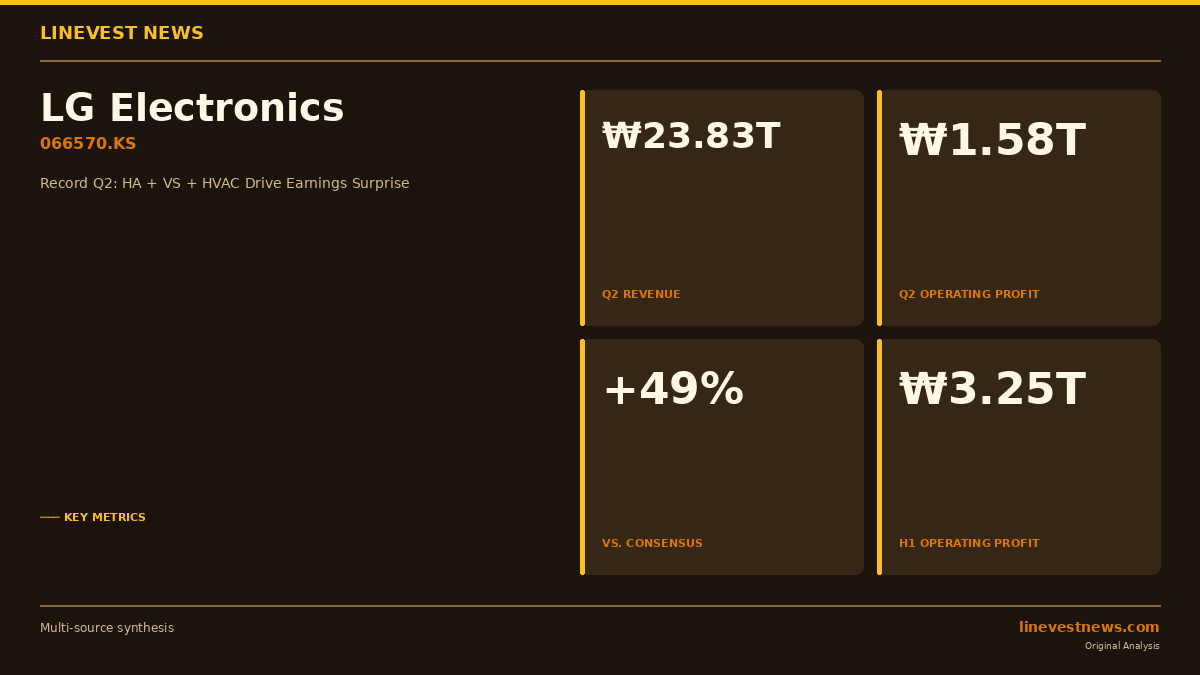

LG Electronics (066570.KS) reported its best-ever second-quarter results on Tuesday, posting operating profit of KRW 1.58 trillion (approximately USD 1.15 billion), a surge of 146.9% year-on-year that exceeded analyst consensus of KRW 1.06 trillion by roughly 49%. Revenue came in at KRW 23.83 trillion, up 14.9% from a year earlier and ahead of the KRW 22.54 trillion forecast.

The first-half performance was equally striking: cumulative H1 sales reached KRW 47.56 trillion — a new record — while H1 operating profit hit KRW 3.25 trillion, already surpassing the KRW 2.48 trillion LG Electronics recorded for the entirety of fiscal 2025.

Part A — What Was Announced

LG Electronics released its preliminary Q2 2026 results on July 8, with detailed segment data and net profit scheduled for disclosure at the full earnings conference later in July.

Headline figures (Q2 2026 vs Q2 2025): | Metric | Q2 2026 | YoY Change | |--------|---------|-----------| | Revenue | KRW 23.83T (≈ USD 17.3B) | +14.9% | | Operating Profit | KRW 1.58T (≈ USD 1.15B) | +146.9% | | OP Margin | ~6.6% | +3.9 pp | | H1 Revenue | KRW 47.56T | Record | | H1 Operating Profit | KRW 3.25T | Record (>FY2025 full year) |

The company attributed the outperformance to four overlapping drivers. First, Home Appliance & Air Solution (HAS) continued its expansion across both premium and mass-market segments, with B2B built-in appliances and commercial laundry accelerating at higher margins. Second, Vehicle Solution (VS) — LG Electronics' automotive infotainment, electric vehicle components, and Magna-partnership business — booked a solid order backlog and is becoming, in management's description, an "emerging cash-generation area."

Third, Eco Solution benefited from record-level summer heat in Europe that drove heat pump demand sharply higher, especially in Germany, France, and the United Kingdom. Fourth, the Media Entertainment segment improved from the year-earlier period on the back of new premium OLED evo and Micro RGB television lines.

The company also recorded a non-recurring boost from a U.S. tariff refund on prior-year duties paid, though the exact magnitude will be detailed at the full earnings call.

Part B — Korea Market Implications

A Diversification Story at the Right Time

LG Electronics' blowout quarter arrives on the same day that Samsung Electronics' record KRW 89.4 trillion Q2 operating profit triggered a sell-the-news rout on KOSPI — the benchmark's sixth circuit breaker of 2026. The contrast is instructive. While Samsung and SK Hynix are priced almost entirely to an AI memory super-cycle narrative, LG Electronics derives its profits from a different, and in many ways more durable, set of demand drivers: global HVAC replacement cycles, EV content-per-vehicle expansion, and premium appliance premiumisation.

For foreign investors monitoring Korea exposure, LG Electronics represents a lower-volatility path to Korean industrial prowess — one not directly tethered to memory pricing or US semiconductor-export policy risk.

Vehicle Solution: The Long-Dated Option

The VS division's trajectory deserves particular attention. LG Electronics supplies infotainment systems and EV powertrain components to General Motors, Stellantis, Volkswagen, and Hyundai Motor Group. As major automakers finalize multi-year software-defined vehicle (SDV) programmes, LG's backlog visibility extends well into 2028. A full-scale SDV platform typically embeds two to three times more LG content per vehicle than a conventional model. With VS now reliably profitable and the order backlog deepening, analysts at major Korean brokerages have flagged the division as a potential re-rating catalyst for the parent stock.

European Heat Pump Tailwind

Southern and Central Europe's record summer temperatures — which drove emergency AC purchases across the region — also pulled forward heat pump replacements under EU Fit for 55 subsidy programmes. LG's Eco Solution division, which supplies heat pumps, solar inverters, and energy storage systems to residential and commercial customers in Europe, is a direct beneficiary. The structural tailwind from EU building decarbonisation mandates is expected to keep European heat pump demand elevated through at least 2028, providing LG with predictable B2B revenue independent of consumer sentiment.

What Investors Are Watching Next

Key questions for the full earnings call later in July:

- Tariff refund magnitude — how much of the OP beat was one-time? Stripping out the refund will clarify underlying margin momentum.

- VS divisional margin — if VS operating margin crossed 5%, it would signal a structural inflection; below 3% would indicate continued drag from EV model ramp costs.

- H2 guidance — LG Electronics rarely gives formal guidance, but commentary on appliance ASP trends and European heat pump order flow will be closely watched.

- Dividend / shareholder return — with H1 OP already above full-year 2025, investors may begin to price in a higher annual dividend or a renewed buyback authorization.

LG Electronics shares closed at KRW 156,200 on July 7, having lagged the broader KOSPI recovery in H1 2026. The record Q2 print, if sustained at the full earnings call, may narrow the gap with peers whose premium is built on near-term AI memory pricing.

Sources: Korea Herald · Korea Herald Business