The move

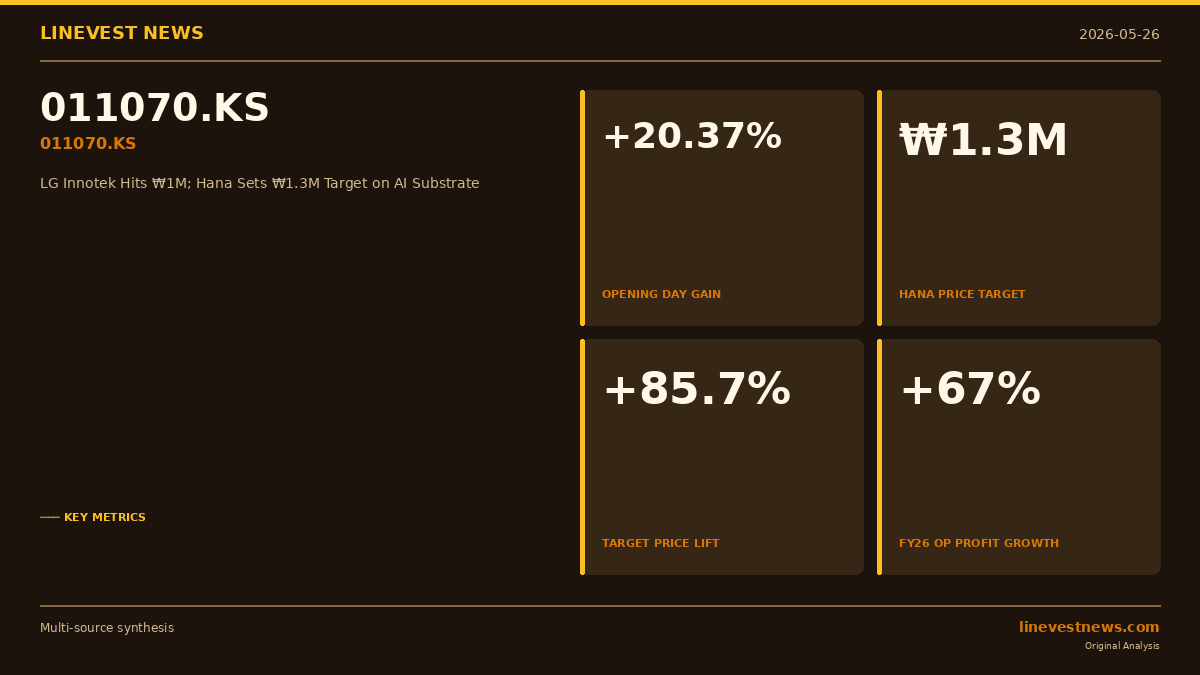

LG Innotek (011070.KS), the camera-module and packaging-substrate affiliate of LG Group, opened up 20.37% on the Korea Exchange on May 26, 2026, trading at ₩1,040,000 ($759) by 9:16 a.m. local time after the prior session closed at ₩864,000 ($631), according to Chosun Biz. The stock pushed as high as ₩1,115,000 ($814) intraday — a 29.1% advance — and held above the ₩1 million threshold, joining the small group of Korean equities labelled hwangjeju ("emperor stocks") in the local market vernacular, per Seoul Economic Daily (Sedaily).

The immediate trigger was a sharply higher price target from Hana Securities, a Korean brokerage. Analyst Kim Min-kyung raised the 12-month target to ₩1,300,000 ($949) from ₩700,000 ($511) — an 85.7% lift — while keeping a Buy rating, citing earnings improvement across all three divisions: camera modules, package solutions, and flip-chip ball grid array (FC-BGA) substrates, per Hankyung. KB Securities and NH Investment & Securities each lifted their targets to ₩1,200,000 ($876) the same day, according to Chosun Biz.

What is the call actually pricing in?

Hana's earnings math is the most concrete way to size the re-rating. Kim forecasts FY2026 revenue of ₩23.85 trillion ($17.4 billion), up 8.9% year-on-year, and operating profit of ₩1.11 trillion ($810 million), up 67% year-on-year, per Sedaily. Against Q1 2026 actuals of ₩5.53 trillion ($4.04 billion) revenue and ₩295.3 billion ($216 million) operating profit (Sedaily), the full-year operating-profit estimate implies a steep second-half acceleration rather than a straight-line run-rate.

The mix shift inside that profit pool is what the brokerage notes are leaning on. The package solutions division — which makes RF system-in-package (RF SiP), flip-chip chip-scale package (FC-CSP) and FC-BGA substrates — accounts for roughly 8% of group revenue, but its share of operating profit is projected to climb from 19% in 2025 to 21% in 2026 and 30% in 2027, per Bloomingbit citing brokerage forecasts. Package solutions posted Q1 2026 revenue of ₩437.1 billion ($319 million), up 16% year-on-year, per Seoul Economic Daily's April 27 Q1 earnings report, with production-line utilisation reported at 100% even in the seasonally softer second quarter, per Sedaily's May 20 follow-up.

Where the brokerages converge — and where they don't

The ₩1.3 million Hana target sits roughly 8% above the ₩1.2 million targets at KB Securities and NH Investment & Securities (Chosun Biz). Earlier in May, before the latest revisions, the brokerage range was wider: KB Securities had been at ₩950,000, NH Investment & Securities had been at ₩700,000 (since lifted to ₩1,000,000 per Bloomingbit's May 19 tally, then further raised to ₩1,200,000 on May 22), and second-tier houses SK Securities (₩850,000 → ₩1,000,000) and Daol Investment & Securities (₩680,000 → ₩950,000), per Bloomingbit's May 19 tally. The compression of targets toward the ₩1.2–1.3 million band over a single week is the analyst-side reflection of what the tape has already done: shares have "nearly tripled" year-to-date, per Seoul Economic Daily.

The catalyst Hana is underwriting

Kim Min-kyung's note identifies two distinct legs. Near term, the camera-module business is expected to benefit from variable-aperture module adoption in the second half of 2026, lifting average selling prices (Sedaily). Longer term, she points to "server FC-BGA supply visibility next year" as the multiple re-rating element, per Hankyung — i.e., the start of shipments into server CPU and AI-accelerator substrate sockets in 2027. LG Innotek began mass-producing FC-BGAs only in early 2024, entering segments where global supply is thin, per Seoul Economic Daily.

The second leg is the one most exposed to execution risk: the company has not yet disclosed named server-CPU or AI-accelerator design wins, and Hana's own framing — "visibility next year" — leaves the 2027 ramp as an assumption rather than a contracted volume.

What to watch next

The Q2 2026 earnings release, due in late July on the usual reporting cadence, is the next datapoint that can confirm or refute the second-half acceleration baked into the ₩1.11 trillion full-year operating-profit print. Specifically: whether package-solutions revenue growth holds the 16% year-on-year pace seen in Q1, and whether camera-module ASPs begin to inflect with the variable-aperture rollout. Any formal disclosure of a server FC-BGA customer — which the company has not announced as of this report — would be the cleanest signal that the 2027 multiple-re-rating thesis is on track.

This article is for informational purposes only and does not constitute investment advice. Figures cited are drawn from Hana Securities research as reported by Hankyung and Seoul Economic Daily, Chosun Biz market coverage, Bloomingbit, and Seoul Economic Daily English edition. USD equivalents use an approximate rate of 1 USD = ₩1,370.

Sources

- Chosun Biz — LG Innotek surges 20% intraday to emperor-stock tier, May 26, 2026

- Maeil Business Daily — LG Innotek crosses ₩1M as brokerages chase, May 26, 2026

- Hankyung — Hana lifts LG Innotek target to ₩1.3M citing FC-BGA visibility, May 26, 2026

- Seoul Economic Daily — LG Innotek brokerage cluster lifts targets, May 26, 2026

- Sedaily English — LG Innotek Q1 operating profit jumps 136% on chip substrates, April 27, 2026

- Sedaily English — LG Innotek target raised on AI substrate boom, May 20, 2026

- Bloomingbit — Korean brokerages compress targets to ₩1.2–1.3M band, May 22, 2026