk since 2023 — stood at approximately KRW 2.4 trillion at the end of June. Three Homeplus-linked PF projects (Gwangju Ssangnyeong Park, Bucheon Sangdong, and Dongdaemun) converted from bridge financing to main PF status during the quarter, reducing the overhang. Lotte E&C targets a further reduction to KRW 2.2 trillion by year-end.

Earnings Recovery

First-quarter 2026 operating profit came in at KRW 50.4 billion (approx. USD 36 million), a significant improvement year-on-year, though the company has not yet fully restored pre-crisis profitability margins. The back-to-back AAA pricing suggests underwriters are comfortable with that recovery trajectory.

Implications for Listed Lotte-Group Investors

Lotte E&C is an unlisted subsidiary of Lotte Holdings (004990.KS). For investors tracking Lotte Holdings or Korea's construction and real estate sector, the ABS program signals that the market's appetite for Lotte E&C paper — once priced as high-risk — has normalised. A stable funding pipeline reduces the risk of group-level contagion that spooked equity investors in 2023.

Korea's listed construction peers — including GS Engineering & Construction (006360.KS) and DL E&C (375500.KS) — have also been working through PF exposure. Lotte E&C's successful AAA ABS issuance may encourage similar off-balance-sheet funding structures across the sector, potentially easing the liquidity premium that has weighed on Korean builder valuations.

Sources: Newsis · Yonhap (Yonhap News Agency)