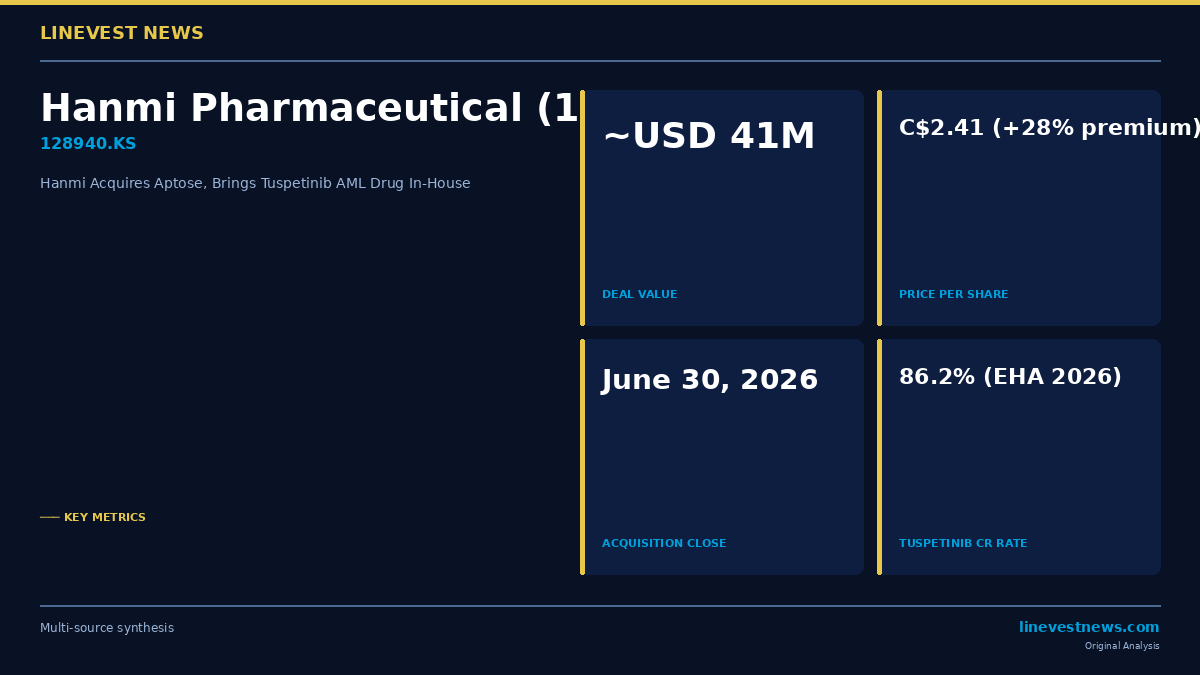

Hanmi Pharmaceutical Co., Ltd. (128940.KS) has completed the acquisition of Aptose Biosciences Inc., a Canadian clinical-stage oncology company, bringing its wholly in-licensed tuspetinib AML program back under direct control. The transaction closed on June 30, 2026, with Aptose shares delisted from the Toronto Stock Exchange (TSX: APS) on July 3.

Part A — Transaction Overview

Hanmi, through its wholly owned subsidiary HS North America Ltd., acquired all outstanding Aptose common shares not already held by the Hanmi group at C$2.41 per share — a 28% premium over Aptose's 30-day volume-weighted average price of C$1.88 on the TSX. The aggregate consideration approximates USD 41 million (KRW ~56.5 billion at current rates).

The deal had a lengthy runway. Hanmi first announced it on November 19, 2025, received Aptose shareholder approval and Ontario Superior Court sanction on March 31, 2026, and cleared Korean regulatory requirements before the June 30 close.

Why did Aptose become a takeout target? The Vancouver-based biotech, founded in 1991, entered technical insolvency by late 2025 as the broader clinical-stage biotech downturn crimped its access to capital markets. Much of Hanmi's acquisition funding — approximately KRW 56.8 billion — was already embedded in existing loans extended to Aptose, which were converted as part of the arrangement. The out-of-pocket net cost is therefore substantially below the headline figure.

Part B — The Tuspetinib Angle: Reversing a Licensing Decision

The strategic heart of the deal is tuspetinib (TUS; internally coded HM43239), an oral multi-kinase inhibitor targeting SYK, FLT3, JAK2, and other drivers of myeloid malignancy. Hanmi originally out-licensed tuspetinib to Aptose in 2021 under a deal worth up to USD 420 million (KRW ~580 billion) in milestone payments and royalties — one of the larger Korea-to-Canada pharma transactions of that year.

The logic at the time was conventional: Hanmi would collect upfront fees while Aptose, with its specialist oncology focus and North American clinical networks, would advance the drug through expensive Phase I/II trials. That calculus shifted when Aptose's balance sheet deteriorated. Rather than watch tuspetinib languish in a cash-strapped partner's pipeline, Hanmi chose to repatriate the asset.

TUSCANY Trial — Phase I/II Efficacy Signal

Aptose's flagship tuspetinib program is the TUSCANY Phase I/II trial, studying the drug as a frontline triplet combination — tuspetinib + venetoclax + azacitidine (TUS + VEN + AZA) — in patients with newly diagnosed AML who are ineligible for conventional induction chemotherapy. This patient segment, typically older or with significant comorbidities, has historically poor outcomes.

Data presented at the European Hematology Association (EHA) Congress in June 2026 showed a composite complete response (CRc) rate of 86.2% across 29 evaluable patients at the 40 mg, 80 mg, 120 mg, and 160 mg dose levels. Notably, 86.4% of CR/CRh responders achieved MRD-negativity — a marker associated with deeper and potentially more durable remission.

These figures compare favorably with the ~70-76% CRc rates historically reported for venetoclax-azacitidine doublet therapy in a similar population, suggesting tuspetinib may add meaningful efficacy as a triplet addition. However, the TUSCANY cohort remains small, and randomized Phase III data will be required before any definitive efficacy conclusions can be drawn.

Investment Implications for Hanmi (128940.KS)

Hanmi's acquisition of Aptose should be read primarily as a pipeline consolidation and North American R&D infrastructure move, not a near-term revenue event.

Bull case. If tuspetinib advances to Phase III with a clean safety profile and the 86.2% CRc rate holds in a larger cohort, the drug could command peak annual revenues of USD 500 million to USD 1 billion in the AML market, which is currently projected to exceed USD 4 billion globally by the early 2030s. Hanmi would retain 100% economics rather than sharing milestones and royalties with an external partner.

Bear case. Phase I/II oncology response rates frequently do not replicate in randomized settings. Venetoclax-azacitidine already represents standard-of-care in this AML segment; demonstrating statistically significant incremental benefit for tuspetinib in a Phase III will require a large, expensive trial that now sits entirely on Hanmi's balance sheet. Hanmi's annual R&D expenditure runs approximately KRW 400-500 billion — absorbing full tuspetinib development costs will test that budget.

North American foothold. HS North America Ltd.'s role as the acquisition vehicle signals that Hanmi intends to keep an operational presence in Canada and the United States. This mirrors the offshore R&D hub strategy adopted by Yuhan Corporation and other Korean pharma names in recent years.

Sector Context

Hanmi has pursued an aggressive out-licensing model over the past decade — efpeglenatide (GLP-1, partnered with Sanofi), rolontis (long-acting G-CSF, filed with FDA), and a portfolio of bispecific antibodies under active BD discussions. The Aptose deal adds an AML asset to a pipeline already weighted toward metabolic disease and autoimmune indications, providing meaningful indication diversification.

Korean pharma investors will watch three milestones: (1) Hanmi's disclosure of a Phase III design and timeline for tuspetinib, expected within 12-18 months; (2) whether Hanmi files a U.S. IND amendment under its own name or maintains Aptose's existing IND; and (3) updated safety data from TUSCANY at the highest dose levels.

Sources: Aptose Biosciences Press Release · GlobeNewsWire · Allsci · Hankyung