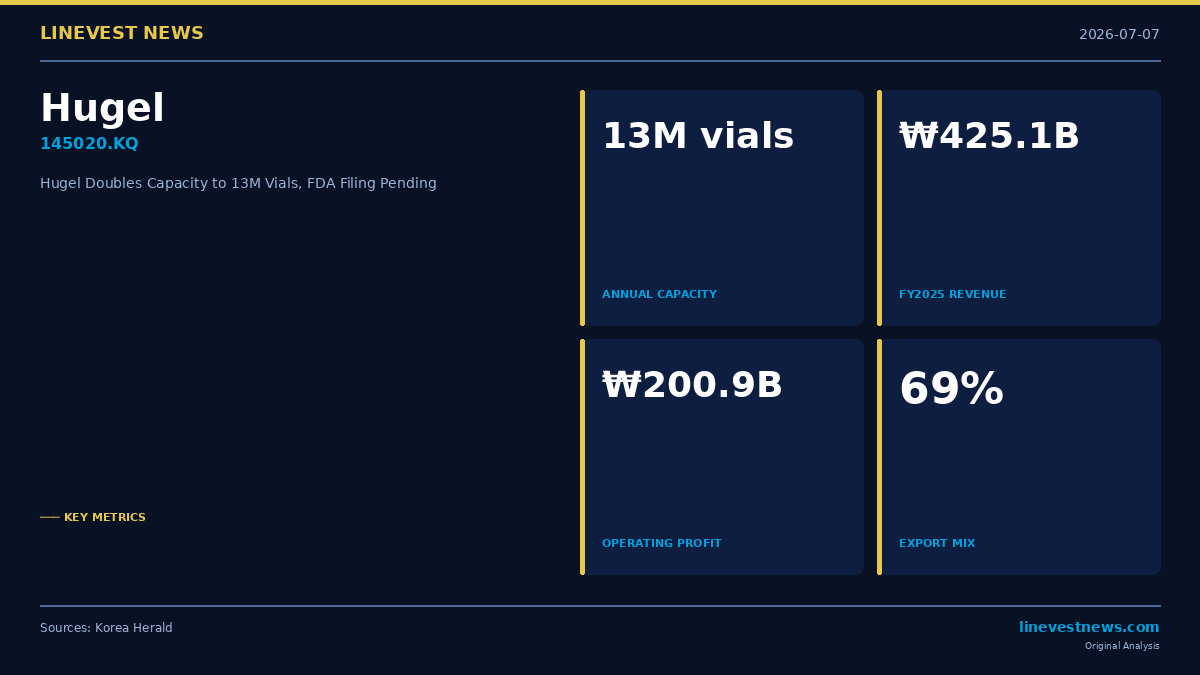

South Korea's Hugel (145020.KQ), one of the world's largest botulinum toxin manufacturers, has doubled its annual production capacity to 13 million vials following the commissioning of Building B at its Geodu factory in Chuncheon, Gangwon Province — and is now seeking US Food and Drug Administration clearance for the new facility to accelerate its Letybo commercial ramp in North America.

What Happened

Building A, Hugel's original toxin plant, produces 5 million vials per year. Building B — which came online in April 2025 — adds 8 million vials of annual output and is meaningfully more efficient: managing director Seol Hee-soo told reporters that it delivers "roughly 1.6 times the output of Building A" with "40 percent faster finished-product manufacturing time."

The production process is tightly controlled. A single master tube of toxin — roughly thumb-sized — yields more than 25,000 clinical vials in a four-hour filling run, followed by a 16-hour freeze-dry cycle. Only 18 certified employees hold biometric clearance to the toxin suite, which requires both fingerprint and iris recognition. The master toxin is stored at −80°C.

Hugel has filed a Prior Approval Supplement with the US FDA to formally register Building B. Sequential regulatory submissions in Europe, China, and other markets are planned beginning in 2026. The company is also validating a vacuum-drying process aimed at additional regulatory submission later this year.

Korea Market Context

The expansion underscores how Korean botulinum toxin producers have seized global market share — particularly in the aesthetic medicine segment — that western peers have been slow to contest.

Hugel's commercial product is sold as Botulax in South Korea and most international markets; the US brand name is Letybo, distributed via a partnership with French pharmaceutical company Ipsen. The FDA-approved Letybo launched in the United States in 2023 and is still in its early commercial ramp against the dominant Botox franchise owned by AbbVie (NYSE: ABBV).

Key metrics from FY2025:

| Metric | Value |

|---|---|

| Revenue | KRW 425.1B (USD 279M) |

| Operating Profit | KRW 200.9B |

| Operating Margin | ~47.3% |

| 5-Year Revenue CAGR | 16.4% |

| Export Mix (toxin) | ~69% |

| Markets Served | 70+ countries |

| Annual Production | 13M vials |

| Global Rank | 5th largest (Pristine Market Insights) |

The near-50% operating margin is notably high for a pharmaceutical manufacturer and reflects the low raw-material cost structure of botulinum toxin: the active substance is produced via bacterial fermentation and freeze-dried, with the scale economics of Building B expected to lower incremental unit cost further as utilization rises.

Investment Angle

FDA clearance as binary catalyst. Hugel's most immediate share-price driver is the pending FDA registration of Building B. Clearance would allow the company to scale US-licensed supply roughly 1.6-fold — removing a bottleneck that could otherwise limit Letybo revenue growth as the product gains physician adoption. Delays would push back the US revenue curve.

US market premium. The United States is the world's largest single-country aesthetics market, and reimbursement dynamics favour branded products. Letybo's approval positions Hugel to capture margin-accretive US sales that, at scale, would shift the revenue mix toward higher-value geographies.

Diversified regulatory approval base. With approvals already in the US, EU, and China — the three largest regulatory jurisdictions — Hugel faces lower portfolio risk than single-market biotech peers. The 70-country footprint also provides demand diversification against regional economic downturns.

Key risks: FDA Building B approval timeline uncertainty; Botox entrenched physician loyalty; consumer discretionary sensitivity in an economic slowdown; manufacturing quality incidents could trigger supply halts; pricing pressure from Chinese domestic competitors in Asia.

Hugel's PE owner, Bain Capital, has held the stake since 2020 and refinanced KRW 765B in debt in June 2026 rather than exiting — a signal of confidence in continued earnings growth. Any eventual IPO re-listing or secondary sale would represent an additional liquidity event for market participants.

Sources: Korea Herald