Korea's financial regulators published draft guidelines on July 6 that would fundamentally reshape how listed conglomerates spin off subsidiaries onto public markets — a long-awaited move aimed at squeezing out the structural discount that has made Korean equities persistently cheap relative to global peers.

The Financial Services Commission and the Korea Exchange jointly released the framework, which adopts a "principally ban, exception allowed" approach. Under the new rules, any listed parent company pursuing a separate public listing of a subsidiary must clear a five-step governance hurdle before the exchange will accept the application.

Part A — What the New Rules Require

Five mandatory obligations apply to parent company boards:

- Impact assessment — quantify expected share-price dilution or corporate value discount for the parent

- Investor protection measures — design concrete remedies such as cash dividends, in-kind distribution of subsidiary shares, or buyback programs

- Shareholder communication or approval — engage investors or formally seek their consent, depending on the subsidiary's size

- Board vote — directors must formally resolve to proceed with the listing

- Public disclosure — the full process, including protection commitments, must be publicly filed

An independent special committee of at least three members must complete a pre-board review before any listing proposal moves forward.

Spin-off subsidiaries face the toughest test. Where a subsidiary is created specifically for listing purposes, shareholder approval follows the Commercial Act's "3 percent rule": the controlling shareholder's voting rights are capped at 3 percent of total shares, and the resolution requires both a majority of votes cast and the support of at least one-quarter of all eligible shares. In practice, this gives minority investors an effective veto.

Small subsidiaries are exempt if their sales, operating profit, and total assets each represent less than 10 percent of the parent's consolidated figures — provided the board fully complies with the five obligations.

Overseas listings are not exempt. Parent companies seeking to list subsidiaries on Nasdaq, the New York Stock Exchange, or other foreign exchanges must follow the same disclosure and governance procedures, with an additional review by the Financial Supervisory Service.

Penalties for non-compliance: fines of up to KRW 1 billion (approximately USD 652,000) and a one-day trading suspension.

The guidelines are open for public comment; a final implementation date has not been announced.

Part B — Korea Discount in Focus: What Investors Need to Know

The Scale of the Problem

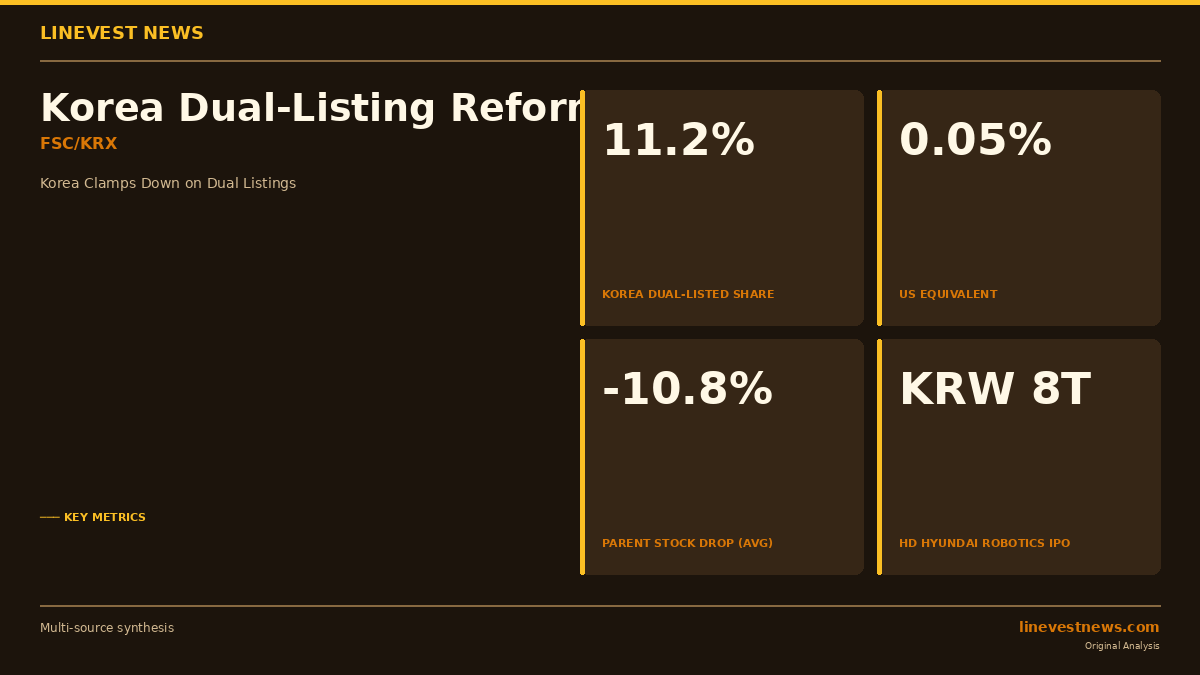

Korea's dual-listing structure is an outlier by international standards. Listed subsidiaries accounted for 11.2 percent of total KOSPI market capitalization at end-2025, versus 0.05 percent in the United States, 4.0 percent in Japan, 2.4 percent in China, and 2.7 percent in Taiwan.

The consequences for parent-company shareholders have been measurable. An analysis of 261 dual listings between 2000 and 2024 found that parent companies' stock prices fell an average of 10.81 percent within six months of a subsidiary's IPO. The mechanism is straightforward: a successful subsidiary listing crystallizes value in a vehicle that minority shareholders of the parent cannot fully access, while the parent continues to bear capital-allocation risk and strategic complexity.

This pattern has contributed to the "Korea discount" — the tendency of KOSPI-listed groups to trade at a significant markdown to their sum-of-parts value. For foreign investors, who held approximately 32 percent of KOSPI market capitalization in mid-2026, the new rules represent a direct response to one of their most persistent complaints about Korean equity markets.

Companies in the Crosshairs

Several high-profile subsidiary listings are already in motion or being planned:

HD Hyundai Robotics — Hyundai Motor Group's industrial-robotics arm is targeting a market valuation of approximately KRW 8 trillion (USD 5.5 billion) in a planned KOSPI listing. Its parent, HD Hyundai (329180.KS), would face shareholder approval requirements under the new framework. HD Hyundai's current market cap is approximately KRW 5.7 trillion, making an KRW 8T subsidiary valuation material under any governance test.

Boston Dynamics — The U.S. humanoid-robotics firm is majority-owned by Hyundai Motor (005380.KS), which completed its acquisition in 2021. Any future listing of Boston Dynamics — a scenario Hyundai has not ruled out — would require FSS review as an overseas listing under the new rules.

Kakao Mobility — Korea's dominant ride-hailing and mobility platform is a subsidiary of Kakao Corp (035720.KS). Kakao Mobility had previously filed for a KOSPI listing before withdrawing. A relisting would now require Kakao Corp's minority shareholders to formally weigh in.

CJ Olive Young — The health-and-beauty retail chain is a subsidiary of CJ Corp (001040.KS) and one of Korea's highest-profile e-commerce plays. Any public listing would trigger the full five-obligation process.

Investor Protection Mechanisms

Beyond blocking value-destructive listings, the rules create new levers for minority shareholders. Parent companies must proactively propose remedies — share buybacks, dividends, or in-kind distributions of subsidiary stock — as conditions for exchange approval. This shifts negotiating power toward retail and institutional investors in the parent and could incentivize more aggressive capital returns.

The framework also signals a broader regulatory direction: Korea is borrowing elements of the U.S. "materiality" and Japan's "two-thirds vote" approaches while adapting them to the chaebol-dominated ownership structure that underpins KOSPI's corporate landscape.

Market Outlook

Analysts and corporate governance advocates have long argued that a clear set of dual-listing rules would improve price discovery and raise the valuation floor for Korean holding companies and conglomerates. If enforced consistently, the new framework could narrow the discount that groups like LG Corp (003550.KS), SK Holdings (034730.KS), and Hanwha (000880.KS) trade relative to their asset values.

For investors in KOSPI conglomerates, the immediate implication is more predictability around subsidiary IPO plans — and a higher bar for value-dilutive transactions. Whether the rules will be applied retroactively to listings already in progress remains to be clarified in the final regulatory text.

Sources: The Korea Herald · Korea JoongAng Daily · BigGo Finance · Financial Services Commission