Apple's entry into the foldable smartphone market this year is set to drive a 24% surge in global foldable panel shipments, with Samsung Display — a wholly owned subsidiary of Samsung Electronics (005930.KS) — positioned to capture premium supply contracts, according to a Counterpoint Research report published July 6.

Part A: Counterpoint Research Data

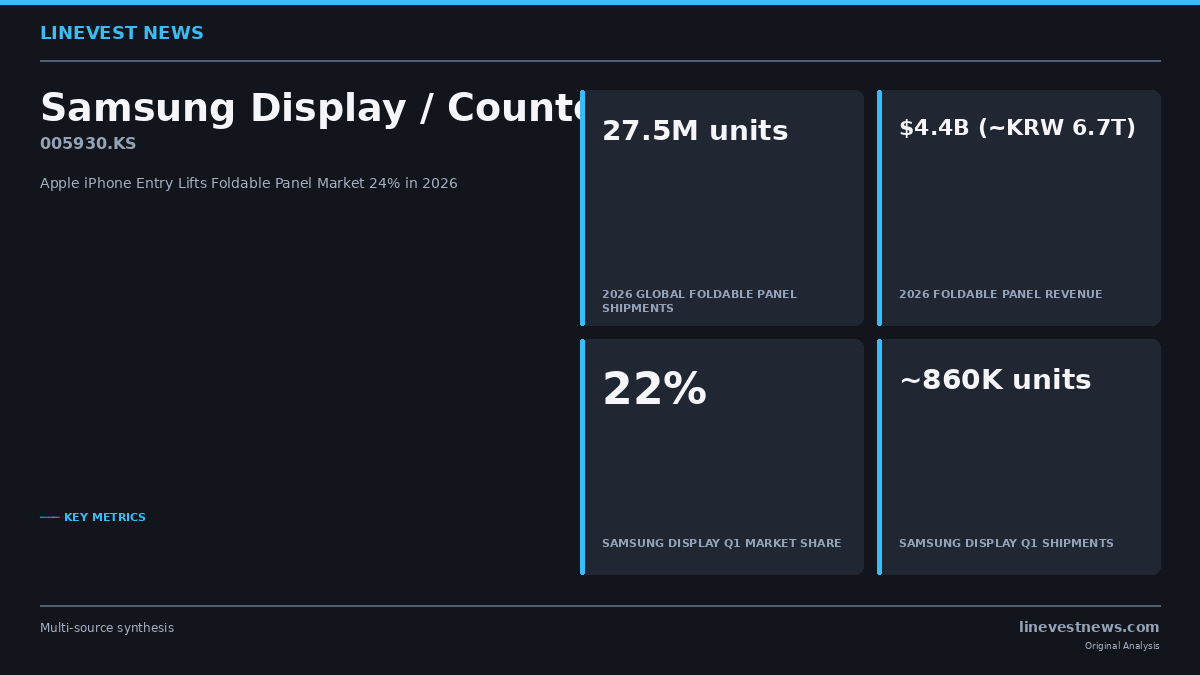

Global foldable smartphone panel shipments are forecast to reach approximately 27.5 million units in 2026 (+24% year-on-year), with market revenue expanding at a faster rate of 48% to roughly $4.4 billion (approximately KRW 6.7 trillion). The disparity between volume and revenue growth reflects Apple's entry into the premium in-fold segment, which is expected to elevate average selling prices and shift the product mix toward higher-margin configurations.

Counterpoint Research identified Apple as the single most important variable shaping the foldable panel market in the second half of 2026. The company is expected to begin commercial procurement for its first foldable iPhone panel in H2, with full-year handset share projected at approximately 29% — positioning Apple as the second-largest buyer behind Samsung Electronics' anticipated 31%.

The first quarter of 2026 recorded a transitional trough: panel shipments fell 7% year-on-year to approximately 3.9 million units as brands adjusted inventories ahead of the new product cycle. Counterpoint described the decline as cyclical rather than structural, noting that H2 is expected to account for approximately 64% of full-year shipments once Apple and Samsung launch new foldable devices simultaneously.

Part B: Korean Market Implications

Samsung Display gains ground ahead of the Apple ramp. In Q1 2026, Samsung Display expanded its market share from 15% to 22%, with shipments rising 37% year-on-year. Critically, the growth was driven not only by Samsung Electronics' internal foldable demand but also by new orders from Chinese brands OPPO and vivo — a diversification that reduces the unit's single-customer concentration risk. Counterpoint analysts projected that Samsung Display's competitive position will "further strengthen" in the second half as both Apple and Samsung Galaxy foldable launches ramp.

BOE's lead narrows. China's BOE Technology held Q1 leadership at approximately 45% share, down from 52% a year earlier, as its primary customer Huawei faces fresh constraints from US technology export controls. BOE's Q1 shipments declined 19% year-on-year. While the Chinese panel maker retains scale advantages in volume tiers, its concentration in the Huawei ecosystem represents a structural risk as premium in-fold growth — where Samsung Display and Apple's supply partnerships cluster — outpaces the broader market.

Dual-beneficiary dynamic for Samsung Electronics. As Samsung Display's parent, Samsung Electronics (005930.KS) stands to capture panel supply economics from Apple's foldable program at premium pricing — a revenue layer that adds to Samsung Galaxy's own foldable handset cycle. With Samsung Electronics' semiconductor division reporting Q2 results on July 7, investors monitoring the broader earnings profile should note that the display segment's Apple-driven H2 order ramp represents an underappreciated secondary catalyst.

Revenue-volume spread signals structural upgrade. Counterpoint's 48% revenue growth forecast outpacing 24% unit growth by 24 percentage points is an unusually wide spread. It reflects the shift in product mix toward wide book-style in-folds from clamshell formats, along with increasing average selling prices as Apple enters with premium-tier configurations. The trifold category — represented by Huawei's Mate XT and Samsung's Galaxy Z Trifold — remains a showcase segment: multi-hinge complexity, lower yields, and weight penalties are expected to limit it to headline launches rather than meaningful volume through 2026, Counterpoint concluded.

Key risks. Any delay to Apple's H2 foldable iPhone launch timeline would shift the H2 concentration back toward early 2027, compressing Samsung Display's revenue outlook for the current fiscal year. A broader macro-driven pullback in premium consumer spending could also dampen adoption velocity, particularly in the KRW 1.5 million–2.5 million (approximately $1,100–$1,800) price bracket where most foldable flagship devices are positioned.

Sources: Counterpoint Research Quarterly Foldable Display Report · Chosunbiz · Yonhap Economy